3 Cash Flow Stocks With More Upside Than The Market May Be Pricing In

With inflation worries, higher funding costs and geopolitical tension all pulling markets in different directions, many investors are looking for stocks where current prices appear lower than the long term cash flow potential. That is exactly what the Undervalued Stocks Based On Cash Flows screener aims to highlight. It uses SWS DCF valuation to flag companies where the market price sits below estimated fair value. For readers who want disciplined value ideas instead of chasing headlines, this article will spotlight 3 of the best stocks from the screener and explain why their cash flow profiles stand out today.

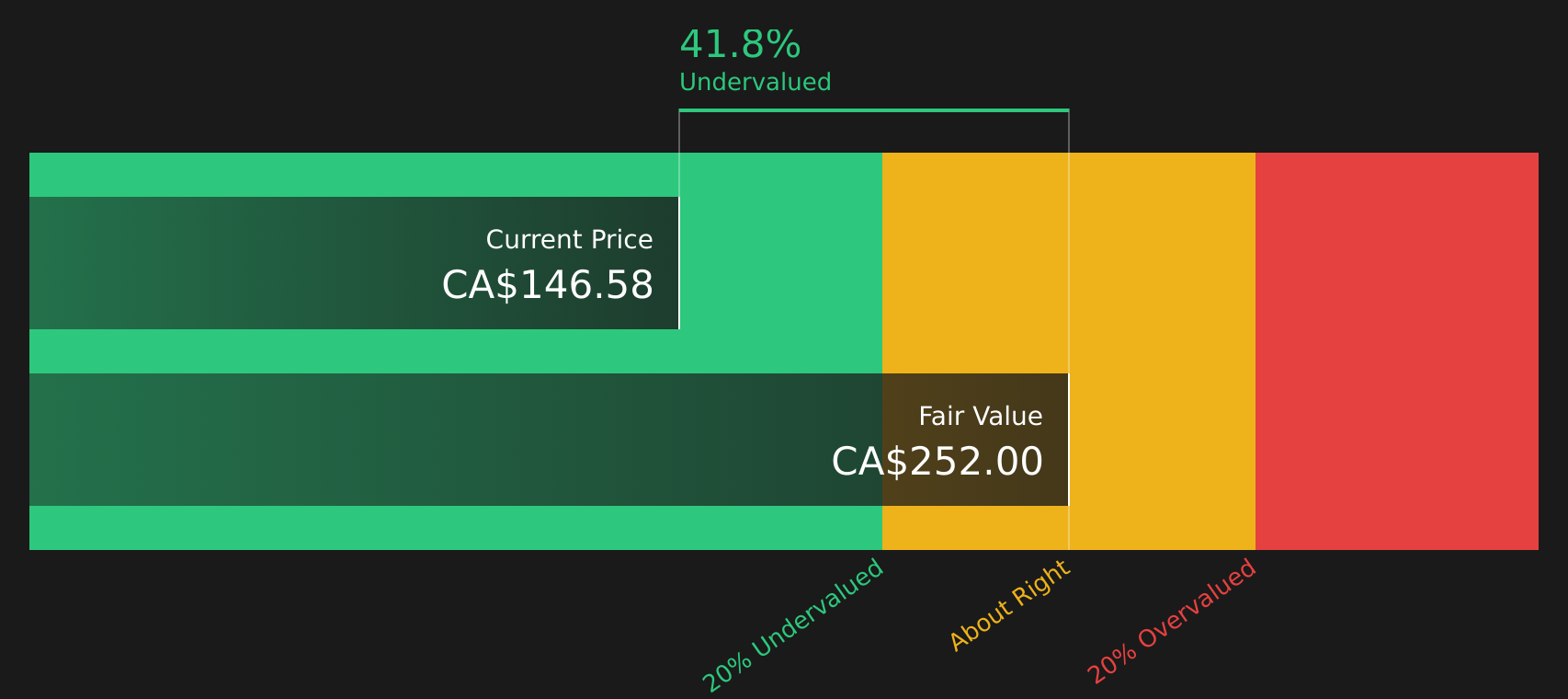

Aritzia (TSX:ATZ)

Overview: Aritzia is a Vancouver based fashion retailer that designs and sells women's apparel and accessories across its own brands, using a mix of boutiques and a fast growing digital channel in Canada and the U.S.

Operations: Aritzia generates about CA$4.0b in revenue, primarily from apparel, with roughly CA$1.5b from Canada and CA$2.5b from the United States.

Market Cap: CA$18.3b

Aritzia stands out in the screener because its fast growing U.S. footprint, strong digital sales and higher margins are paired with a share price that still screens as below estimated cash flow value. Recent quarters show double digit revenue and earnings growth, with return on equity around 32% and net margins near 11%. At the same time, the stock trades on a higher P/E than many specialty retail peers, which raises questions about how much optimism is already in the price. In addition, active store expansion, a buyback program and bullish analyst targets sit alongside funding and execution risks, creating a company profile where the potential opportunity is notable but the investment case remains complex.

Aritzia’s accelerating U.S. expansion and high returns on equity are getting attention, but the real tension is how that growth lines up with its current valuation. Before deciding it is overhyped or overlooked, review the analyst forecasts for Aritzia

Stantec (TSX:STN)

Overview: Stantec is a Canadian consulting and engineering company that helps governments and businesses plan, design, and manage infrastructure projects, from water systems and transit lines to buildings and environmental services, across Canada, the U.S., and global markets.

Operations: Stantec generates about CA$6.6b in revenue across its core regions, with roughly CA$3.5b from the United States, CA$1.6b from Canada, and CA$1.6b from global operations.

Market Cap: CA$11.2b

Stantec catches attention in a cash flow focused screener because it combines a global infrastructure footprint with earnings growth that analysts expect to outpace the broader Canadian market, yet its current share price sits well below one estimate of fair value. Investors are watching a rising backlog of CA$9.0b, reaffirmed 2026 revenue guidance, and profit margins that improved to 7.4%, all while the stock trades on a lower P/E than many North American construction peers. The flip side is a high reliance on external debt and an upcoming CEO transition, which add financing and leadership risk. For investors weighing whether the current valuation gap fairly reflects those trade offs, Stantec offers a detailed case study in growth at a measured price.

Stantec’s rising CA$9.0b backlog and reaffirmed 2026 revenue guidance suggest investors may be underestimating how its current pricing compares with future contracts. Before the market fully connects those dots, review the DCF valuation analysis for Stantec

Avino Silver & Gold Mines (TSX:ASM)

Overview: Avino Silver & Gold Mines is a Vancouver based miner focused on acquiring, exploring, and advancing silver, gold, copper, and base metal deposits in Mexico, anchored by its 100% owned Avino Mine area in Durango and options over the Ana Maria and El Laberinto properties.

Operations: Avino Silver & Gold Mines generates about US$112.8m in revenue from gold and other precious metals, all from operations in Mexico.

Market Cap: CA$1.45b

Avino Silver & Gold Mines has attracted investor interest because its current share price sits below one estimate of future cash flow value. Recent Q1 2026 results show revenue of US$39.43m and net income of US$15.91m, which indicates strong profitability. Forecasts calling for earnings growth above 20% a year and higher measured and indicated resources after the latest reserve update may appeal to investors who want direct exposure to silver and gold. At the same time, a relatively high P/E, reliance on external borrowing, insider selling and recent shareholder dilution make this a more complex investment case, and investors need to weigh the cash flow potential against a higher risk profile.

Avino Silver & Gold Mines is showing strong profitability and higher measured resources, yet its higher P/E and funding risks hint that investors might be missing a key twist in the 3 key rewards and 3 important warning signs (1 is major!)

The three stocks here are only a starting point, and the full Undervalued Stocks Based On Cash Flows screener surfaced 17 more companies where cash flow potential and current pricing create equally compelling stories to investigate. Use Simply Wall St to identify and analyze the exact catalysts, cash flow profiles, and valuation gaps that matter most so you can focus on the highest conviction ideas for your watchlist.

Take Control of Your Investment Journey

If Aritzia or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Today?

Momentum can shift quickly as fresh stock ideas move from under the radar to full breakout. Scan these focused shortlists before the crowd catches up and consider them in your own research.

- Review companies turning early AI traction into profits by exploring the 63 profitable AI stocks that aren't just burning cash while the market is still pricing many peers on hope instead of cash flows.

- Strengthen your core holdings by checking the list of solid balance sheet and fundamentals (12 results) curated to highlight companies pairing sturdy finances with fundamentals that can support long term compounding.

- Explore potential precious metals opportunities by scanning the 33 elite gold producer stocks to see a curated view of producers with scale instead of chasing every headline spike.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com