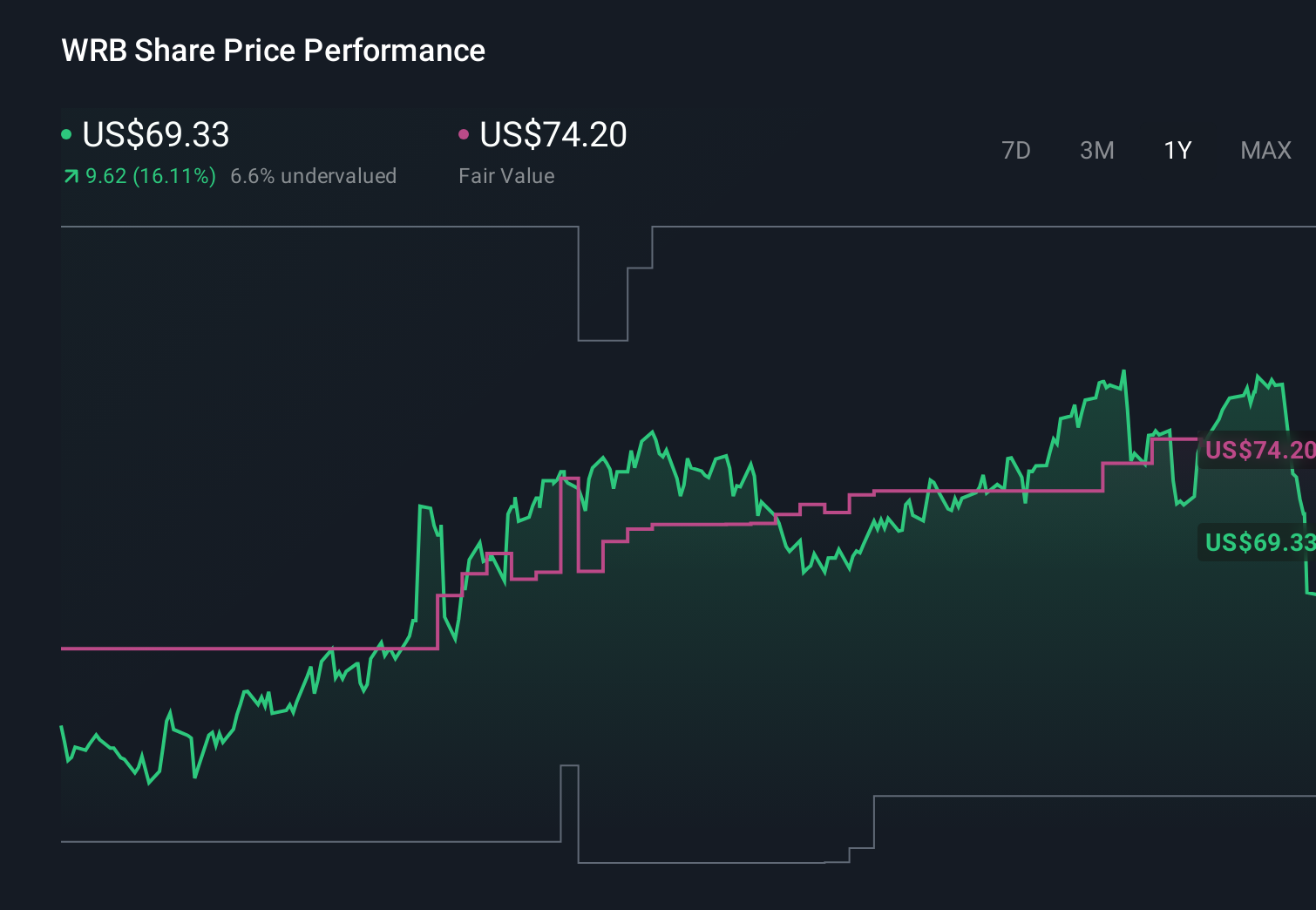

Do Trimmed EPS Estimates Test W. R. Berkley’s Earnings Resilience Story for Investors (WRB)?

- In the past few days, analysts projected that W. R. Berkley would post quarterly earnings of US$1.09 per share and revenue of US$3.70 billion, reflecting modest year-over-year growth despite a small downward revision to earnings estimates over the last month.

- This mix of expected earnings and revenue growth, alongside slightly tempered forecasts, offers a window into how investors may be reassessing W. R. Berkley’s earnings resilience.

- With analysts still expecting higher earnings despite trimmed estimates, we’ll now examine how this shapes W. R. Berkley’s broader investment narrative.

This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

W. R. Berkley Investment Narrative Recap

To own W. R. Berkley, you need to believe in its ability to sustain disciplined underwriting and steady profitability across insurance cycles. The latest analyst expectations for quarterly EPS of US$1.09 on revenue of US$3.70 billion suggest only a modest tweak to near term sentiment, so they do not materially change the key short term catalyst: how resilient margins look in the upcoming results. The biggest near term risk remains pressure on underwriting quality and pricing in competitive property and reinsurance segments.

Recent capital return moves are particularly relevant here, especially the June 2026 decision to lift the regular quarterly dividend by 11.1 percent and pay a US$0.50 special dividend. Together with ongoing buybacks, these actions highlight how management is deploying excess capital at a time when analysts are trimming near term earnings estimates, sharpening the focus on whether future results can comfortably support both underwriting ambitions and continued shareholder distributions.

Yet beneath the reassuring earnings forecasts, investors should be aware of how rising competition and potential pricing slippage could...

Read the full narrative on W. R. Berkley (it's free!)

W. R. Berkley’s narrative projects $14.3 billion revenue and $2.0 billion earnings by 2028. This implies 0.0% yearly revenue growth and an earnings increase of about $0.2 billion from $1.8 billion today.

Uncover how W. R. Berkley's forecasts yield a $68.33 fair value, in line with its current price.

Exploring Other Perspectives

Some of the most optimistic analysts, who were assuming earnings could reach about US$2.1 billion by 2029, lean heavily on margin expansion, whereas this latest EPS revision shows how quickly views on underwriting and loss trends can shift, reminding you that even bullish narratives about stronger specialty growth and climate risk pricing may need to be reconsidered as new information comes through.

Explore 2 other fair value estimates on W. R. Berkley - why the stock might be worth just $68.33!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your W. R. Berkley research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free W. R. Berkley research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate W. R. Berkley's overall financial health at a glance.

No Opportunity In W. R. Berkley?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com