Asian Market Value Picks: 3 Stocks Estimated Below Intrinsic Worth

Amid renewed geopolitical tensions and energy market volatility, Asian markets have experienced mixed performances, with some sectors showing resilience while others face challenges. In this environment, identifying undervalued stocks—those trading below their intrinsic worth—can present unique opportunities for investors seeking value in a complex market landscape.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | HK$19.28 | HK$38.12 | 49.4% |

| Rakuten Bank (TSE:5838) | ¥5809.00 | ¥11507.47 | 49.5% |

| Rakus (TSE:3923) | ¥1019.00 | ¥2014.24 | 49.4% |

| Moshi Moshi Retail Corporation (SET:MOSHI) | THB39.00 | THB75.90 | 48.6% |

| Laopu Gold (SEHK:6181) | HK$385.20 | HK$746.36 | 48.4% |

| Huatu Cendes (SZSE:300492) | CN¥23.09 | CN¥45.69 | 49.5% |

| GreenEnergy (TSE:1436) | ¥1387.00 | ¥2707.83 | 48.8% |

| CSPC Innovation Pharmaceutical (SZSE:300765) | CN¥37.55 | CN¥74.24 | 49.4% |

| Citicore Renewable Energy (PSE:CREC) | ₱4.39 | ₱8.48 | 48.2% |

| BEAUTY GARAGE (TSE:3180) | ¥1438.00 | ¥2875.79 | 50% |

Let's dive into some prime choices out of the screener.

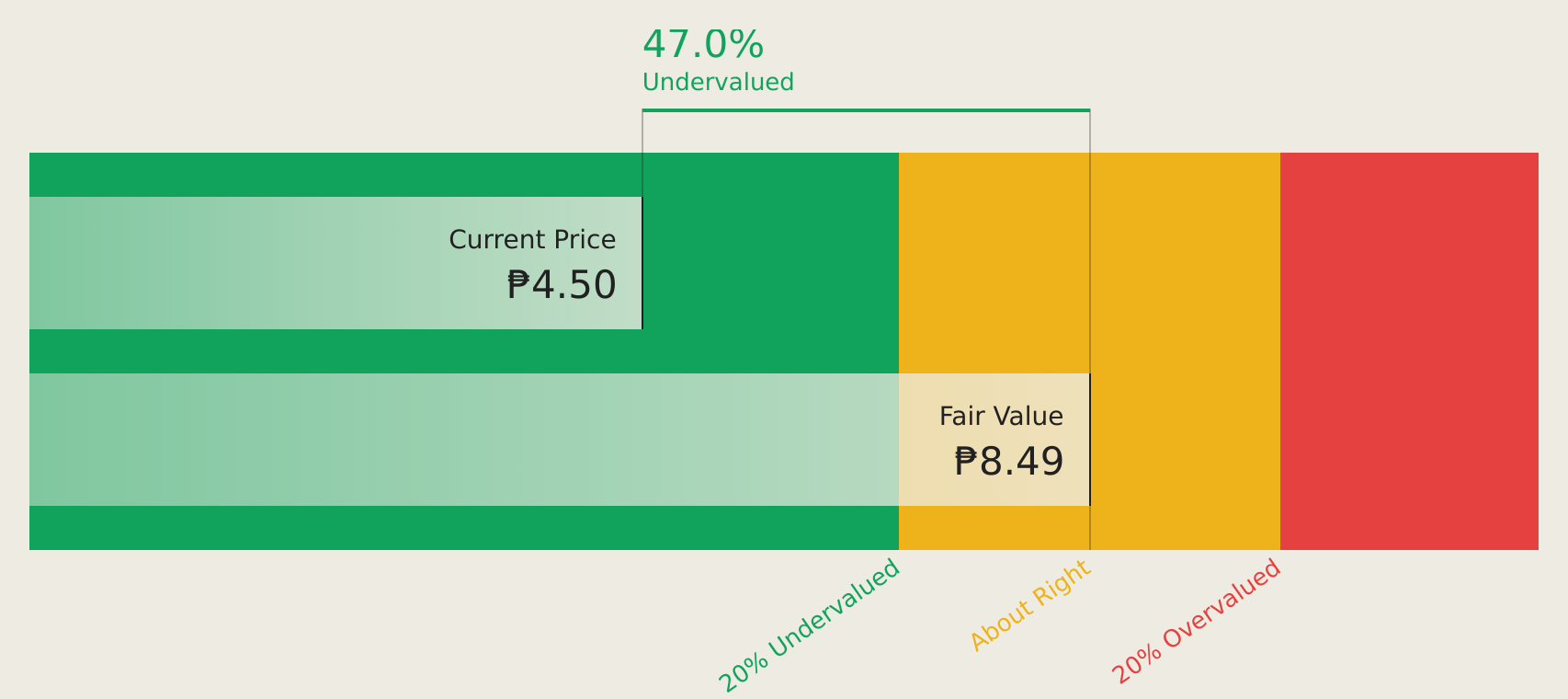

Citicore Renewable Energy (PSE:CREC)

Overview: Citicore Renewable Energy Corporation is a renewable energy developer in the Philippines, focusing on solar, run-of-river hydro, and wind energy platforms, with a market cap of ₱48.99 billion.

Operations: The company generates revenue primarily through its Power segment, which accounts for ₱5.41 billion, and its REIT segment, contributing ₱1.87 billion.

Estimated Discount To Fair Value: 48.2%

Citicore Renewable Energy Corporation is trading at ₱4.39, significantly below its estimated future cash flow value of ₱8.48, suggesting it is undervalued based on cash flows. Despite a recent decline in sales to PHP 1.14 billion, net income rose to PHP 272.43 million, indicating high-quality earnings growth of 47.5% over the past year. With expected revenue growth of 42.6% annually and robust profit forecasts, the company shows strong potential for future financial performance amidst ongoing executive changes and strategic amendments to its Articles of Incorporation aimed at enhancing corporate governance and flexibility for fundraising activities.

- According our earnings growth report, there's an indication that Citicore Renewable Energy might be ready to expand.

- Take a closer look at Citicore Renewable Energy's balance sheet health here in our report.

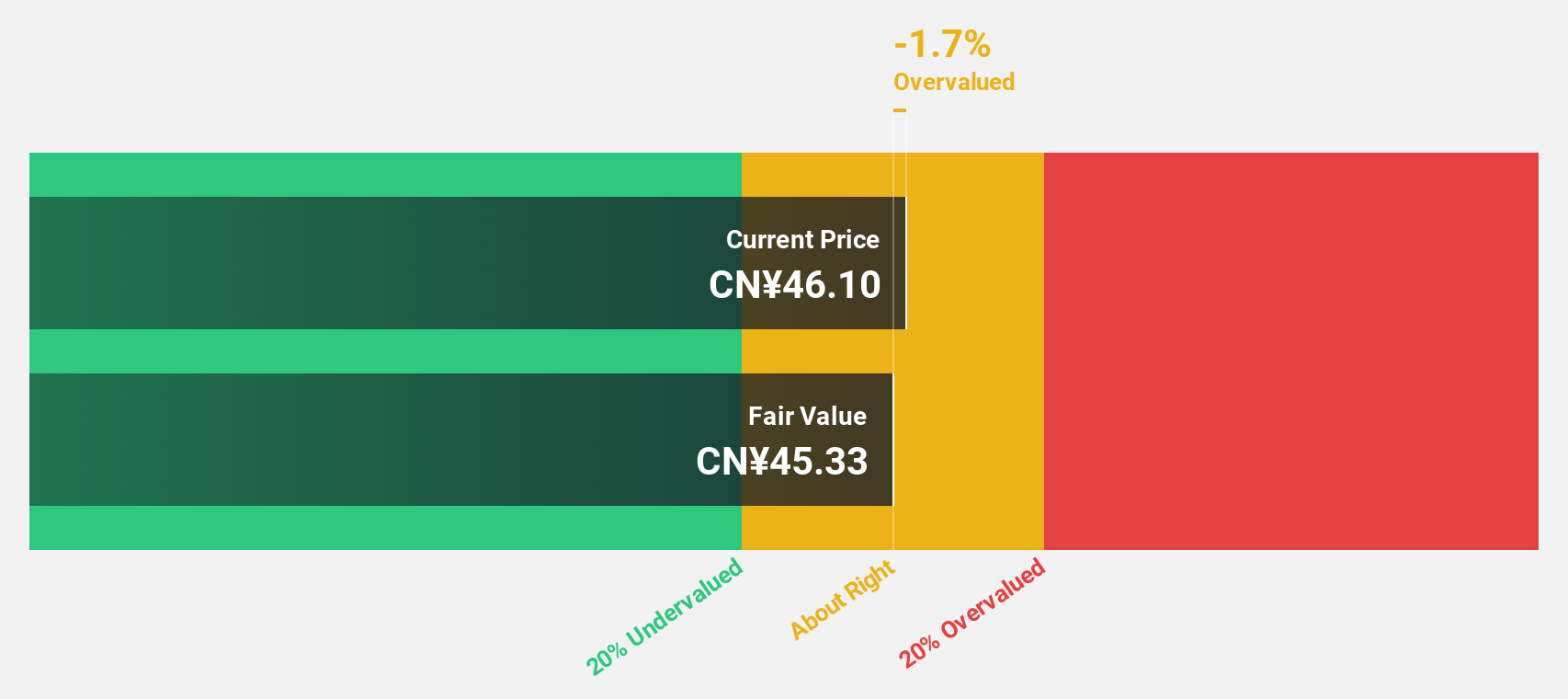

Shanghai Aohua Photoelectricity Endoscope (SHSE:688212)

Overview: Shanghai Aohua Photoelectricity Endoscope Co., Ltd. operates in the medical device industry, specializing in the development and production of endoscopic equipment, with a market cap of CN¥3.75 billion.

Operations: The company's revenue is primarily derived from its medical devices segment, totaling CN¥787.64 million.

Estimated Discount To Fair Value: 20.2%

Shanghai Aohua Photoelectricity Endoscope is trading at CN¥27.87, below its estimated future cash flow value of CN¥34.93, highlighting undervaluation based on cash flows. The company reported Q1 2026 sales of CNY 137.5 million with a reduced net loss of CNY 24.43 million compared to the previous year. Despite low forecasted return on equity, earnings are expected to grow significantly at 61.1% annually over the next three years, surpassing market averages and indicating potential for robust financial improvement.

- The growth report we've compiled suggests that Shanghai Aohua Photoelectricity Endoscope's future prospects could be on the up.

- Get an in-depth perspective on Shanghai Aohua Photoelectricity Endoscope's balance sheet by reading our health report here.

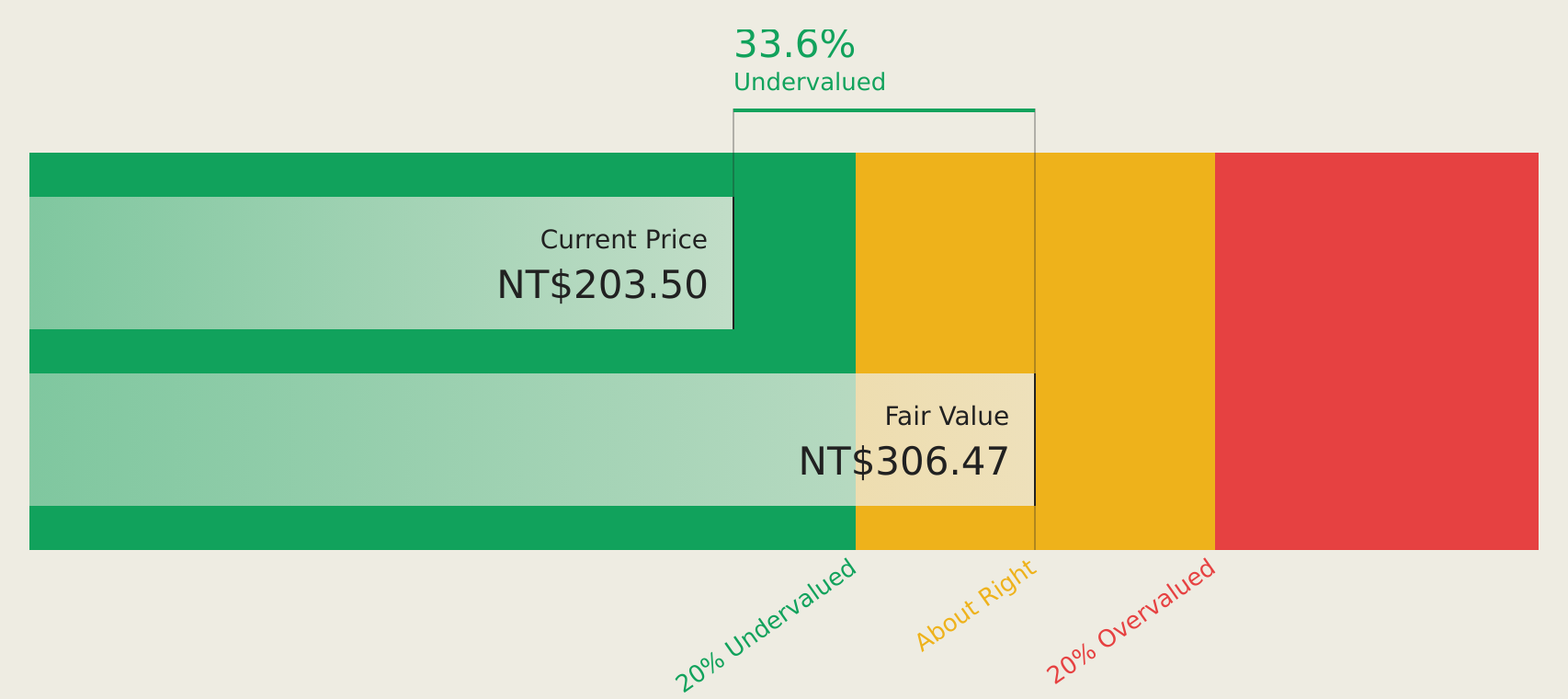

ASROCK Incorporation (TWSE:3515)

Overview: ASROCK Incorporation designs, develops, and sells motherboards across Asia, Europe, America, and internationally with a market cap of NT$26.25 billion.

Operations: The company's revenue segment consists of NT$50.74 billion from motherboards and other products.

Estimated Discount To Fair Value: 30.5%

ASROCK Incorporation is trading at TWD 212.5, significantly below its estimated future cash flow value of TWD 305.96, suggesting undervaluation. The company reported strong Q1 2026 earnings with sales of TWD 13.37 billion and net income of TWD 511.87 million, reflecting growth from the previous year. Earnings are forecast to grow annually by over 25%, outpacing the Taiwan market average, although its dividend yield of 5.18% isn't well-covered by free cash flows.

- The analysis detailed in our ASROCK Incorporation growth report hints at robust future financial performance.

- Navigate through the intricacies of ASROCK Incorporation with our comprehensive financial health report here.

Make It Happen

- Navigate through the entire inventory of 186 Undervalued Asian Stocks Based On Cash Flows here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com