Domino's Pizza (DPZ) Stock Looks Cheap On Fair Value And Earnings

Domino's Pizza stock has fallen 31.9% over the past year, yet both an intrinsic value estimate based on a Discounted Cash Flow (DCF) approach and the market multiples currently point to the shares trading at a discount to their assessed worth. That sets up a clear tension for investors trying to judge whether the recent weakness has already priced in the key risks around margins, competition and consumer demand.

- Over the past 12 months, the share price decline of 31.9% raises the question of whether sentiment has moved further than the underlying cash generation potential of Domino's Pizza.

- Recent coverage has highlighted steady revenue growth and an expanding international footprint as potential supports for cash flow, while concerns about margin pressure and slower international results remain a central risk to how much value investors assign to that growth.

- On Simply Wall St's broader checks, Domino's Pizza screens as a mixed picture rather than a clear bargain or clear overvaluation, with 4 out of 6 valuation metrics pointing to value.

The stock's next move may depend on whether the current discount to intrinsic value and multiples offers enough compensation for the operational and competitive risks that Domino's Pizza still faces.

Find out why Domino's Pizza's -31.9% return over the last year is lagging behind its peers.

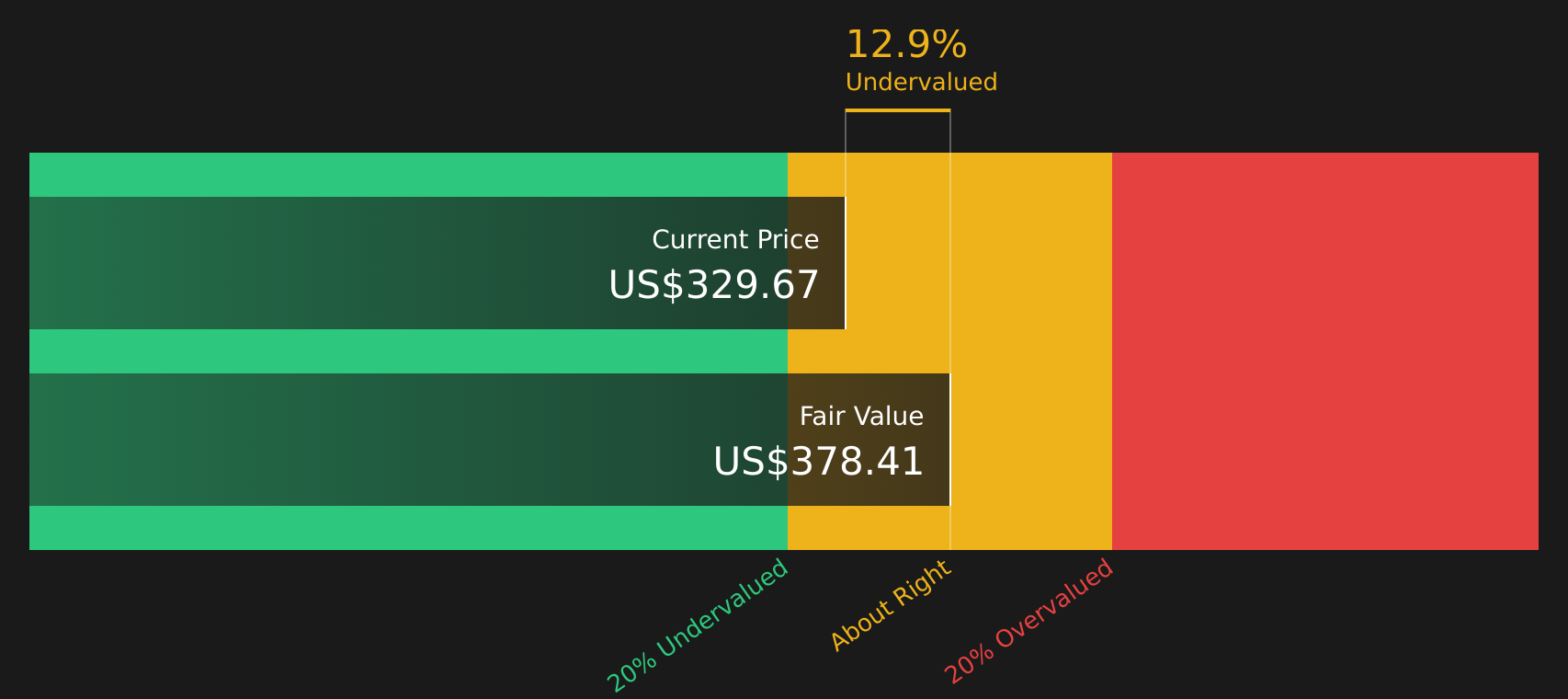

Is Domino's Pizza Still Cheap on Cash Flow?

The Discounted Cash Flow (DCF) model here uses projected free cash flows to equity and discounts them back to today. For Domino's Pizza, the latest twelve month free cash flow is about $657.9 million, and the model assumes cash flows continue growing from this base rather than swinging sharply higher or lower. On that set of cash flows, the DCF points to an estimated intrinsic value of about $379 per share.

Compared with the current share price, that intrinsic value suggests the stock currently appears around 18.0% undervalued. Recent discussion of leadership changes and index shifts, including Domino's Pizza moving into several Russell 2500 indices, may help explain why some investors are cautious even though this particular cash flow analysis supports a higher valuation estimate.

Overall, this DCF analysis indicates that Domino's Pizza stock currently appears undervalued relative to its assessed cash flow value.

Our Discounted Cash Flow (DCF) analysis suggests Domino's Pizza is undervalued by 18.0%. Track this in your watchlist or portfolio, or discover 47 more high quality undervalued stocks.

Does Domino's Pizza Look Undervalued on Earnings?

The P/E ratio is a useful cross check for Domino's Pizza because earnings are a key focus for income oriented investors following its dividend track record. Domino's Pizza currently trades on a P/E of about 17.5x, which is below both the Hospitality industry average of 24.2x and the broader peer average of 26.1x.

On Simply Wall St's fair P/E estimate of 20.4x, which reflects the company's size, margins and risk profile, Domino's Pizza screens at a discount to where this framework would typically place it. The gap between the current 17.5x and the 20.4x fair multiple suggests investors are assigning a lower earnings multiple than the model implies, even as broader checks show a mixed but not extreme risk picture.

Taken together, the P/E workup indicates Domino's Pizza stock appears undervalued on an earnings multiple basis.

See what the numbers say about this price — find out in our valuation breakdown.

The Domino's Pizza Narrative: What Would Justify Today's Price?

Simply Wall St Narratives take the valuation puzzle around Domino's Pizza's cash flows and earnings and explain what kind of future growth, margins and earnings power would need to hold for the stock to be worth meaningfully more or less than it is today. They do this using a set of alternative fair value cases where the underlying assumptions are laid out so you can compare them against Domino's Pizza's actual results over time on the Community page.

Community views on Domino's Pizza sit far apart, with one side seeing clear value and the other focused on execution and category limits.

Bull case: 24% undervalued

"Its franchise business model and disciplined capital allocation decisions also result in a stellar ROIC around 10 times its cost of capital..."

Read the full Bull Case to see why Domino's Pizza could be undervalued

Bear case: 7% overvalued

"Although the U.S. pizza category has been growing at roughly 1% to 2% a year since 2019, Domino's already holds about 1 in 4 U.S. pizza orders..."

Read the full Bear Case to see why Domino's Pizza could be overvalued

Do you think there's more to the story for Domino's Pizza? Head over to our Community to see what others are saying!

The Bottom Line

Domino's Pizza screens as undervalued on both the Discounted Cash Flow (DCF) intrinsic value estimate and its current earnings multiple, so the valuation work points in the same direction rather than giving a mixed signal. That said, the broader checks are not strong enough to call it a straightforward bargain, which keeps the focus on whether the market is correctly discounting the risks around margins, competition and international execution. The key question from here is whether Domino's Pizza can defend profitability and cash generation well enough for that current discount to represent an opportunity rather than a potential value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com