Are Vestis (VSTS) Labor Pressures Quietly Rewriting Its Cost Structure And Service Reliability Story?

- Workers at Vestis, represented by Teamsters Local 135, recently launched an unfair labor practice strike after alleging the company threatened employees for engaging in protected concerted activity under the National Labor Relations Act, while also calling for fair pay and benefits.

- This labor dispute introduces fresh operational and legal risks for Vestis, potentially affecting service reliability and cost structures at a time of ongoing business challenges.

- We’ll now examine how this unfair labor practice strike, and the related operational and legal pressures, may reshape Vestis’s investment narrative.

We've uncovered the 10 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

Vestis Investment Narrative Recap

To own Vestis, you need to believe it can turn a challenged, debt‑heavy uniform rental business into a steadier, higher‑margin operator by improving pricing, service quality, and technology. The unfair labor practice strike adds near term legal and operational uncertainty, but with 29 workers involved, the direct impact on the key catalyst of operational turnaround and on the existing top risk of high leverage and pressured margins appears manageable for now.

The recent Q2 FY2026 results, with US$659.44 million in sales and only US$2.6 million in net income, are particularly relevant here because they highlight how limited Vestis’s earnings cushion is if strikes, legal costs, or service disruptions increase expenses. When margins are this thin, even modest labor related pressures can influence how quickly management can invest in technology upgrades and route optimization that are central to the turnaround story.

But beneath the improving revenue forecasts some analysts were using, there is a labor and customer service risk investors should be aware of...

Read the full narrative on Vestis (it's free!)

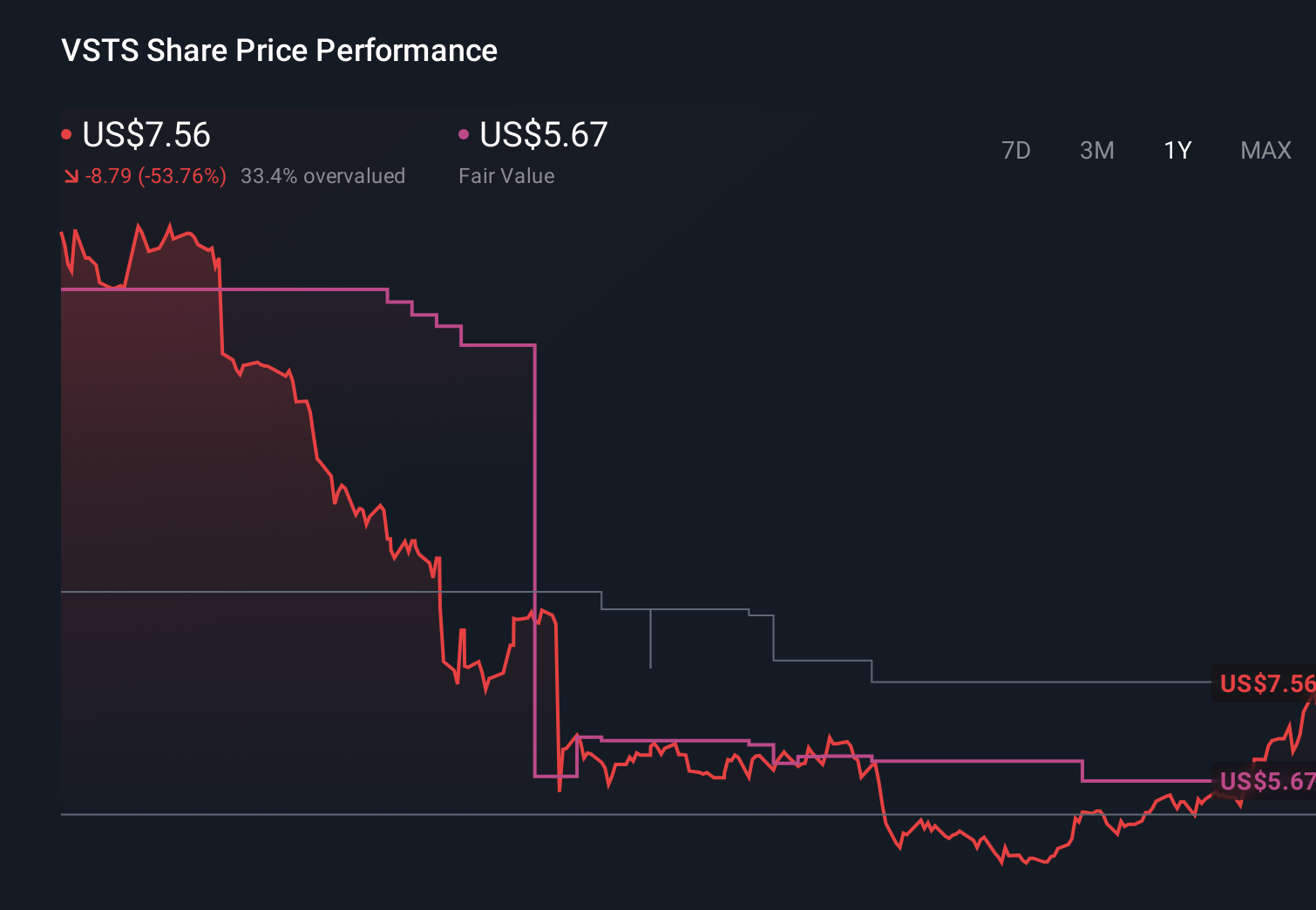

Vestis’ narrative projects $2.8 billion revenue and $110.4 million earnings by 2029.

Uncover how Vestis' forecasts yield a $10.16 fair value, a 35% downside to its current price.

Exploring Other Perspectives

Before this strike, the most optimistic analysts were assuming revenue of about US$2.9 billion and earnings of roughly US$132 million by 2029, yet ongoing service and labor issues could challenge that path, so it is worth weighing these upbeat forecasts against the risk that customer attrition and employee unrest prove harder to fix than expected.

Explore another fair value estimate on Vestis - why the stock might be worth just $15.00!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Vestis research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Vestis research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Vestis' overall financial health at a glance.

No Opportunity In Vestis?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- Find 47 companies with promising cash flow potential yet trading below their fair value.

- Invest in the nuclear renaissance through our list of 90 elite nuclear energy infrastructure plays powering the global AI revolution.

- Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com