Discover Daqo New Energy And 2 Other Growth Stocks With Strong Insider Confidence

In the last week, the United States market has stayed flat but it is up 19% over the past year with earnings forecasted to grow by 18% annually. In such a promising environment, growth companies with high insider ownership can be particularly appealing as they often indicate strong confidence from those who know the business best.

Top 10 Growth Companies With High Insider Ownership In The United States

| Name | Insider Ownership | Earnings Growth |

| Uxin (UXIN) | 34.3% | 69.4% |

| Upstart Holdings (UPST) | 14.1% | 60% |

| OS Therapies (OSTX) | 12.4% | 53.5% |

| Laird Superfood (LSF) | 16.7% | 115.9% |

| Karman Holdings (KRMN) | 15.6% | 52.6% |

| IREN (IREN) | 13.6% | 38.8% |

| ERock (EROC) | 20.1% | 56.3% |

| Corcept Therapeutics (CORT) | 10.9% | 48.9% |

| Cerebras Systems (CBRS) | 10.9% | 73.7% |

| AppLovin (APP) | 23.2% | 21.7% |

We'll examine a selection from our screener results.

Daqo New Energy (DQ)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Daqo New Energy Corp. manufactures and sells polysilicon to photovoltaic product manufacturers in China, with a market cap of approximately $839.06 million.

Operations: The company generates revenue primarily from its polysilicon segment, which accounted for $568.22 million.

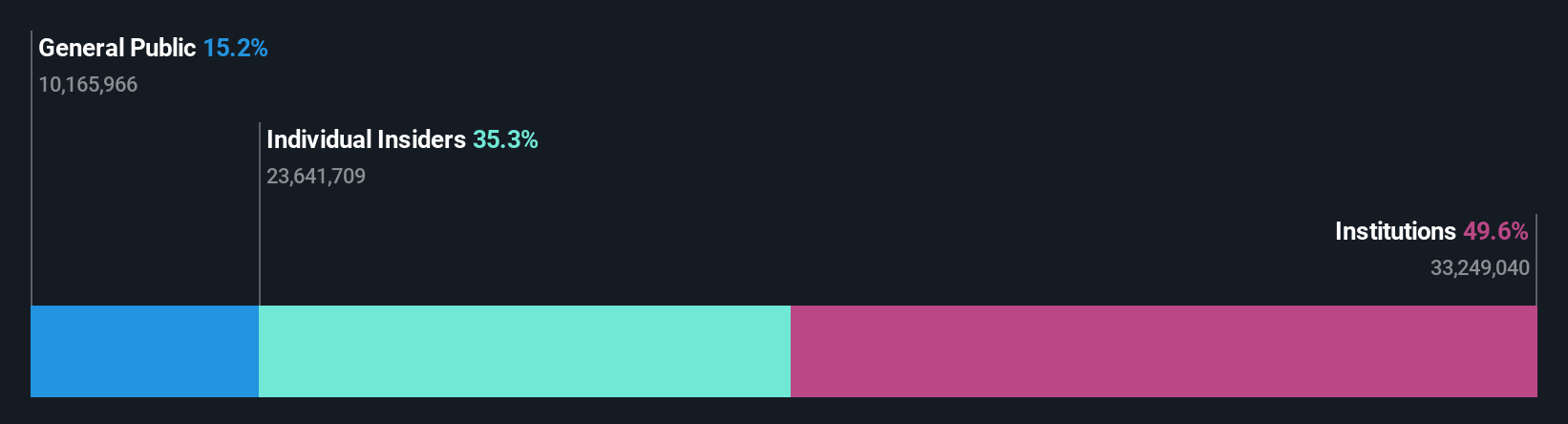

Insider Ownership: 36.2%

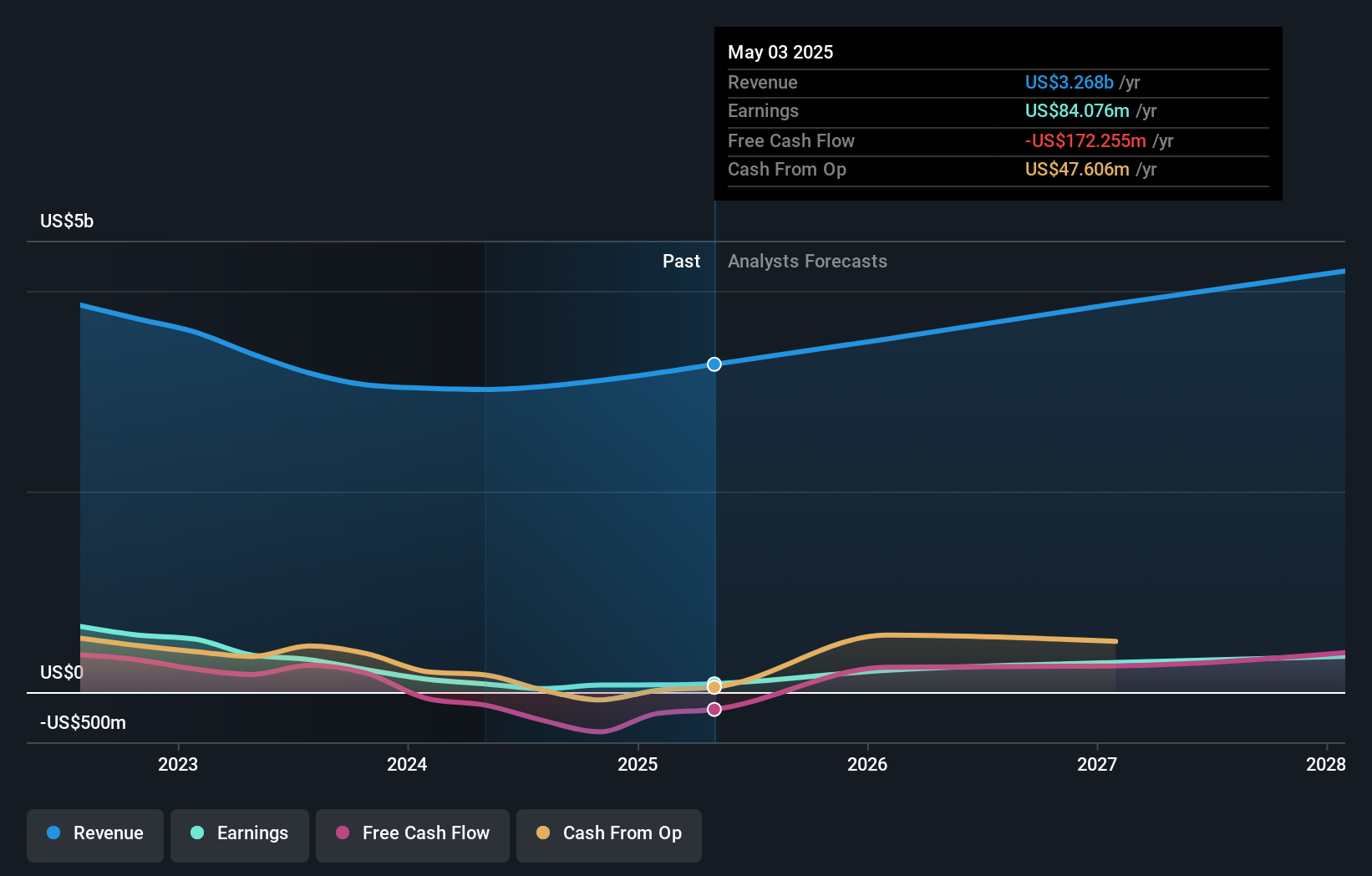

Daqo New Energy is positioned for significant growth, with its revenue projected to increase by 30.1% annually, outpacing the US market. Despite recent financial challenges, including a net loss of US$88.38 million in Q1 2026, the company anticipates becoming profitable within three years. The recent agreement to establish a new manufacturing base in Kunshan highlights its expansion strategy into next-generation energy solutions. Currently trading at 80.7% below estimated fair value, Daqo presents potential upside for investors focused on growth and insider ownership dynamics.

- Get an in-depth perspective on Daqo New Energy's performance by reading our analyst estimates report here.

- The valuation report we've compiled suggests that Daqo New Energy's current price could be quite moderate.

Pershing Square (PS)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Pershing Square Inc. operates as an alternative asset manager with a market cap of $14.01 billion.

Operations: The company generates revenue from its asset management segment, totaling $767.71 million.

Insider Ownership: 34.2%

Pershing Square shows potential for growth with substantial insider buying in the past three months, indicating confidence from within. Despite a volatile share price and a forecasted revenue decline of 1.6% annually over the next three years, earnings are expected to grow significantly at 56.4% per year, surpassing US market averages. Recent earnings revealed a net loss of US$147.59 million, but analysts predict a stock price rise of 22.3%.

- Click here to discover the nuances of Pershing Square with our detailed analytical future growth report.

- Insights from our recent valuation report point to the potential overvaluation of Pershing Square shares in the market.

RH (RH)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: RH operates as a retailer and lifestyle brand in the home furnishings market across several countries, including the United States, Canada, and parts of Europe, with a market cap of approximately $3.13 billion.

Operations: The company's revenue is primarily generated from its Restoration Hardware (RH) segment, contributing $3.23 billion, and the Waterworks segment, which adds $197.32 million.

Insider Ownership: 14.8%

RH's earnings are projected to grow significantly at 31.5% annually, outpacing the US market average of 18.2%, despite revenue growth being slower than the market. Insider activity shows more shares bought than sold recently, reflecting internal confidence amid financial challenges like a recent net loss of US$13.7 million in Q1 2026. RH's strategic collaborations and expansions, such as with Mercedes-AMG PETRONAS Formula One Team and new galleries in London and Milan, highlight its growth ambitions beyond traditional markets.

- Navigate through the intricacies of RH with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility RH's shares may be trading at a premium.

Seize The Opportunity

- Click through to start exploring the rest of the 164 Fast Growing US Companies With High Insider Ownership now.

- Seeking Other Investments? The end of cancer? These 33 emerging AI stocks are developing tech that will allow early idenification of life changing disesaes like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com