Pandox (OM:PNDX B) Could Be 19% Undervalued Following Q2 Revenue Growth

Pandox (OM:PNDX B) stock is in focus after the company reported Q2 2026 results, with higher sales and revenue but a sharply lower quarterly net income, alongside ongoing climate focused investment projects.

See our latest analysis for Pandox.

Pandox shares have recently bounced, with a 1-day share price return of 3.07% and a 30-day share price return of 3.80%. The stock is still down 12.60% year to date, while a 3-year total shareholder return of 51.92% points to stronger longer term momentum as investors weigh the latest earnings and climate investment updates against previous gains.

If Pandox’s move has you looking wider, this could be a good moment to broaden your search and check out 105 top founder-led companies

Pandox’s latest jump comes after stronger revenue and lease income but a weaker quarterly profit, which leaves a key issue on the table: is the share price now tracking business fundamentals or mainly a swing in sentiment as we look at valuation next?

Most Popular Narrative: 19.3% Undervalued

With Pandox closing at SEK174.80 against a narrative fair value of SEK216.60, the gap between current pricing and analyst expectations is clear and worth unpacking.

Pandox's recent acquisitions, including Hotel Pullman Cologne and Elite Hotel Frost, are expected to achieve stabilized yields of 6.5% and 7%, respectively, which could potentially increase net operating income and overall earnings. The reclassification of Hotel Hubert in Brussels to a Leases segment with a new lease to Numa is anticipated to enhance property value, suggesting an uptick in revenue and cash flows from the property.

Want to see what turns those hotel yields and lease shifts into a higher fair value for Pandox? The narrative leans heavily on revenue growth, slimmer margins and a much richer future earnings multiple.

Result: Fair Value of SEK216.60 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this upbeat Pandox narrative still leans on assumptions that could be tested by weaker Own Operations demand or ongoing currency swings that affect reported asset values.

Find out about the key risks to this Pandox narrative.

Another View: Pandox Versus the SWS DCF Model

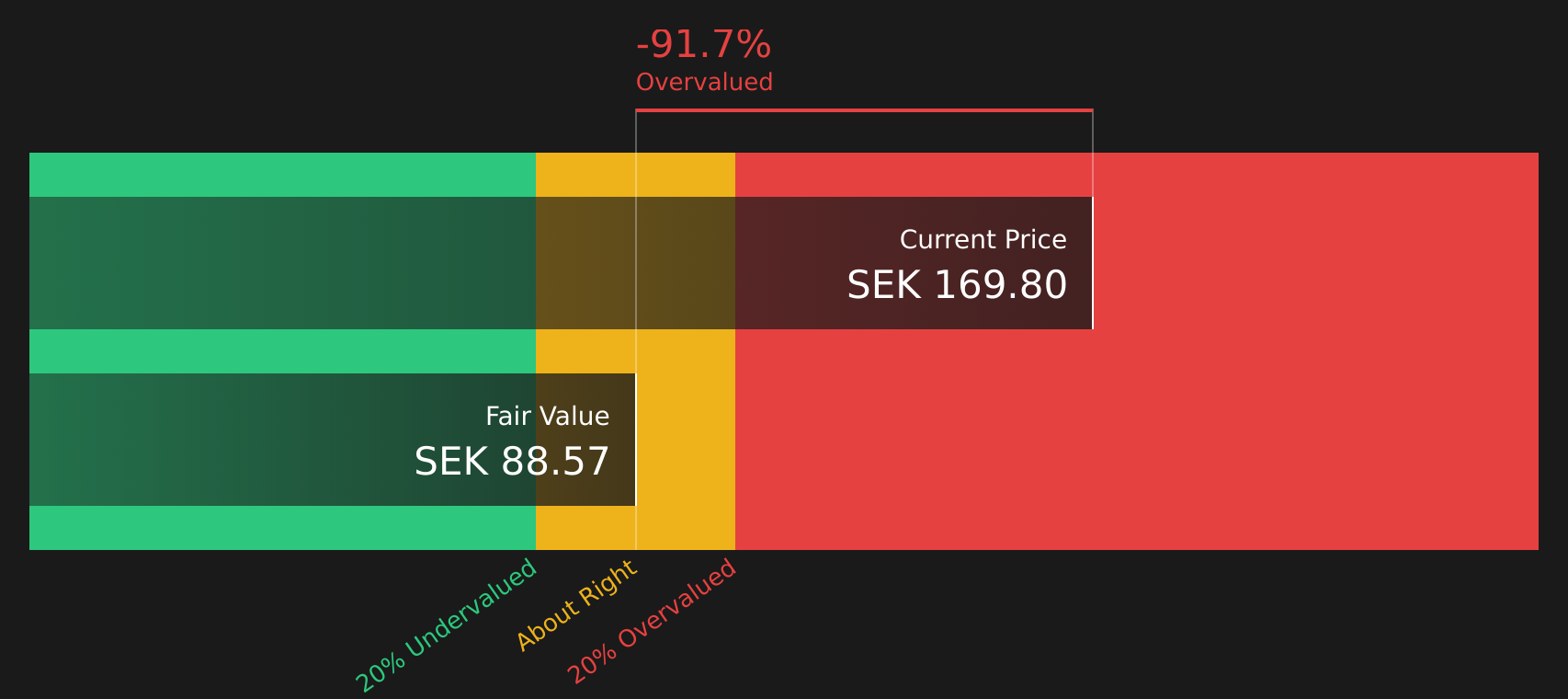

There is a clear clash between the upbeat analyst narrative on Pandox and the Simply Wall St DCF model, which estimates a future cash flow value of SEK87.22 per share versus the current SEK174.80. This implies the stock is trading above that DCF estimate rather than below it.

This raises a practical question for you, as an investor: which story about Pandox’s future cash flows feels more realistic?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Pandox for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 216 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment on Pandox clearly split between upside potential and valuation questions, it makes sense to move quickly and assess the data yourself. To get a balanced snapshot of what is worrying investors and what they are optimistic about, start with these 5 key rewards and 4 important warning signs

Looking for more investment ideas beyond Pandox?

If the mixed signals around Pandox have you thinking about diversification, use this moment to compare fresh opportunities before the next set of results lands.

- Target potential long term compounders by scanning companies with appealing valuations using the 216 high quality undervalued stocks.

- Strengthen your income stream by reviewing businesses that meet strict payout and resilience criteria via the 461 dividend fortresses.

- Prioritise resilience by focusing on companies that score well on financial robustness through the 297 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com