3 TSX Stocks Estimated To Be Trading Below Fair Value By At Least 38.7%

The Canadian market has seen robust earnings growth, particularly driven by the energy and material sectors, contributing to a projected 32% increase in TSX earnings for the second quarter. As investors navigate these conditions, identifying stocks trading below their fair value can offer opportunities for those looking to capitalize on potential undervaluation amidst strong sector performance.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Timbercreek Financial (TSX:TF) | CA$6.36 | CA$12.47 | 49% |

| TFI International (TSX:TFII) | CA$210.02 | CA$368.98 | 43.1% |

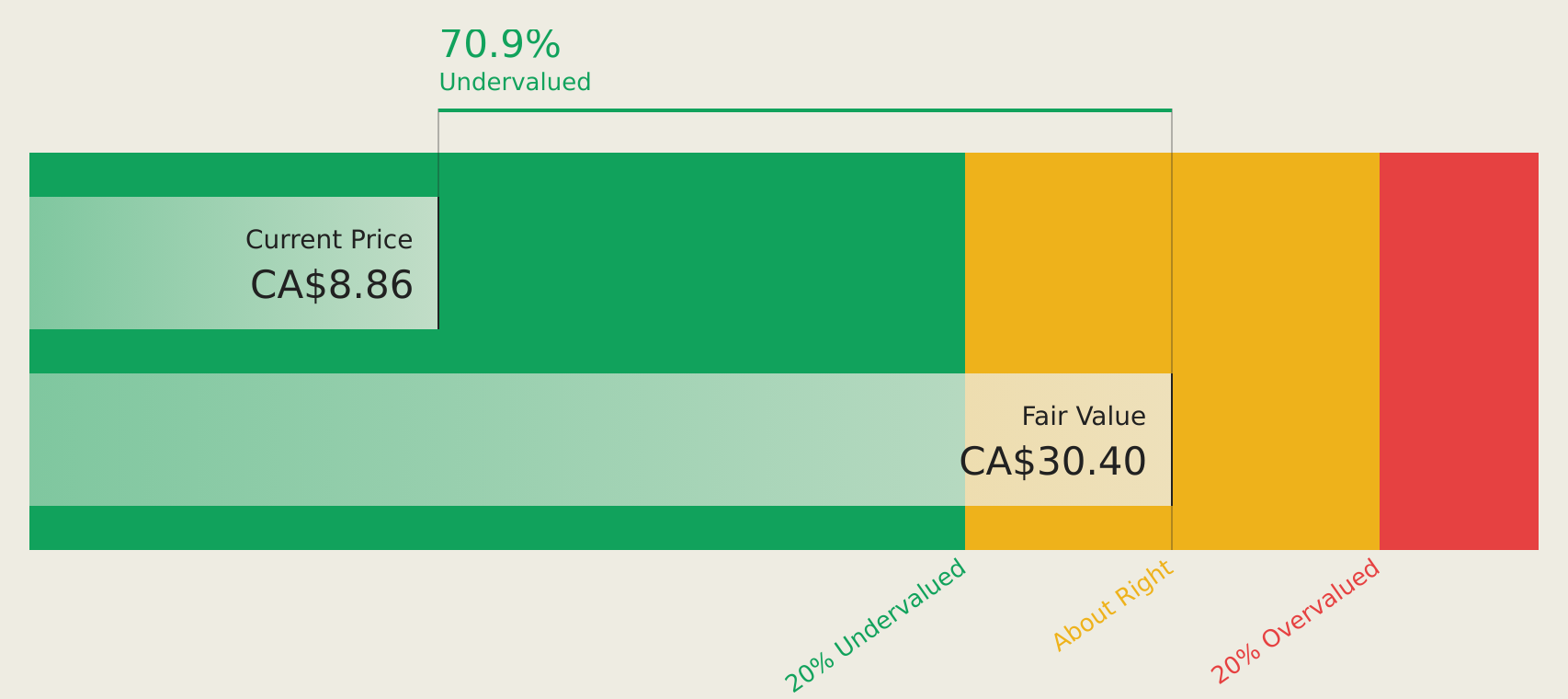

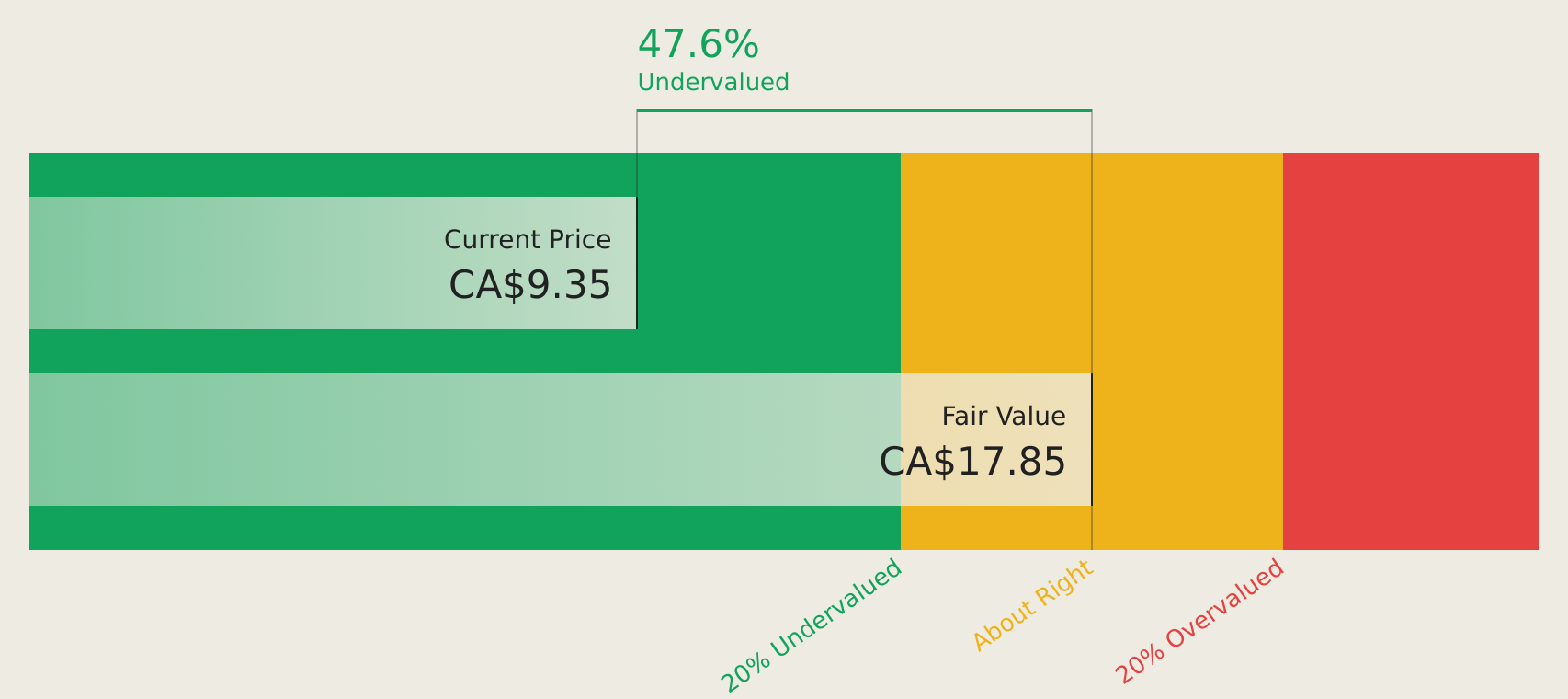

| Surge Energy (TSX:SGY) | CA$9.39 | CA$17.85 | 47.4% |

| Medexus Pharmaceuticals (TSX:MDP) | CA$5.13 | CA$9.18 | 44.1% |

| Mattr (TSX:MATR) | CA$17.07 | CA$27.85 | 38.7% |

| Hemlo Mining (TSX:HMMC) | CA$6.50 | CA$11.76 | 44.7% |

| G Mining Ventures (TSX:GMIN) | CA$40.24 | CA$79.83 | 49.6% |

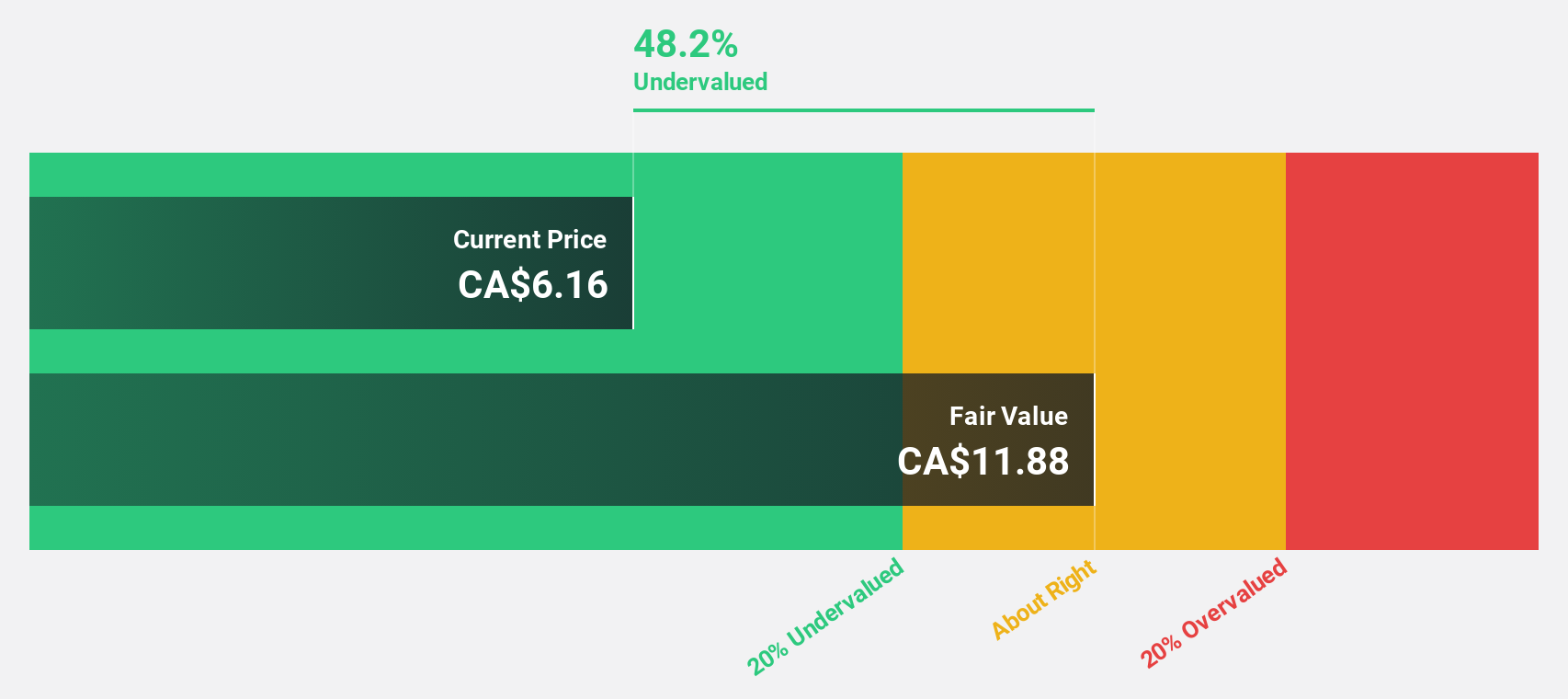

| Endeavour Silver (TSX:EDR) | CA$11.37 | CA$21.94 | 48.2% |

| Chemtrade Logistics Income Fund (TSX:CHE.UN) | CA$17.03 | CA$30.39 | 44% |

| Aritzia (TSX:ATZ) | CA$146.58 | CA$252.00 | 41.8% |

We're going to check out a few of the best picks from our screener tool.

Endeavour Silver (TSX:EDR)

Overview: Endeavour Silver Corp. is a silver mining company involved in the acquisition, exploration, development, extraction, processing, refining, and reclamation of mineral properties in Mexico, Chile, Peru, and the United States with a market cap of CA$3.28 billion.

Operations: The company's revenue segments include Bolanitos at $62.30 million and Guanaceví at $215.80 million, with a segment adjustment of $335.60 million.

Estimated Discount To Fair Value: 48.2%

Endeavour Silver is trading at CA$11.37, significantly below its estimated future cash flow value of CA$21.94, highlighting potential undervaluation based on cash flows. Recent announcements show strong operational performance with increased silver and gold sales and production compared to the previous year. The company reported a notable turnaround in financial results with first-quarter net income of US$64.9 million against a loss last year, driven by robust revenue growth forecasted at 9% annually over the Canadian market average.

- Upon reviewing our latest growth report, Endeavour Silver's projected financial performance appears quite optimistic.

- Delve into the full analysis health report here for a deeper understanding of Endeavour Silver.

Mattr (TSX:MATR)

Overview: Mattr Corp. is a materials technology company serving infrastructure markets such as electrification, transportation, and energy across various regions including Canada and the Asia Pacific, with a market cap of CA$854.52 million.

Operations: The company's revenue is derived from two main segments: Composite Technologies, contributing CA$531.80 million, and Connection Technologies, generating CA$738.35 million.

Estimated Discount To Fair Value: 38.7%

Mattr is trading at CA$17.07, well below its estimated future cash flow value of CA$27.85, suggesting potential undervaluation based on cash flows. Despite a recent dip in net income to CA$7.4 million from last year's CA$52.73 million, earnings are forecasted to grow significantly at 52.5% annually, outpacing the Canadian market average of 10.9%. However, profit margins have declined and interest payments remain poorly covered by earnings.

- Our comprehensive growth report raises the possibility that Mattr is poised for substantial financial growth.

- Click here to discover the nuances of Mattr with our detailed financial health report.

Surge Energy (TSX:SGY)

Overview: Surge Energy Inc. is involved in the exploration, development, and production of oil and gas properties in Western Canada, with a market cap of CA$940.82 million.

Operations: The company generates revenue of CA$479.11 million from its oil and gas exploration and production activities in Western Canada.

Estimated Discount To Fair Value: 47.4%

Surge Energy, trading at CA$9.39, is valued below its estimated future cash flow value of CA$17.85, highlighting potential undervaluation based on cash flows. Despite recent insider selling and a net loss of CA$24.68 million in Q1 2026, earnings are expected to grow significantly at 89.5% annually, surpassing the Canadian market average of 10.9%. However, dividends remain poorly covered by earnings amidst steady production growth forecasts for the year.

- Our earnings growth report unveils the potential for significant increases in Surge Energy's future results.

- Dive into the specifics of Surge Energy here with our thorough financial health report.

Where To Now?

- Unlock more gems! Our Undervalued TSX Stocks Based On Cash Flows screener has unearthed 19 more companies for you to explore.Click here to unveil our expertly curated list of 22 Undervalued TSX Stocks Based On Cash Flows.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com