Exploring High Growth Tech Stocks This July 2026

As global markets grapple with renewed Middle East tensions and energy market volatility, the Nasdaq Composite and S&P 500 have managed to post gains, buoyed by a rebound in semiconductor and AI-related shares despite broader economic uncertainties. In this dynamic environment, identifying high growth tech stocks involves looking for companies that can leverage technological advancements and maintain strong performance even amid fluctuating market conditions.

Top 10 High Growth Tech Companies Globally

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Hacksaw | 25.41% | 24.79% | ★★★★★★ |

| Fositek | 29.45% | 38.06% | ★★★★★★ |

| Shengyi Electronics | 31.91% | 35.53% | ★★★★★★ |

| Gold Circuit Electronics | 36.81% | 38.20% | ★★★★★★ |

| Shengyi TechnologyLtd | 23.42% | 27.86% | ★★★★★★ |

| Mobvista | 22.88% | 41.07% | ★★★★★★ |

| KebNi | 27.13% | 90.94% | ★★★★★★ |

| Unimicron Technology | 32.09% | 53.80% | ★★★★★★ |

| CD Projekt | 32.95% | 29.66% | ★★★★★★ |

| CARsgen Therapeutics Holdings | 63.94% | 80.57% | ★★★★★★ |

Underneath we present a selection of stocks filtered out by our screen.

Mycronic (OM:MYCR)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Mycronic AB (publ) is a company that develops, manufactures, and sells production equipment for the electronics industry worldwide, with a market cap of SEK67.49 billion.

Operations: Mycronic generates revenue primarily through its Pattern Generators (PG) segment, which contributes SEK3.26 billion, followed by Global Technologies at SEK2.18 billion. The company also earns from High Volume and PCB Assembly Solutions segments, with revenues of SEK1.87 billion and SEK1.37 billion respectively.

Mycronic's recent performance underscores its resilience and potential within the tech sector, notably with a robust second-quarter earnings report showing sales up to SEK 2.42 billion from SEK 2.07 billion year-over-year, and net income rising to SEK 527 million from SEK 446 million. This growth trajectory is bolstered by strategic client acquisitions, such as the new orders for SLX mask writers in Asia and Europe valued between USD 5-8 million each, highlighting demand in semiconductor manufacturing—a critical area of technological advancement. The company's commitment to R&D is evident with significant investments aimed at enhancing their offerings in photomask production for semiconductors, positioning Mycronic favorably against industry demands and future modernization needs.

- Click here to discover the nuances of Mycronic with our detailed analytical health report.

Explore historical data to track Mycronic's performance over time in our Past section.

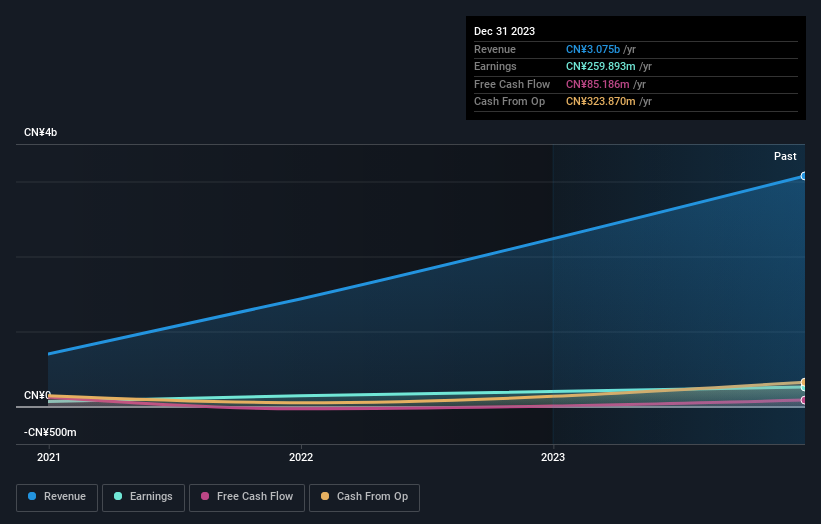

CICT Mobile Communication Technology (SHSE:688387)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: CICT Mobile Communication Technology Co., Ltd. is a company listed on the Shanghai Stock Exchange, focusing on mobile communication technology, with a market cap of CN¥55.66 billion.

Operations: CICT Mobile Communication Technology generates revenue primarily from its mobile communication technology products and services. The company has a market cap of CN¥55.66 billion, indicating its significant presence in the sector.

CICT Mobile Communication Technology has demonstrated a notable trajectory in the high-growth tech sector, with revenue growth projected at 16.7% annually. Despite current unprofitability, earnings are expected to surge by 159.3% per year over the next three years, signaling potential for significant financial turnaround. The company's recent private placement of 70 million shares aims to raise approximately CNY 7 billion, underscoring its strategic initiatives to fuel expansion and innovation. This move aligns with industry trends towards enhancing technological capabilities and market reach, particularly in mobile communications where demand continues to escalate globally.

Shenzhen Uniconn Technology (SZSE:301631)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shenzhen Uniconn Technology Co., Ltd. specializes in the R&D, design, production, sale, and service of electrical connection components in China with a market capitalization of approximately CN¥8.19 billion.

Operations: The company generates revenue primarily from the sale of electrical connection components, totaling approximately CN¥5.51 billion.

Shenzhen Uniconn Technology has recently shown robust financial performance, with a notable increase in annual revenue to CNY 5.15 billion, up from CNY 3.91 billion the previous year, reflecting a growth of approximately 32%. This surge is supported by strategic amendments to company bylaws and capital adjustments aimed at bolstering market competitiveness. Additionally, the firm's commitment to shareholder value is evident from its consistent dividend payouts and a recent proposal for an increased cash dividend. These moves underscore Shenzhen Uniconn’s agility in navigating the tech landscape while maintaining steady profit growth, which stood at an impressive 26% increase year-over-year.

Make It Happen

- Get an in-depth perspective on all 206 Global High Growth Tech and AI Stocks by using our screener here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com