European Market Insights: Antin Infrastructure Partners And 2 Stocks Estimated Below Intrinsic Value

As geopolitical tensions and energy market volatility continue to influence the European markets, the pan-European STOXX Europe 600 Index recently experienced a decline of 1.79%. In this fluctuating environment, identifying stocks that are estimated to be trading below their intrinsic value can offer potential opportunities for investors seeking to navigate these uncertain times.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Vossloh (XTRA:VOS) | €58.55 | €115.61 | 49.4% |

| VIGO Photonics (WSE:VGO) | PLN500.00 | PLN993.48 | 49.7% |

| New Wave Group (OM:NEWA B) | SEK92.60 | SEK180.07 | 48.6% |

| Netcompany Group (CPSE:NETC) | DKK309.00 | DKK606.27 | 49% |

| Micro Systemation (OM:MSAB B) | SEK82.20 | SEK160.16 | 48.7% |

| Koskisen Oyj (HLSE:KOSKI) | €8.58 | €17.14 | 49.9% |

| Jerónimo Martins SGPS (ENXTLS:JMT) | €16.22 | €31.72 | 48.9% |

| Hiab Oyj (HLSE:HIAB) | €53.75 | €106.73 | 49.6% |

| Dustin Group (OM:DUST) | SEK1.844 | SEK3.56 | 48.2% |

| Casta Diva Group (BIT:CDG) | €3.09 | €6.06 | 49% |

Below we spotlight a couple of our favorites from our exclusive screener.

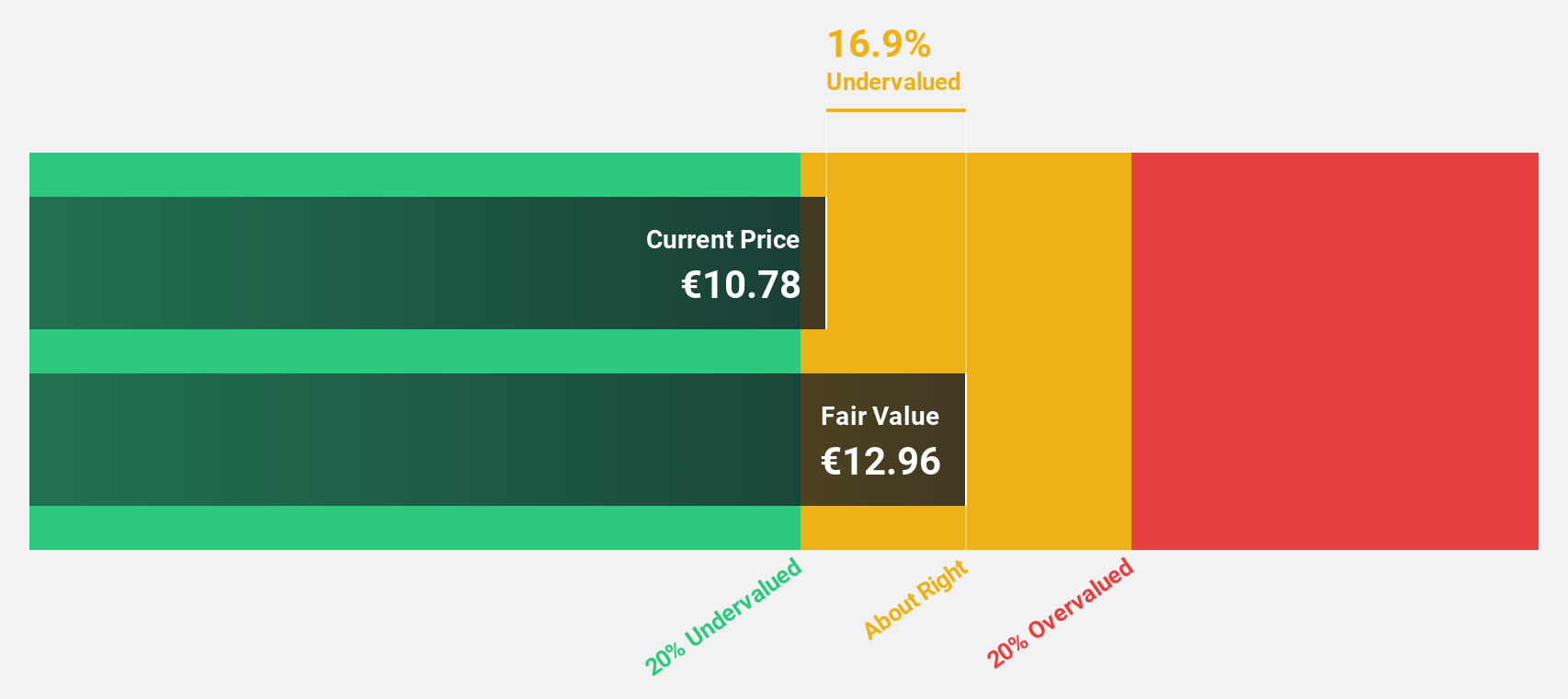

Antin Infrastructure Partners (ENXTPA:ANTIN)

Overview: Antin Infrastructure Partners S.A. is a private equity firm that focuses on infrastructure investments, with a market cap of €1.61 billion.

Operations: The company's revenue primarily comes from its asset management segment, totaling €292.47 million.

Estimated Discount To Fair Value: 33.6%

Antin Infrastructure Partners is trading at €9.02, significantly below its estimated future cash flow value of €13.58, suggesting undervaluation based on cash flows. Despite a dividend yield of 7.87%, the payout isn't well covered by earnings or free cash flows, posing sustainability concerns. However, Antin's revenue and earnings are forecast to grow faster than the French market at 13.2% and 13.9% per year respectively, indicating robust underlying business growth potential despite recent executive changes aimed at strengthening leadership for future fundraising efforts.

- Our earnings growth report unveils the potential for significant increases in Antin Infrastructure Partners' future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Antin Infrastructure Partners.

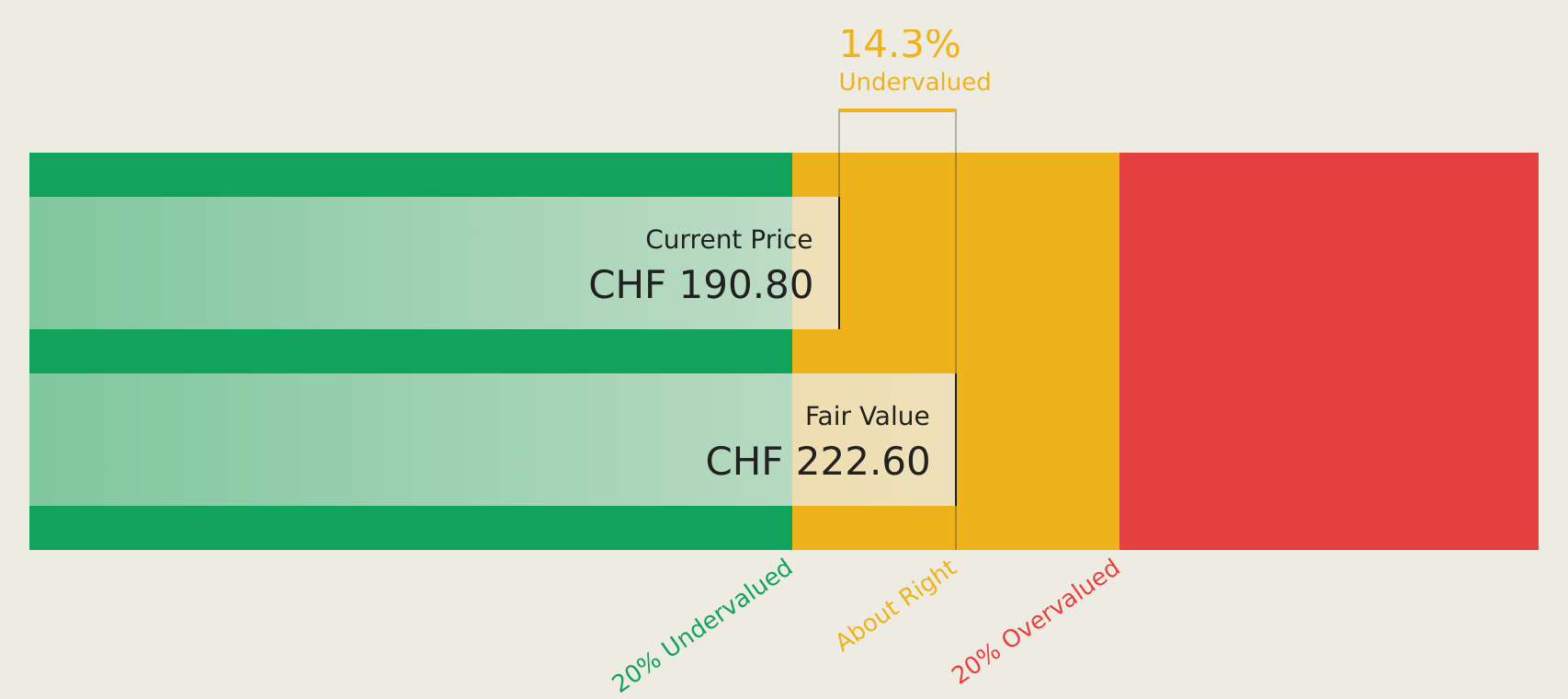

Huber+Suhner (SWX:HUBN)

Overview: Huber+Suhner AG provides power and data connectivity components and system solutions across various regions including Switzerland, Europe, the Middle East, Africa, the Asia-Pacific, and the Americas, with a market cap of CHF3.66 billion.

Operations: The company's revenue segments are comprised of Industry at CHF325.20 million, Communication at CHF274.39 million, and Transportation at CHF264.54 million.

Estimated Discount To Fair Value: 10.8%

Huber+Suhner, trading at CHF198.4, is valued below its estimated future cash flow value of CHF222.42, though not significantly undervalued. Its earnings are projected to grow at 27.2% annually, outpacing the Swiss market's growth rate. Despite recent share price volatility, strategic alliances with Microsoft for HCF cable and connector solutions could enhance long-term revenue prospects by improving optical network performance and efficiency in data centers through innovative technology deployments.

- The analysis detailed in our Huber+Suhner growth report hints at robust future financial performance.

- Click here to discover the nuances of Huber+Suhner with our detailed financial health report.

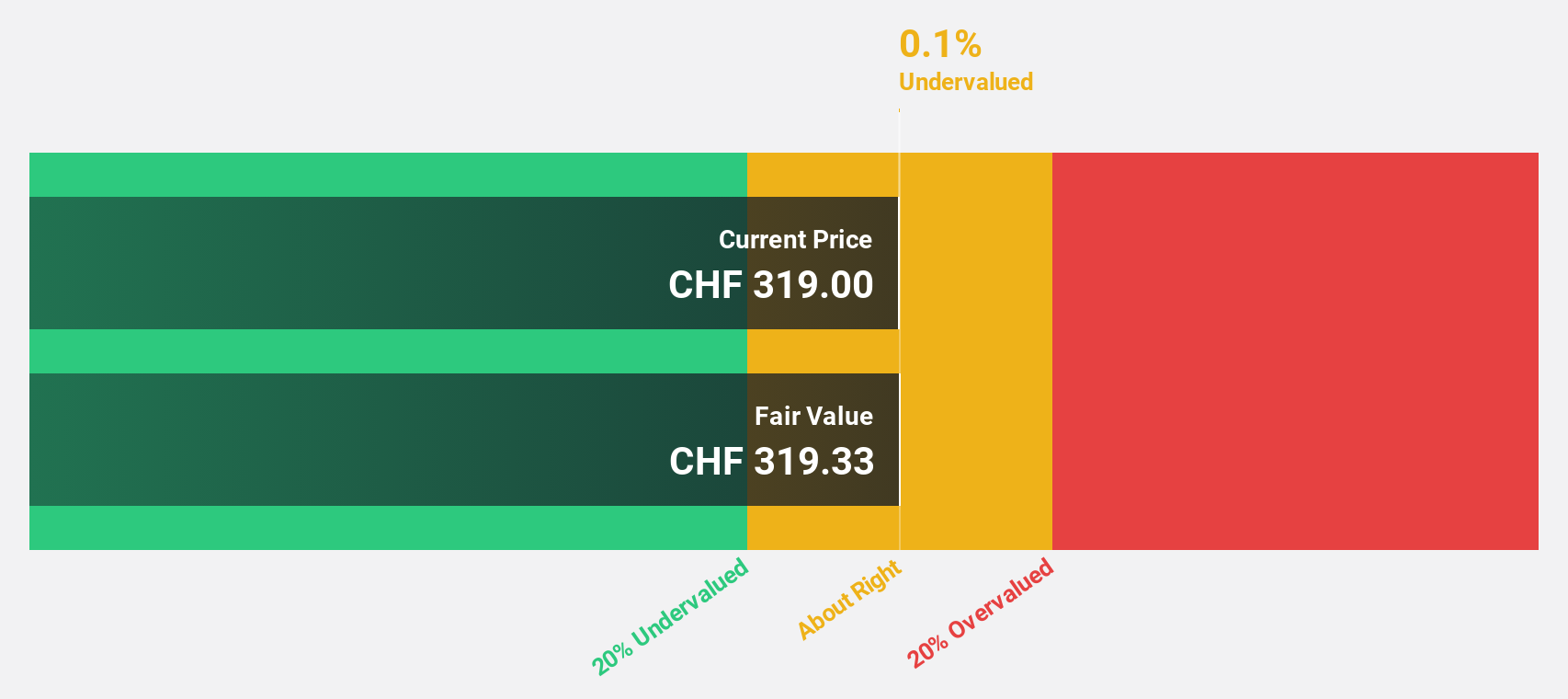

Kardex Holding (SWX:KARN)

Overview: Kardex Holding AG offers intralogistics solutions across Europe, the Middle East, Africa, the Americas, and the Asia Pacific with a market cap of CHF1.86 billion.

Operations: The company's revenue segments include Automated Products generating €572.80 million and Standardized Systems contributing €278.10 million.

Estimated Discount To Fair Value: 38.2%

Kardex Holding, trading at CHF240.5, is significantly undervalued relative to its future cash flow value of CHF388.96. The company's earnings are forecasted to grow at 31.4% annually, surpassing the Swiss market's growth rate of 10.9%. Despite recent share price volatility and a dividend that isn't well covered by earnings or cash flows, Kardex anticipates revenue growth between 15-20% for 2026, potentially enhancing its valuation based on cash flows.

- Our expertly prepared growth report on Kardex Holding implies its future financial outlook may be stronger than recent results.

- Unlock comprehensive insights into our analysis of Kardex Holding stock in this financial health report.

Next Steps

- Unlock more gems! Our Undervalued European Stocks Based On Cash Flows screener has unearthed 198 more companies for you to explore.Click here to unveil our expertly curated list of 201 Undervalued European Stocks Based On Cash Flows.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com