3 AI Infrastructure Stocks With Big European Operations On Investors’ Radar

Intel’s planned €5b expansion of its Irish semiconductor facilities has put fresh attention on US-listed multinationals that already run large European operations. For investors, this kind of cross-Atlantic footprint can cut both ways, offering potential exposure to local policy support as well as regional execution risks. With AI data-centre demand and the EU’s chip ambitions in the spotlight, it is worth asking which stocks could be helped most by this wave of investment and manufacturing focus. Below, three positively exposed stocks from our screener are unpacked so you can decide whether they deserve a place on your watchlist.

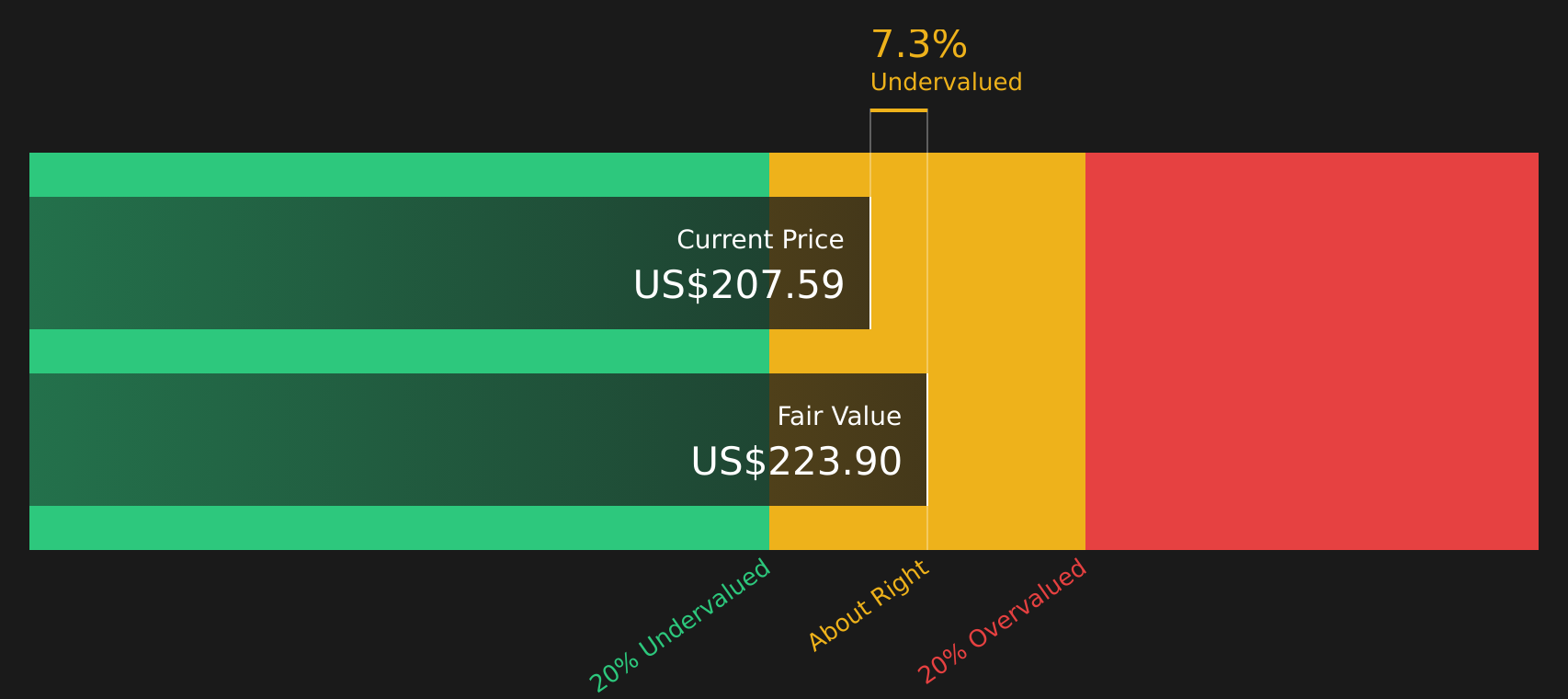

Corning (GLW)

Overview: Corning is a materials science company that supplies fiber optic cables and connectivity hardware for telecom and AI data centres, as well as advanced glass and ceramics used in consumer electronics, automotive, life sciences and other industrial applications across North America, Europe and Asia.

Operations: Corning generates about US$6.8b from Optical Communications and around US$1.8b from Automotive, alongside an aggregate segment adjustment of roughly US$8.5b and an unallocated constant currency impact of US$753m.

Market Cap: US$164.3b

For investors tracking Intel’s EU expansion and the AI buildout, Corning offers a different angle on the same story, supplying the glass and fiber that sit behind higher chip and data-centre spending while also running advanced manufacturing sites across Europe that can align with local incentive schemes. The company is leaning into Gen AI connectivity, with management highlighting strong interest from hyperscalers and multi decade fiber agreements linked to large U.S. and global customers, yet it also carries elevated debt, a rich P/E and meaningful reliance on non GAAP metrics. Add in rapid earnings growth, active buybacks and tariff exposure that is partly cushioned by producing close to customers, and Corning becomes a complex opportunity that warrants a closer look.

Corning’s multi decade fiber commitments and AI data centre exposure look powerful, but the mix of rich P/E, debt and non GAAP reliance deserves context that many investors may be missing. Start with the 2 key rewards and 3 important warning signs

Viavi Solutions (VIAV)

Overview: Viavi Solutions provides test, monitoring, assurance and security tools that help telecom operators, cloud providers, data centers, aerospace and defense customers build and maintain complex high speed networks, and also supplies optical security and 3D sensing products used in anti counterfeiting, industrial and automotive applications.

Operations: Viavi Solutions generates about US$1.0b from Network and Service Enablement and roughly US$327.6m from Optical Security and Performance Products, with revenue spread across the United States, EMEA, Greater China and the wider Asia Pacific and Americas regions.

Market Cap: US$10.6b

Intel’s €5b AI chip expansion in Ireland helps explain why Viavi Solutions is attracting attention, as the company sits behind many of the fiber, Ethernet and timing upgrades that AI data centres and European carriers now require. Viavi is rolling out tools for 400G, 800G and 1.6T optical testing, Ultra Ethernet Transport validation and AI focused security and timing products, which all tie into that rising demand. At the same time, the stock combines this growth story with ongoing losses, heavy use of external funding and recent insider selling. Analysts are expecting a return to profitability and strong revenue growth. However, the balance sheet and earnings history still raise questions, and Viavi appears to be a higher risk AI infrastructure play that may warrant closer scrutiny before you decide how it fits your portfolio.

Viavi’s AI and high speed networking story appears to be gaining momentum, yet losses and funding needs still hang over the stock. Before opinions harden, see how the 2 key rewards and 3 important warning signs (1 is major!) might shift the picture.

Sanmina (SANM)

Overview: Sanmina is an electronics manufacturing services company that designs, builds and services complex hardware for original equipment manufacturers, from circuit boards and subassemblies through to full systems, across industrial, medical, defense, automotive, communications and cloud infrastructure markets worldwide.

Operations: Sanmina generates about US$9.7b from Integrated Manufacturing Solutions and roughly US$1.8b from Components, Products and Services, with intersegment revenue of US$129.6m.

Market Cap: US$11.2b

Sanmina stands out in the screener because it sits in the slipstream of rising AI and data centre spending, yet still offers exposure to industrial, medical and defense hardware where electronics content is rising. Recent commentary highlights new AI focused factories, expanded optical and liquid cooling capabilities and the planned ZT Systems acquisition, which could significantly reshape its size and role in accelerated compute infrastructure. At the same time, the stock trades modestly below some fair value estimates and below peer average P/Es. Set against this, customer concentration, a large recent one off loss, reliance on external funding and heavy integration work mean execution missteps could quickly affect margins and earnings. This makes it important to consider how the risk and reward really stack up for Sanmina’s next chapter.

Sanmina’s AI factories, liquid cooling push and ZT Systems deal could be reshaping the company faster than the market realises. However, the real twist sits in the 2 key rewards and 2 important warning signs

The three stocks covered here are just a starting point. The full US-Listed Multinational Companies with Significant European Operations idea surfaces 37 more companies that carry equally compelling cross Atlantic narratives in the US-Listed Multinational Companies with Significant European Operations screener. With Simply Wall St, you can quickly identify, filter and analyze the specific catalysts and narratives highlighted in this article so you can focus on the highest conviction opportunities across this group.

Take Control of Your Investment Journey

If Sanmina or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond These Stocks?

Some of the strongest breakout setups get spotted early, then move fast. Before momentum really flies and the best entry points get caught by the crowd, act now.

- Chase potential early breakouts in resilient companies by scanning a curated 80 resilient stocks with low risk scores that still show price and fundamentals holding up while the window looks open.

- Spot under the radar momentum in future facing automation plays by running through a focused list of 32 robotics and automation stocks before prices reflect the full story.

- Target fresh infrastructure trends supporting the AI buildout by working through a hand picked 34 power grid technology and infrastructure stocks while these ideas are still flying under most radars.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com