Energy Transfer (ET) Could Be 17% Below Fair Value On $1.7b Notes Pricing

Energy Transfer (ET) has just priced more than $1.7b in junior subordinated notes, a financing move tied to redeeming preferred units, refinancing existing debt, and supporting general partnership purposes.

See our latest analysis for Energy Transfer.

Against this backdrop of fresh junior subordinated notes, Energy Transfer’s share price has eased 0.7% over the last day but remains higher over the past week and month, with an 18.5% year to date share price return and strong multi year total shareholder returns.

If you are looking beyond Energy Transfer and want more ideas in the wider energy infrastructure space, this could be a good moment to scan 34 power grid technology and infrastructure stocks

Bulls see Energy Transfer’s $1.7b junior subordinated notes as smart balance sheet work, while bears see extra leverage risk. The key question is which side the current valuation and cash generation profile really support next.

Most Popular Narrative: 16.7% Undervalued

The most followed narrative currently pegs Energy Transfer’s fair value at about $23.59 per unit versus the last close of $19.66, framing the latest junior subordinated notes within a wider long term cash flow story.

Aggressive organic growth project backlog (many expected to deliver mid teen returns from 2026 onward) and a proven history of successful M&A provide strong forward visibility into distributable cash flow and earnings growth, likely supporting valuation re rating over time.

Read the complete narrative. Read the complete narrative.

Want to see what underpins that higher fair value for Energy Transfer? The narrative leans on projected revenue expansion, fatter margins, and a richer earnings multiple than the sector. The tension sits in how those assumptions compare with your own view of midstream growth and future cash generation.

Result: Fair Value of $23.59 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that higher fair value narrative for Energy Transfer could be challenged if large projects face cost overruns or if long term natural gas demand proves weaker than expected.

Find out about the key risks to this Energy Transfer narrative.

Another View: What Multiples Say About Energy Transfer

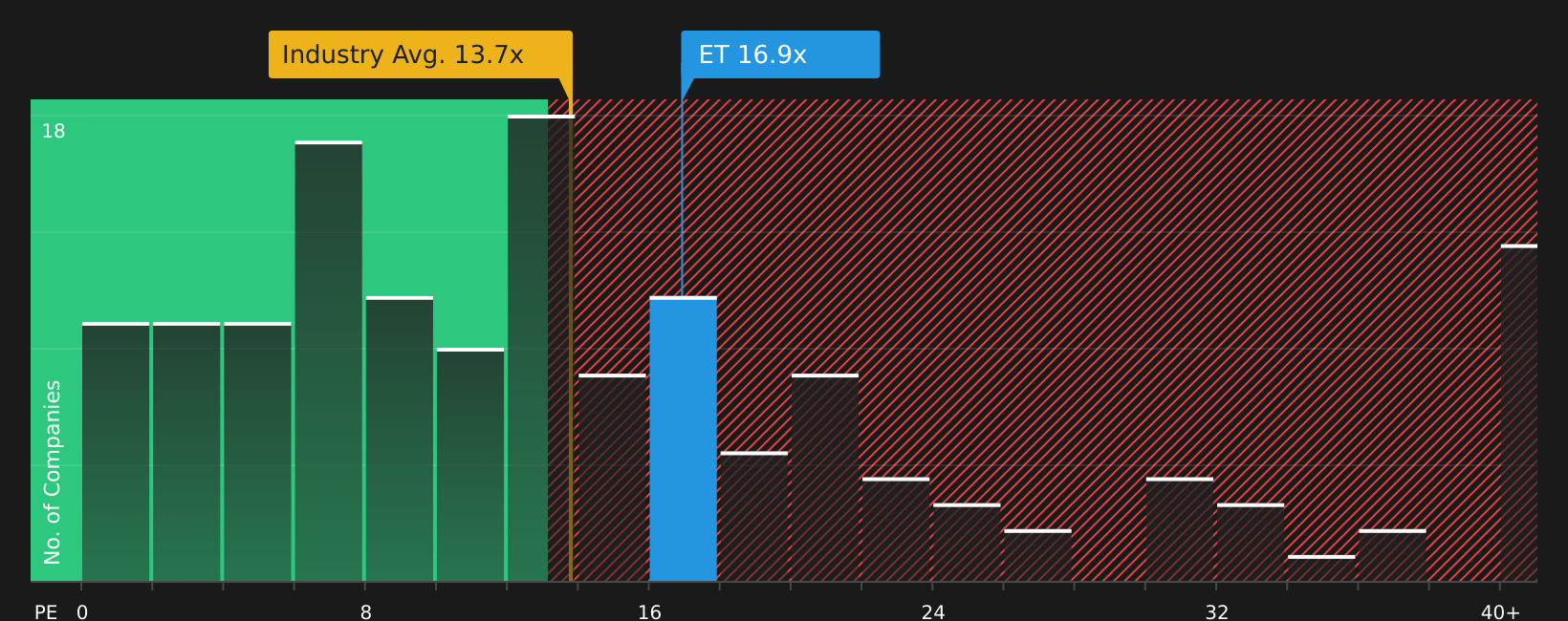

While the popular narrative leans on cash flows and analyst targets to argue that Energy Transfer is undervalued, the current P/E of 16.5x sends a more mixed signal. It is higher than the US Oil and Gas industry average of 13.4x, yet below the peer average of 18.9x and well under the fair ratio estimate of 25.6x, which suggests the market could shift toward richer pricing if sentiment improves. For you as an investor, that gap can look like either a valuation cushion or a sign that expectations already bake in a fair amount of good news. Which side do you think you are on?

See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

If the mix of optimism and concern around Energy Transfer feels finely balanced, it is worth reviewing the data and forming your own view quickly. To see in one place what investors currently view as key positives and key watchpoints, start with 3 key rewards and 2 important warning signs

Looking for more investment ideas beyond Energy Transfer?

If Energy Transfer has sharpened your focus on opportunities, do not stop here. Use the Simply Wall Street Screener to quickly surface stocks that better match your criteria.

- Target potential mispricing by scanning companies that look attractively valued on fundamentals with the help of the 45 high quality undervalued stocks.

- Strengthen your income stream by reviewing stocks that combine higher yields with sturdier payouts through the 9 dividend fortresses.

- Prioritize resilience by focusing on companies with healthier finances using the 79 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com