3 Canadian Dividend Stocks With Strong Payouts and Balance Sheets

Dividend Powerhouses can be appealing when inflation, interest rates and growth stories move in different directions across regions. While bond yields and policy signals shift from the US to Europe and Asia, a portfolio anchor of companies paying more than a 5% dividend yield that appears well covered, growing and stable can help keep your cashflow less tied to short term headlines. This article focuses on the Dividend Powerhouses (3%+ Yield) screener and highlights 3 stocks from the list that stand out on income quality, balance sheet strength and consistency of payouts.

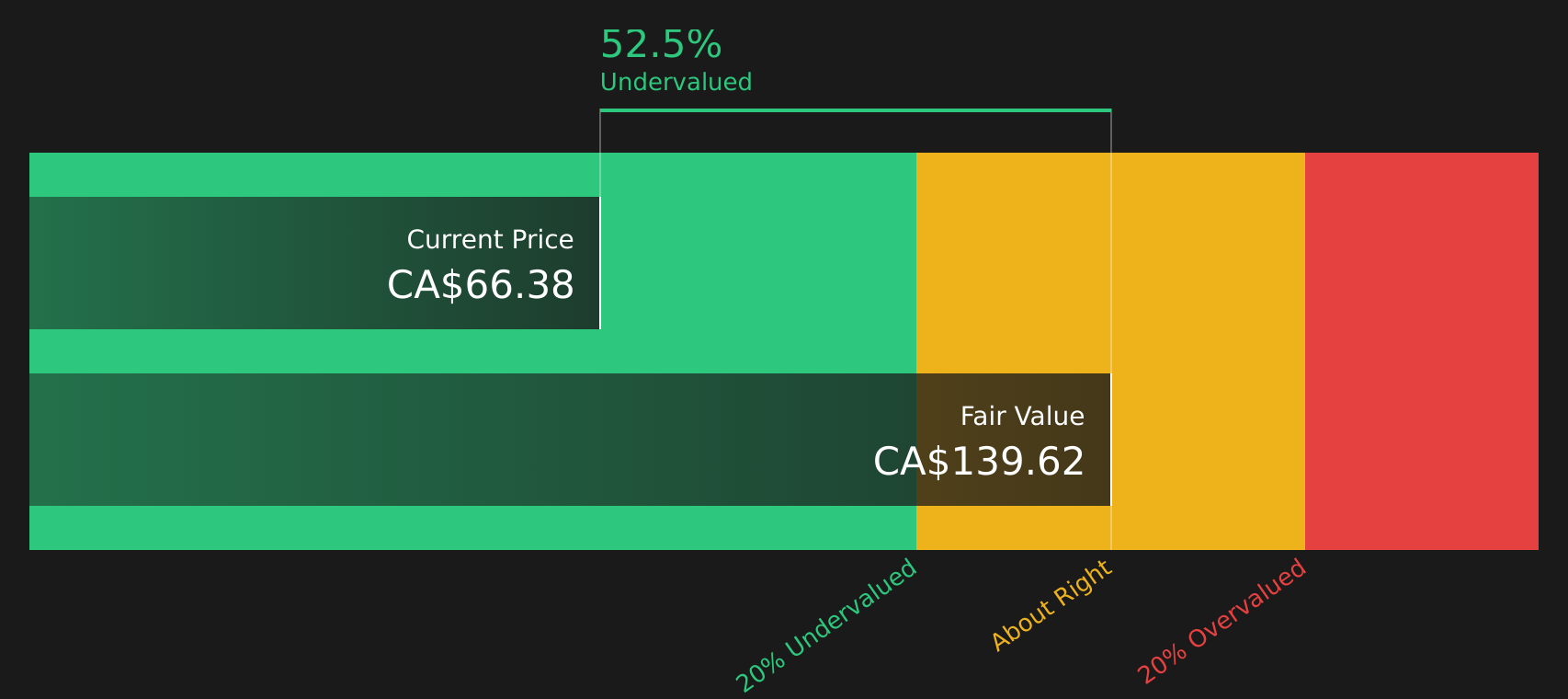

Peyto Exploration & Development (TSX:PEY)

Overview: Peyto Exploration & Development is a Calgary based energy producer focused on exploring, developing and producing natural gas, oil and natural gas liquids in Alberta’s Deep Basin, a core Canadian gas region. The company has operated in this basin since the late 1990s, building a business centered on long life gas assets and supporting infrastructure.

Operations: Peyto generates all of its approximately CA$1.2b in revenue from oil and gas exploration and production activities in Canada, primarily in Alberta’s Deep Basin.

Market Cap: CA$4.9b

Peyto Exploration & Development may appeal to income-focused investors because it combines a relatively high current yield with exposure to long term gas demand tied to LNG linked pricing through its 10 year Centrica contract starting in 2029. Recent quarterly figures, including CA$426.4 million in Q1 2026 revenue and record production of 147,513 boe/d, illustrate the scale of its operations. Analyst work and Simply Wall St estimates indicate that the stock currently screens as undervalued on cash flow and earnings metrics. At the same time, the business is heavily concentrated in Alberta gas, faces policy and infrastructure cost pressures, and has experienced periods when dividends were not steady. Investors therefore need to consider whether the stronger contracts and cost discipline sufficiently balance these risks.

Peyto’s yield and LNG linked contract story looks compelling, but the real question is whether the current pricing already reflects that potential or not, and what the DCF valuation analysis for Peyto Exploration & Development reveals about the trade off between upside and concentration risk.

Canadian Natural Resources (TSX:CNQ)

Overview: Canadian Natural Resources is a large Calgary headquartered energy producer that acquires, develops and produces crude oil, natural gas and NGLs across Western Canada, the North Sea and Offshore Africa, selling everything from synthetic crude and oil sands bitumen to light, medium and heavy crude products.

Operations: Canadian Natural Resources generates most of its revenue from Exploration and Production in North America at about CA$19.1b and Oil Sands Mining and Upgrading at about CA$17.4b. There are additional contributions from Midstream and Refining of CA$818m and North Sea Exploration and Production of CA$217m.

Market Cap: CA$124.8b

Income investors looking at Canadian Natural Resources get a mix of scale, capital returns and some important questions about how long that can last. The company combines a roughly 4% dividend yield with a long record of annual dividend growth and active buybacks, supported by high margins, strong recent earnings, and a diversified asset base that includes oil sands, conventional production and midstream assets. At the same time, heavy exposure to oil sands, reliance on external funding and analyst expectations for earnings and revenue declines over the next few years mean the profile is not risk free. The real interest lies in whether the current valuation and future capital returns fairly reflect those cross currents or leave something on the table.

Canadian Natural Resources sits at the crossroads of scale, a roughly 4% yield and active buybacks, yet many investors may not fully grasp what the 4 key rewards and 2 important warning signs (1 is major!) is hinting at beneath those headline returns

Manulife Financial (TSX:MFC)

Overview: Manulife Financial is a Toronto based global insurer and wealth manager that provides life insurance, retirement, investment and banking style products to individuals and institutions across Canada, the U.S., Asia and other markets.

Operations: Manulife Financial generates around CA$7.1b from Global Wealth and Asset Management, CA$4.5b from Asia insurance and annuity products, CA$3.3b from Canada, CA$755m from Corporate and Other, and CA$355m from the U.S., supported by diversified geographic revenues across Asia, the U.S. and Canada.

Market Cap: CA$97.9b

Manulife Financial stands out on the Dividend Powerhouses screener because it mixes a 3.21% dividend yield with double digit earnings and revenue growth forecasts, improving profit margins and a business that spans both insurance and asset management. Recent net income of CA$1,193m and the latest dividend declaration underline the company’s emphasis on steady capital returns, while AI led initiatives in wealth and asset management and recognition as the top life insurer for AI maturity point to an effort to keep costs in check and widen its product reach. At the same time, heavy use of external funding, insider selling and rapid leadership turnover raise questions about risk and governance that careful investors will want to weigh against the upside story.

Manulife Financial’s mix of AI driven efficiency and multi region earnings potential appears to mark an inflection point for its income story, but the real twist sits in the full narrative for Manulife Financial

The three Dividend Powerhouses highlighted here are just a starting point. The full Dividend Powerhouses (3%+ Yield) screen surfaces 9 more companies that pair high yields with income stories you have not seen yet on this page through the Dividend Powerhouses (3%+ Yield) screener. To identify and analyze the highest conviction dividend plays for your own portfolio, Simply Wall St lets you filter for the precise catalysts and narratives covered in this article so you can focus on the income streams that fit your goals.

Take Control of Your Investment Journey

If Canadian Natural Resources or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives For Your Curiosity?

Some of the sharpest moves start quietly, then momentum builds and prices are flying before most investors notice. Scan fresh ideas that are under the radar for now and aim to act before broader interest develops.

- Target resilient payers with staying power by running a focused search through the 6 dividend fortresses while yields are still holding up and attention is elsewhere.

- Look for fast moving enablers of next generation chips and data centers by scanning the curated 52 AI infrastructure stocks before additional capital flows into the strongest stories.

- Explore the build out of tomorrow’s power networks by reviewing the hand picked 34 power grid technology and infrastructure stocks while these grid upgrade plays are still issuing new filings.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com