Everspin Technologies (MRAM) Stock Looks Undervalued On Cash Flow But Overvalued On Sales

Everspin Technologies stock has more than doubled over the past five years, yet its valuation signals are split, with a Discounted Cash Flow (DCF) intrinsic value estimate suggesting the shares trade at a discount while market based multiples point to a richer pricing.

- Everspin Technologies has returned 214.0% over 5 years, which puts current buyers in the position of judging whether that gain already reflects the company’s long term cash flow potential.

- Recent US defense related contracts and index inclusion can support expectations for future cash flows, but reliance on a limited set of large customers may increase the risk that any contract changes weigh heavily on those cash flows.

- The company scores 4 out of 6 on the broader valuation checks, which is a mixed picture rather than a clear bargain or clear overvaluation, and you can see the breakdown at 4.

The key question for investors is whether the 20.7% discount indicated by the DCF style intrinsic value estimate outweighs the signal from richer market multiples for Everspin Technologies.

Is Everspin Technologies a Bargain on Cash Flow?

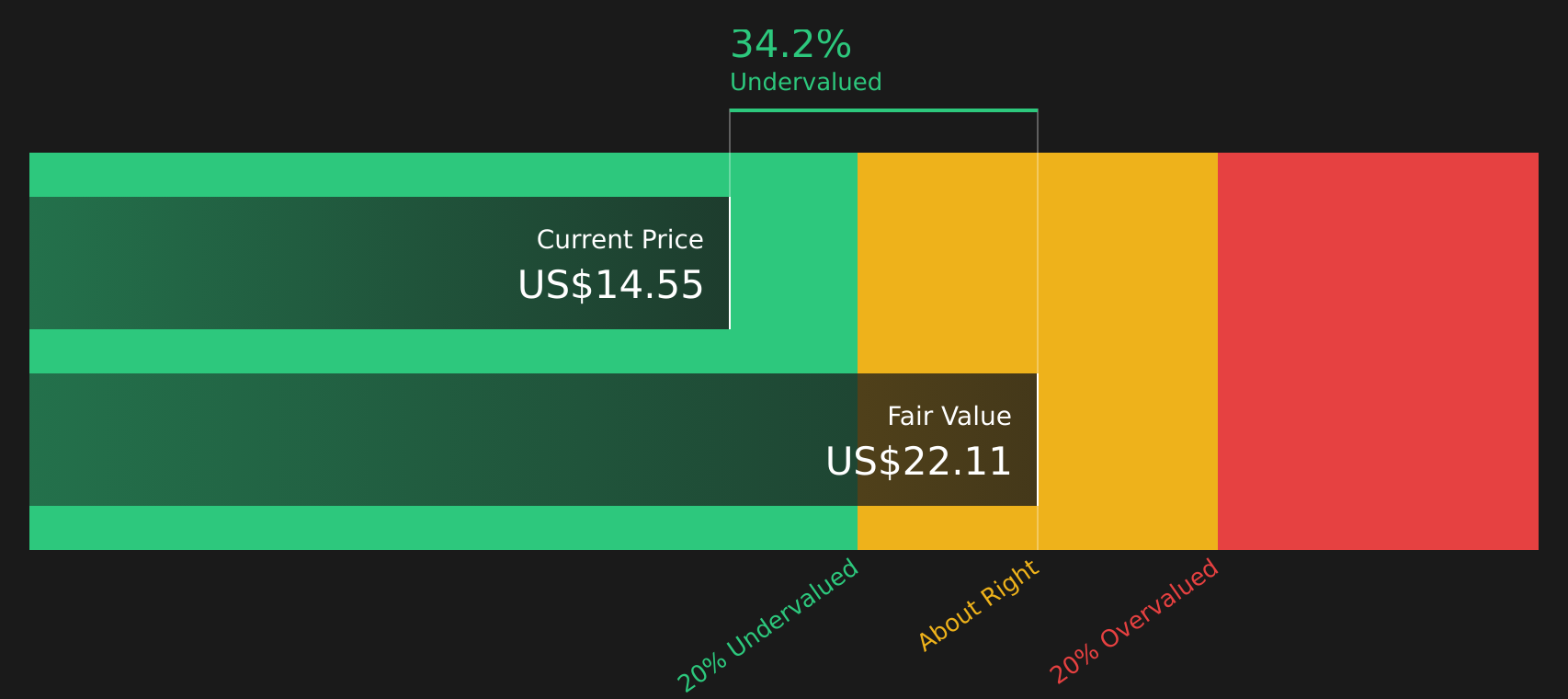

The Discounted Cash Flow (DCF) model used here projects the cash Everspin Technologies could generate for shareholders and discounts it back to today. Based on the latest twelve month figures, the company produced around $4.2 million in free cash flow, and the DCF assumes that cash flows grow from this base rather than shrink.

Under those assumptions, the model arrives at an estimated intrinsic value of about $22.07 per share, which is roughly 20.7% above the current share price. The recent $40 million US defense subcontract helps explain why the market is willing to ascribe richer growth expectations. At the same time, the DCF output indicates that the current share price does not fully reflect the projected cash generation.

Overall, the Discounted Cash Flow (DCF) workup indicates that, relative to its modeled cash flows, Everspin Technologies stock appears undervalued.

Our Discounted Cash Flow (DCF) analysis suggests Everspin Technologies is undervalued by 20.7%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Is Everspin Technologies Getting Expensive on Sales?

The P/S ratio is a useful cross check for Everspin Technologies because revenue is less affected by accounting choices than earnings, and the company’s P/E is currently very high.

Everspin Technologies trades on a P/S of about 7.2x, which is slightly below the semiconductor industry average of 7.9x and well below the peer group average of 15.4x. However, the tailored fair P/S ratio for the company is estimated at 5.8x, reflecting its specific growth outlook, margins, size, and risk profile.

Compared with that 5.8x fair multiple, the current 7.2x suggests investors are paying a premium to the level implied by those fundamentals, even if the stock does not look stretched against some peers. This gap indicates that, on sales, Everspin Technologies stock is pricing in stronger conditions than the model assumes.

On the P/S multiple, Everspin Technologies stock currently screens as overvalued relative to its modeled fair ratio.

See what the numbers say about this price — find out in our valuation breakdown.

The Everspin Technologies Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Everspin Technologies pick up where this valuation split leaves off, by setting out in plain terms which combinations of future growth, margins and earnings would need to hold for Everspin Technologies' stock to be worth materially more or materially less than today's price. These narratives are available on the company's Community page. Rather than relying on a single multiple or model output, each narrative lays out the assumptions behind its fair value so you can revisit them as new results are released.

One of the top community narratives on Everspin Technologies: roughly fairly valued

"This narrative explores a more pessimistic perspective on Everspin Technologies compared to the consensus, based on a Fair Value that aligns with the bearish cohort of analysts."

Read one of the top narratives on Everspin Technologies

Do you think there's more to the story for Everspin Technologies? Head over to our Community to see what others are saying!

The Bottom Line

For Everspin Technologies, the Discounted Cash Flow (DCF) workup points to an intrinsic value above the current share price, while the sales based multiples suggest the stock is overvalued relative to its tailored fair P/S ratio. That gap reflects different emphases, with the intrinsic value view anchored on cash flow timing and capital needs, and the multiples view more about how much growth and sentiment are already in the price. With broader valuation checks landing in mixed territory, the key consideration is whether future cash flows and contract stability ultimately justify paying a premium multiple, or whether the current discount to intrinsic value proves to be a value trap.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com