UK Recruitment Stocks That Could Gain From The New Switzerland Trade Deal

The new £5.2b UK Switzerland trade deal puts services squarely in the spotlight, with easier travel, visa free short stays and lower roaming costs all aimed at making cross border business simpler. For UK listed financial and professional services stocks, that shift could change how investors think about overseas earnings potential and operational risk. This article picks out three stocks from a UK Financial and Professional Services Stocks screener that appear especially exposed to these developments and explains why the news might matter to their long term story, whether you are looking for opportunity or reasons to stay cautious.

Staffline Group (AIM:STAF)

Overview: Staffline Group is a UK and Ireland focused recruitment and outsourced HR specialist that supplies large scale workforces to food processing, manufacturing, e retail, driving and logistics clients, as well as permanent recruitment and managed transport services.

Operations: Staffline Group generates around £1.0b from Recruitment GB and £102.1m from Recruitment Ireland, with £1.1b of revenue reported across the UK and the Republic of Ireland.

Market Cap: £43.4m

Staffline Group sits at the intersection of tight UK labour markets and the new UK Switzerland services deal, where easier travel, lower roaming costs and visa free short stays could support extra cross border projects that require outsourced staffing and HR support. Analysts currently expect earnings and revenue growth, yet margins remain thin at around 0.5% and funding is entirely reliant on external borrowing, so balance sheet risk cannot be ignored. Add in significant recent insider selling and governance questions, and the result is a small cap that combines potential upside with clear pressure points that investors may wish to examine in more detail.

Staffline Group’s thin 0.5% margins and reliance on borrowing could be masking a bigger story about how much pressure the balance sheet can really absorb before growth ambitions hit a wall, and the Staffline Group financial health report might be where that tension finally comes into focus.

PageGroup (LSE:PAGE)

Overview: PageGroup is a global recruitment consultancy that matches professionals with employers across roles ranging from junior staff to senior executives, operating through brands such as Michael Page, Page Personnel, Page Executive and Page Outsourcing. It supports companies with permanent, temporary, contract and outsourced hiring needs across multiple sectors and regions.

Operations: PageGroup generates approximately £1.6b from recruitment services, with revenue spread across the Americas (£282.8m), Asia Pacific (£215.2m), the UK (£234.7m) and EMEA (£863.9m).

Market Cap: £398.4m

PageGroup sits in a favourable position within the new UK Switzerland services deal, because easier travel, visa free short stays and lower roaming costs directly support cross border hiring in finance and other professional sectors where the group already has established client relationships. Analysts expect earnings growth from a low base, while revenue is forecast to be broadly flat and recent profit margins are 0.6%. This underlines how much the outlook depends on improved conversion rates, cost savings and higher value placements. The 6.67% dividend yield is not fully covered by earnings and the shares trade on a high P/E, so investors may wish to consider whether this mix of growth potential, income and risk is reflected appropriately in the current valuation.

PageGroup’s mix of flat revenue, slim 0.6% margins and a 6.67% dividend yield suggests the headline story might be incomplete. The analysis report for PageGroup could highlight where income appeal and valuation risk really meet.

Robert Walters (LSE:RWA)

Overview: Robert Walters is a global recruitment consultancy that connects employers with professionals across fields such as finance, technology, legal, engineering, healthcare and HR, while also offering executive search, interim placements and talent advisory services. Alongside traditional recruitment, it provides outsourcing and consultancy solutions that help companies manage wider workforce and talent needs.

Operations: Robert Walters generates about £609.8m from Specialist Professional Recruitment and £171.3m from recruitment outsourcing, with revenue spread across Asia Pacific (£375.0m), the United Kingdom (£180.6m), Europe (£194.5m) and the Rest of World (£31.0m).

Market Cap: £55.4m

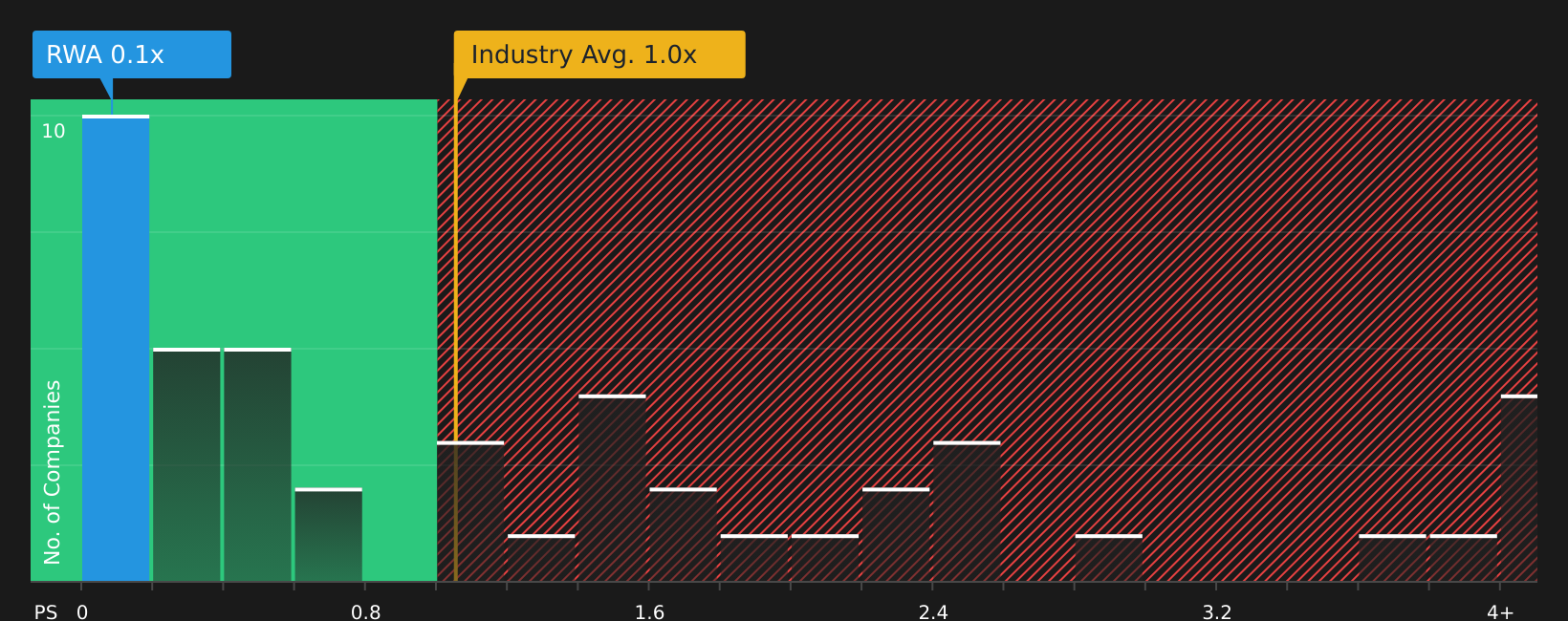

Robert Walters sits squarely in the crosshairs of the new UK Switzerland services deal, because smoother travel, visa free short stays and lower roaming costs directly affect how easily finance and professional clients move people across borders, and how often they need outsourced recruitment and advisory support. The stock combines a low P/S multiple and large upside to one fair value estimate, with clear risks around current losses, reliance on permanent placements and higher risk external borrowing. For investors who think AI driven efficiencies, cost savings and more flexible staffing solutions can shift margins over time, the key question is whether the current valuation already reflects those potential payoffs or still leaves room for mispricing.

Robert Walters’ low P/S ratio and reliance on permanent placements hint at a story investors may be underpricing. The full narrative for Robert Walters could show whether today’s valuation is quietly masking a much bigger twist.

The three recruitment stocks in this article are only a starting point, with the full UK Financial and Professional Services Stocks screener surfacing 17 more UK listed financial and professional services companies that each carry their own potentially important narrative around cross border business and trade. Use Simply Wall St to identify, analyze and filter for the specific catalysts, balance sheet traits and earnings profiles that matter most so you can focus on the highest conviction ideas from that wider group.

Take Control of Your Investment Journey

If PageGroup or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About Alternative Stock Paths?

Fresh ideas do not stay under the radar for long, and early interest often sets the breakout tone before momentum comes flying in, so act now and get in early.

- Spot companies quietly building strength before the crowd by scanning the list of solid balance sheet and fundamentals (20 results) that filters for resilient businesses investors often overlook.

- Ride potential income and price momentum together by checking the 3 dividend fortresses built around companies offering substantial yields with an eye on staying power.

- Catch emerging themes while they are still dropping hints, not headlines, by working through the curated 10 high quality undiscovered gems list.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com