Asian Growth Companies With Strong Insider Confidence July 2026

As global markets navigate through geopolitical tensions and energy market volatility, Asia's growth stocks are capturing attention with their potential resilience and performance. In this environment, companies demonstrating high insider ownership can be particularly appealing as it often signals strong confidence from those closest to the business.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Zhejiang Taotao Vehicles (SZSE:301345) | 27.9% | 31.5% |

| Shanghai Biren Technology (SEHK:6082) | 11% | 116.9% |

| Seojin SystemLtd (KOSDAQ:A178320) | 22% | 110.6% |

| SEERS (KOSDAQ:A458870) | 33.2% | 41.5% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Fulin Precision (SZSE:300432) | 10.4% | 60.7% |

Below we spotlight a couple of our favorites from our exclusive screener.

Xiaomi (SEHK:1810)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Xiaomi Corporation is an investment holding company involved in the development and sales of smartphones both in Mainland China and internationally, with a market cap of approximately HK$663.95 billion.

Operations: The company's revenue segments include CN¥180.10 billion from smartphones, CN¥115.54 billion from IoT and lifestyle products, CN¥107.35 billion from smart EV, AI and other new initiatives, CN¥37.83 billion from internet services, and CN¥4.31 billion from other related businesses.

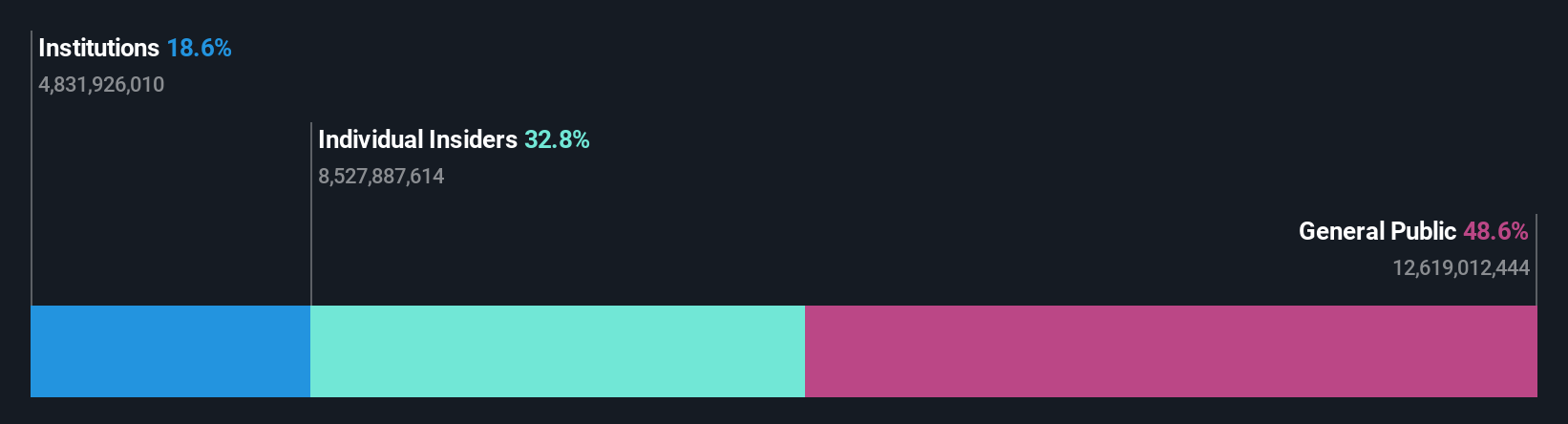

Insider Ownership: 33.2%

Revenue Growth Forecast: 13.9% p.a.

Xiaomi, a growth company with high insider ownership, is expected to see annual earnings growth of 20.2%, outpacing the Hong Kong market's 12.6%. However, recent financials show a decline in Q1 2026 sales and net income compared to the previous year. Despite this, Xiaomi trades at a good value relative to peers and is priced below its estimated fair value. The company recently amended its bylaws and appointed Summer Peng as general manager for Korea to boost market presence.

- Navigate through the intricacies of Xiaomi with our comprehensive analyst estimates report here.

- The analysis detailed in our Xiaomi valuation report hints at an deflated share price compared to its estimated value.

Xi'an Bright Laser TechnologiesLtd (SHSE:688333)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Xi'an Bright Laser Technologies Co., Ltd. provides metal additive manufacturing solutions in China and has a market cap of CN¥27.75 billion.

Operations: Xi'an Bright Laser Technologies Co., Ltd. generates revenue through its metal additive manufacturing solutions in China.

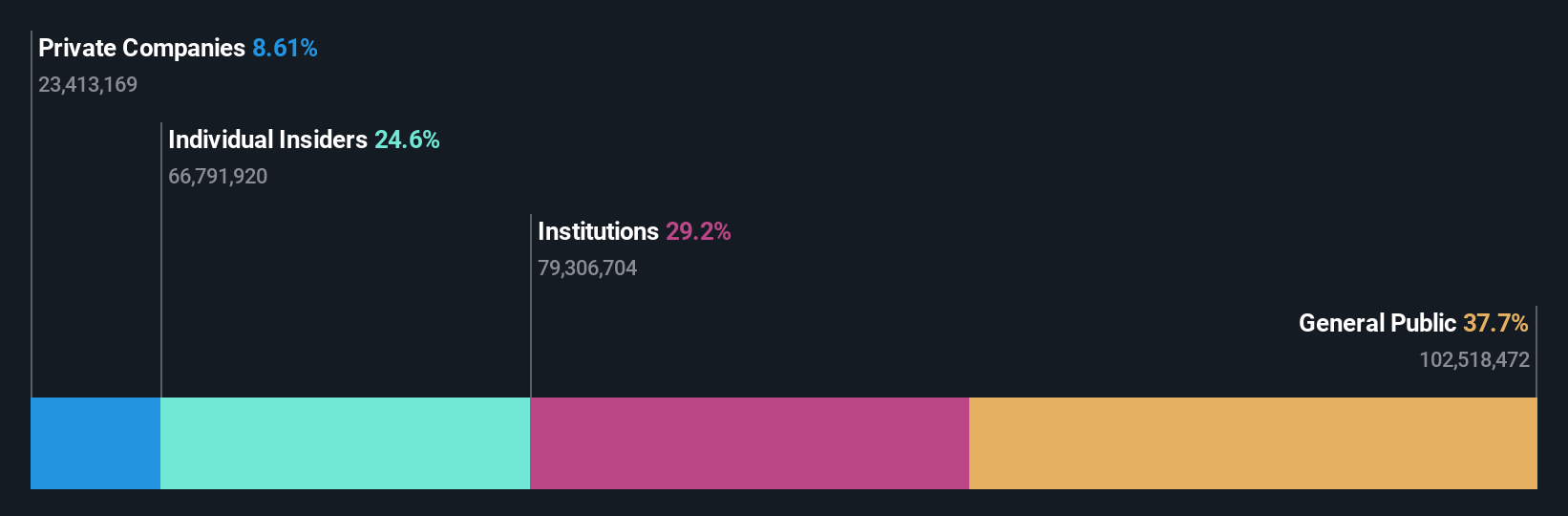

Insider Ownership: 24.5%

Revenue Growth Forecast: 33.4% p.a.

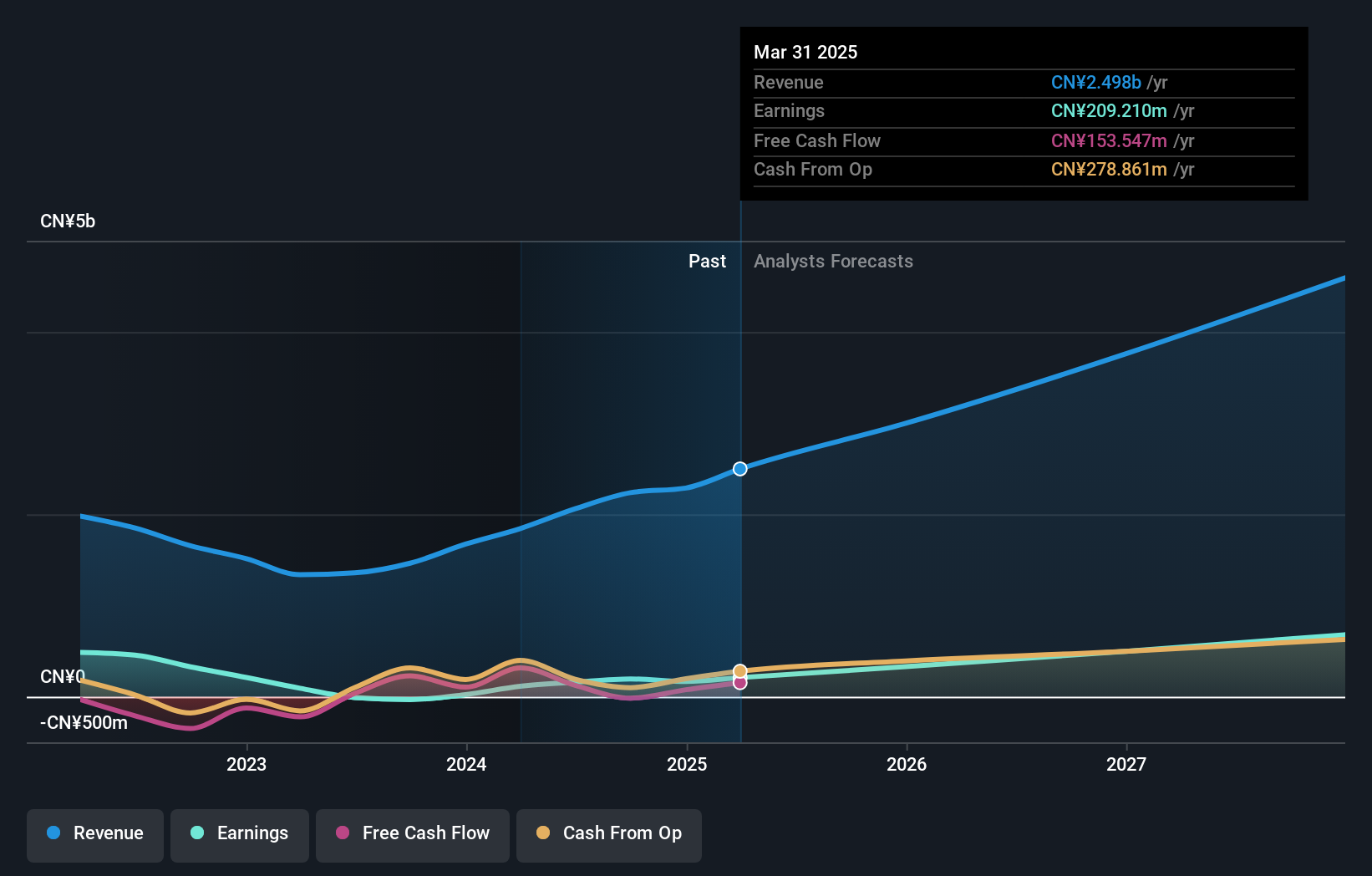

Xi'an Bright Laser Technologies demonstrates strong growth potential with earnings projected to rise 33.2% annually, surpassing the broader Chinese market's forecast. Recent financials reveal a significant turnaround, with Q1 2026 net income of CNY 16.78 million compared to a loss previously. Despite high share price volatility and low future return on equity projections, the company's revenue is expected to grow at an impressive rate of 33.4% per year, indicating robust expansion prospects in the coming years.

- Click to explore a detailed breakdown of our findings in Xi'an Bright Laser TechnologiesLtd's earnings growth report.

- Our expertly prepared valuation report Xi'an Bright Laser TechnologiesLtd implies its share price may be too high.

Allwinner TechnologyLtd (SZSE:300458)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Allwinner Technology Co., Ltd. is involved in the research, design, development, manufacture, and sale of intelligent application system-on-a-chip (SoC), analog components, and wireless connectivity integrated circuits both in China and internationally, with a market cap of approximately CN¥39.65 billion.

Operations: The company's revenue primarily comes from its Integrated Circuit Design segment, which generated CN¥3.13 billion.

Insider Ownership: 36.6%

Revenue Growth Forecast: 17.9% p.a.

Allwinner Technology Ltd. shows promising growth potential with earnings expected to increase by 28.3% annually, outpacing the Chinese market's forecast. Recent Q1 2026 results highlight strong performance, with net income rising to CNY 203.03 million from CNY 91.55 million a year ago, despite an unstable dividend track record and low future return on equity projections of 16.4%. The company's price-to-earnings ratio remains favorable compared to industry averages, supporting its growth narrative in the semiconductor sector.

- Take a closer look at Allwinner TechnologyLtd's potential here in our earnings growth report.

- Upon reviewing our latest valuation report, Allwinner TechnologyLtd's share price might be too optimistic.

Taking Advantage

- Unlock our comprehensive list of 474 Fast Growing Asian Companies With High Insider Ownership by clicking here.

- Looking For Alternative Opportunities? Uncover 27 companies that survived and thrived after COVID and have the right ingredients to survive Trump's tariffs.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com