Humana Stock And 2 Government Supplier Shares Worth Watching Now

The Senate’s push to curb dividends and buybacks for Pentagon contractors has put traditional defense stocks under a cloud, but it also draws attention to a different corner of the market: larger non defense contractors and government suppliers that may not face the same direct constraints. For investors watching this policy debate, the question is which companies could be relatively better positioned if Section 815 becomes law, or even if it just keeps uncertainty elevated. This article looks at 3 stocks exposed to this news, helping you decide whether they deserve a closer look or a place on your avoid list.

Tennant (TNC)

Overview: Tennant is a long-established US company that designs and manufactures floor cleaning machines and technologies for commercial and industrial sites, from hospitals and stadiums to warehouses and retail stores, with offerings that include autonomous scrubbers, detergent-free cleaning systems and ongoing service and parts.

Operations: Tennant generates about US$1.2b in annual revenue from designing, manufacturing and selling equipment used in the maintenance of nonresidential surfaces across its global footprint.

Market Cap: US$1.46b

Tennant provides exposure to recurring, non defense government and commercial cleaning budgets at a time when defense contractors may face tighter dividend and buyback rules under Section 815. However, the picture is not straightforward. The company is investing in robotics and environmentally focused cleaning, targeting US$250m in robotics revenue by 2028, and analysts currently project strong earnings growth, but recent results show thin net margins at 2.6% and earnings that declined sharply last year. Heavy reliance on external funding, tariff pressures and weaker international performance add further risk. For investors weighing whether this mix of growth initiatives, capital returns and execution challenges is attractive in a policy sensitive market, Tennant’s profile may warrant further research.

Tennant’s push into robotics and greener cleaning is easy to focus on, but the real story may sit in how growth plans stack up against thin 2.6% margins and funding risks. The DCF valuation analysis for Tennant starts to unpack these issues.

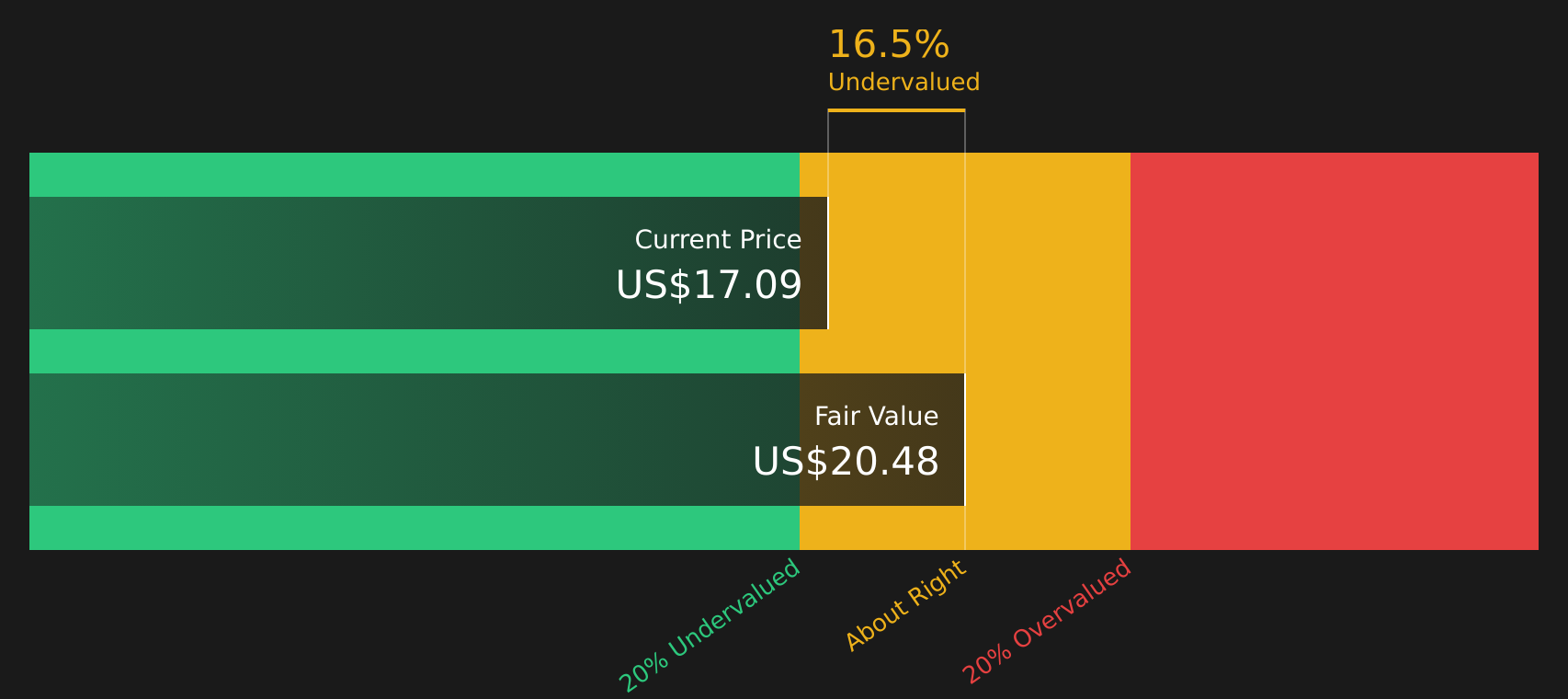

Humana (HUM)

Overview: Humana is a large US health insurer focused on Medicare Advantage and related government backed programs, combining medical and specialty insurance with senior focused primary care, home health, pharmacy and post acute care services under its CenterWell brands.

Operations: Humana generates about US$131.7b in Insurance revenue and US$23.5b from CenterWell, with small corporate eliminations of US$18.0b, almost all from US operations totaling roughly US$137.3b.

Market Cap: US$47.1b

Humana stands out in this screener because it is deeply tied to US government healthcare spending rather than defense budgets, so Section 815 is less of a direct overhang while the stock still reflects policy risk through Medicare Advantage rates, Stars scores and coding changes. The company is heavily investing in AI driven efficiency and clinical programs to sharpen margins. Net profit margins sit at about 0.8% after a recent one off loss of US$718m and earnings have fallen more than 20% over the past year. With analysts still forecasting strong earnings growth and recent broker upgrades pointing to potential margin improvement, the tension between its growth plans, thin margins and elevated P/E gives investors plenty to weigh up around Humana’s longer term risk reward profile.

Humana’s thin 0.8% margins and heavy Medicare exposure could be masking a very different earnings story once AI driven efficiency and care programs take effect, and the analyst forecasts for Humana hints at where that tension really leads

Luxfer Holdings (LXFR)

Overview: Luxfer Holdings is a specialty industrial manufacturer that produces high performance gas cylinders and advanced magnesium and zirconium based materials used in areas such as emergency response, healthcare, alternative fuel transport, aerospace, defense and space applications across multiple regions worldwide.

Operations: Luxfer generates US$189.2m of revenue from its Elektron segment and US$175.5m from Gas Cylinders, with a small segment adjustment of US$6.8m.

Market Cap: US$456m

Luxfer Holdings sits in an interesting spot for investors watching Section 815, because it supplies municipalities and federal agencies and has aerospace and defense exposure, yet is not a pure Pentagon contractor and so is less directly tied to dividend and buyback restrictions. The company is leaning into higher value decarbonization, hydrogen and aerospace materials while consolidating production and exiting lower margin activities. This could matter for margins that currently sit at 3.1% and dividends that are not fully covered by earnings. At the same time, guidance for higher 2026 revenue, a recent quarterly profit and a P/E that screens as expensive versus machinery peers but below its own estimated fair P/E all point to a more complex risk reward balance than headline multiples suggest.

Luxfer’s higher value materials push could be masking a very different risk reward profile, and the 2 key rewards and 3 important warning signs might be where the real inflection point in the story starts to show.

The three stocks here are just a starting point, and the full Non-Defense Contractors and Government Suppliers screener surfaces 44 more companies with equally compelling government supplier narratives that you have not seen yet. Use Simply Wall St to unlock that broader list, and then identify and analyze the specific catalysts, policy exposure and business profiles that align with your highest conviction ideas.

Take Control of Your Investment Journey

If Tennant or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Alternatives Before Everyone Else?

Fresh stock ideas can move from quiet to breakout fast, and by the time momentum is flying you are already caught chasing. Scan these under the radar picks now and consider acting early.

- Spot potential turnaround stories with balance sheet strength by scanning the curated list of solid balance sheet and fundamentals (47 results) before the crowd starts hunting for quality defensives.

- Explore structural trends in automation and efficiency by reviewing companies in the hand picked 32 robotics and automation stocks while valuations may still reflect older assumptions.

- Review opportunities related to power grid upgrades by assessing infrastructure stocks inside the targeted 34 power grid technology and infrastructure stocks while the story is still developing.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com