Cenovus Energy (TSX:CVE) Stock Looks Like A Bargain Despite A 345% Run

Cenovus Energy’s share price has surged over the past few years, and after a very strong 5 year return alongside a high valuation score that screens the stock as undervalued on several checks, the key issue now is whether the current price still leaves room for value focused investors.

- Cenovus Energy has delivered a very large 5 year return of 345.1%, which puts extra emphasis on whether today’s valuation still compensates you for the gains already on the table.

- Recent coverage has highlighted earnings upgrades and integration benefits from the MEG Energy acquisition as potential supports for future cash generation, while exposure to commodity price swings and large capital projects can still weigh on how the market prices that cash flow.

- The stock scores highly on Simply Wall St’s checks, with a 5 out of 6 valuation score, which means the broader set of valuation metrics leans cheap rather than expensive at the current level.

The issue now is whether Cenovus Energy’s strong run has fairly reset expectations or whether the valuation checks suggest there is still a margin of safety in the current share price.

Does Cenovus Energy Look Undervalued on Earnings?

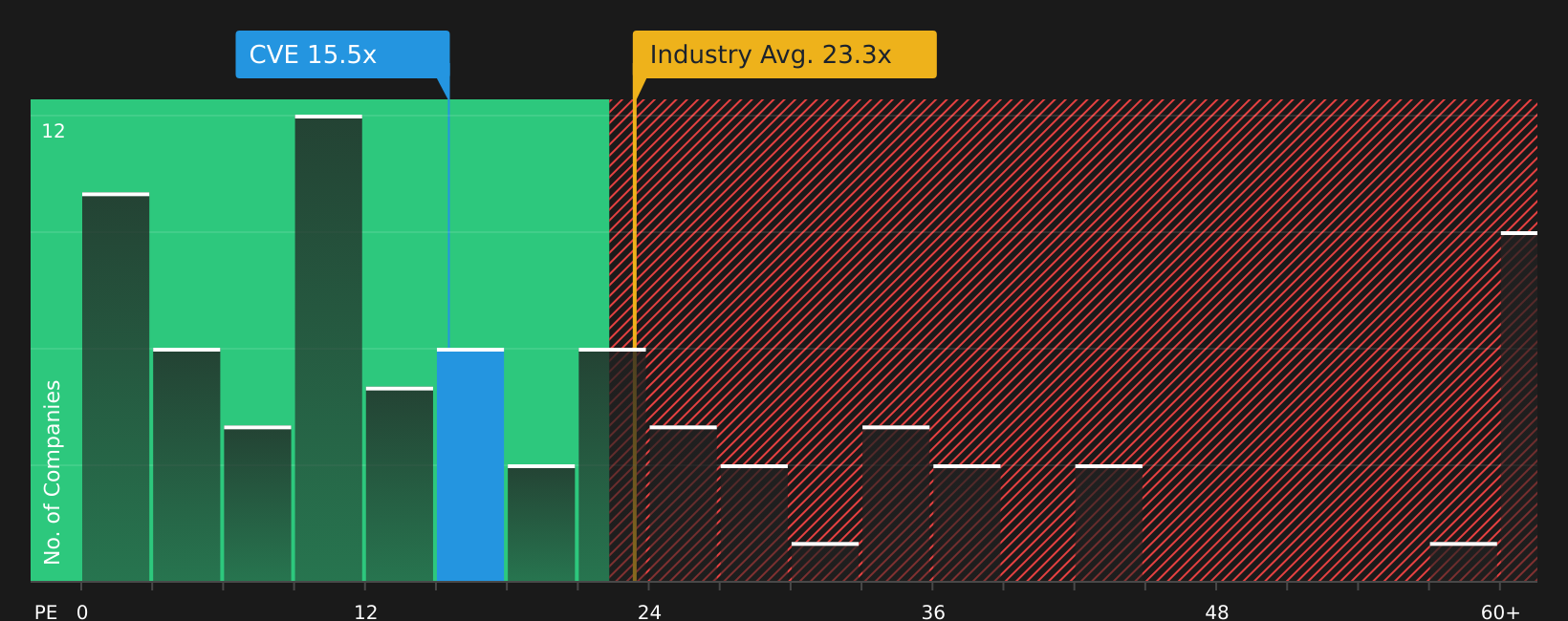

The P/E ratio is a useful metric for Cenovus Energy because earnings are a key driver for investors monitoring cash generation from oil and gas producers. Cenovus Energy trades at about 15.7x earnings, which is below the Oil and Gas industry average P/E of roughly 24.0x and also under the broader peer group average of 24.8x. This places the stock on a lower multiple than many comparable companies in the sector.

The tailored fair P/E for Cenovus Energy is 19.2x, based on factors such as its margins, scale and risk profile, so the current P/E sits meaningfully below that implied level. Despite recent optimism around strong earnings and MEG Energy acquisition synergies, the market is still pricing Cenovus Energy at a discount to what this framework suggests for its earnings profile.

On the P/E multiple, Cenovus Energy stock appears attractively valued relative to both its fair ratio and sector benchmarks.

See what the numbers say about this price — find out in our valuation breakdown.

The Cenovus Energy Narrative: What Would Justify Today's Price?

Simply Wall St Narratives for Cenovus Energy pick up where the valuation checks stop by spelling out which paths for Cenovus Energy's growth, margins and earnings would need to occur for the stock to be worth materially more or materially less than today's price. Each Narrative ties a fair value estimate to a specific story about Cenovus Energy's potential catalysts and risks, so you can track over time which version of events seems to be unfolding on the Community page.

One of the top community narratives on Cenovus Energy: 15% undervalued

"Successful completion of key growth projects such as Narrows Lake, West White Rose, and the Foster Creek optimization is set to deliver significant new, stable, long-life production…"

Read one of the top narratives on Cenovus Energy

Do you think there's more to the story for Cenovus Energy? Head over to our Community to see what others are saying!

The Bottom Line

Cenovus Energy screens as undervalued on current earnings multiples, with the tailored P/E framework suggesting the market is not fully crediting its cash generation profile. That gap likely reflects how investors weigh integration execution, commodity price swings and the capital demands of major projects. For you, the key question is whether that discount compensates for those risks or signals the market is correctly cautious. The crux of the Cenovus Energy debate is whether cash flows from its portfolio and acquisitions prove resilient enough for the P/E to re-rate closer to peers, or whether the stock settles into a lower multiple as the new normal.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com