Corteva (CTVA) Could Be 6% Below Fair Value On Arevo Soybean Seed Deal

Corteva (CTVA) stock is drawing attention after the company partnered with Arevo AB to integrate Arginex Soy, an arginine-based seed treatment, into its soybean seed treatment portfolio for improved crop nutrition and sustainability.

See our latest analysis for Corteva.

Corteva shares, which closed at US$84.91, have cooled slightly in the last week but still show firm momentum, with a 30 day share price return of 11.52% and a 5 year total shareholder return of 114.79%.

If this kind of product focused story has your attention, it can be a good moment to broaden your search and check out 18 top founder-led companies

After Corteva’s recent run and the new Arginex Soy partnership, the share price sits close to analyst targets but at a deeper discount to some intrinsic value estimates, so where does fair value really look anchored now?

Most Popular Narrative: 5.7% Undervalued

Corteva closed at $84.91 compared with a widely followed fair value estimate of about $90, and the current narrative hinges on how earnings and margins evolve under a focused seed and crop protection profile.

Advancements in Corteva's innovation pipeline including premium trait launches (Vorceed, PowerCore), expansion of biological products, and gene editing enable premium pricing, secure market share, and improve product mix, translating into higher gross margins and earnings growth.

Read the complete narrative. Read the complete narrative.

Want to see what sits behind that earnings story for Corteva? The core of this narrative is a specific mix of revenue growth, margin expansion, and a future earnings multiple that treat the company more like a premium inputs provider rather than a commodity chemical stock. Curious which assumptions have the greatest impact on that fair value gap and how sensitive it is to small changes in growth?

Result: Fair Value of $90.05 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the Corteva story could shift if ongoing price pressure in crop protection or tighter environmental regulation weighs on margins and tempers those fair value expectations.

Find out about the key risks to this Corteva narrative.

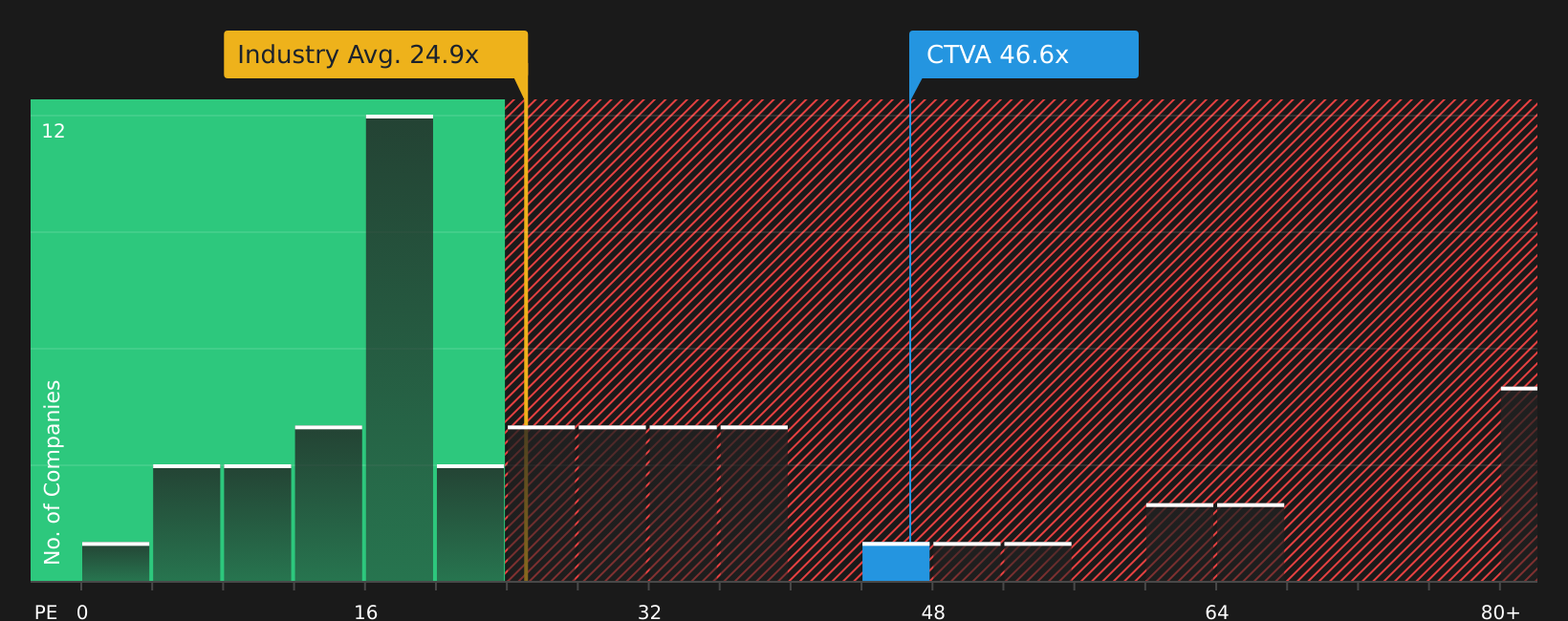

Another View: Corteva Through the P/E Lens

While the SWS DCF model points to Corteva trading below estimated fair value, the picture looks tighter when you look at the P/E ratio. At 45.4x earnings, Corteva sits well above the US Chemicals industry on 25.2x and the fair ratio of 25x, which suggests less room for error if growth or margins fall short. Which yardstick do you trust more when expectations are this high?

See what the numbers say about this price in context of peers and the fair ratio, and how that gap could close over time, in our valuation breakdown See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

With sentiment on Corteva finely balanced between opportunity and caution, now is a useful time to weigh the data yourself and decide where you stand, starting with the 3 key rewards and 1 important warning sign.

Looking for more investment ideas beyond Corteva?

If Corteva has sharpened your interest, do not stop here. Use the Simply Wall Street Screener to compare other stocks, test ideas, and pressure test your portfolio.

- Spot potential bargains early by scanning screener containing 20 high quality undiscovered gems that pair strong fundamentals with relatively low market attention.

- Strengthen your portfolio’s core with solid balance sheet and fundamentals stocks screener (48 results) that emphasize financial resilience and cleaner balance sheets.

- Dial down volatility risk by checking 79 resilient stocks with low risk scores that score well on stability while still offering equity upside.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com