Bravida Holding (OM:BRAV) Lands Major Data Centre Work, Is The Stock Now Pricey?

Bravida Holding (OM:BRAV) has attracted fresh investor attention after securing a €200 million principal contractor role for atNorth’s data centre in Kouvola, Finland, supported by additional contracts in Swedish public infrastructure and Nordic data centre projects.

See our latest analysis for Bravida Holding.

The latest data centre wins come on the back of strong recent market interest in Bravida Holding, with a 24.6% 3 month share price return and a 48.6% 1 year total shareholder return.

If this surge in Nordic data centre and infrastructure work has caught your attention, it could be a good moment to see what else is emerging across power and grid related opportunities via the 34 power grid technology and infrastructure stocks.

After Bravida Holding’s strong share price run and a series of sizeable data centre and infrastructure contracts, the tension now is simple: pay up for the momentum, or wait for a more comfortable entry as valuation settles?

Most Popular Narrative: 1% Overvalued

Bravida Holding closed at SEK130.40 against a narrative fair value of SEK128.43, so the current price sits slightly above that widely followed estimate.

Bravida's strategic focus on selective project acquisition, prioritizing projects with better margins, is expected to enhance long-term revenue and profitability, potentially leading to improved net margins.

Curious what kind of revenue growth, margin uplift and future earnings power need to line up to support that fair value and price target tension? The full narrative lays out the step by step financial path behind those assumptions, including how projected growth, profitability and valuation multiples all have to work together.

Result: Fair Value of SEK128.43 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, there are still pressure points that could unsettle the Bravida Holding story, including the 26% drop in order intake and ongoing restructuring costs in Sweden and Denmark.

Find out about the key risks to this Bravida Holding narrative.

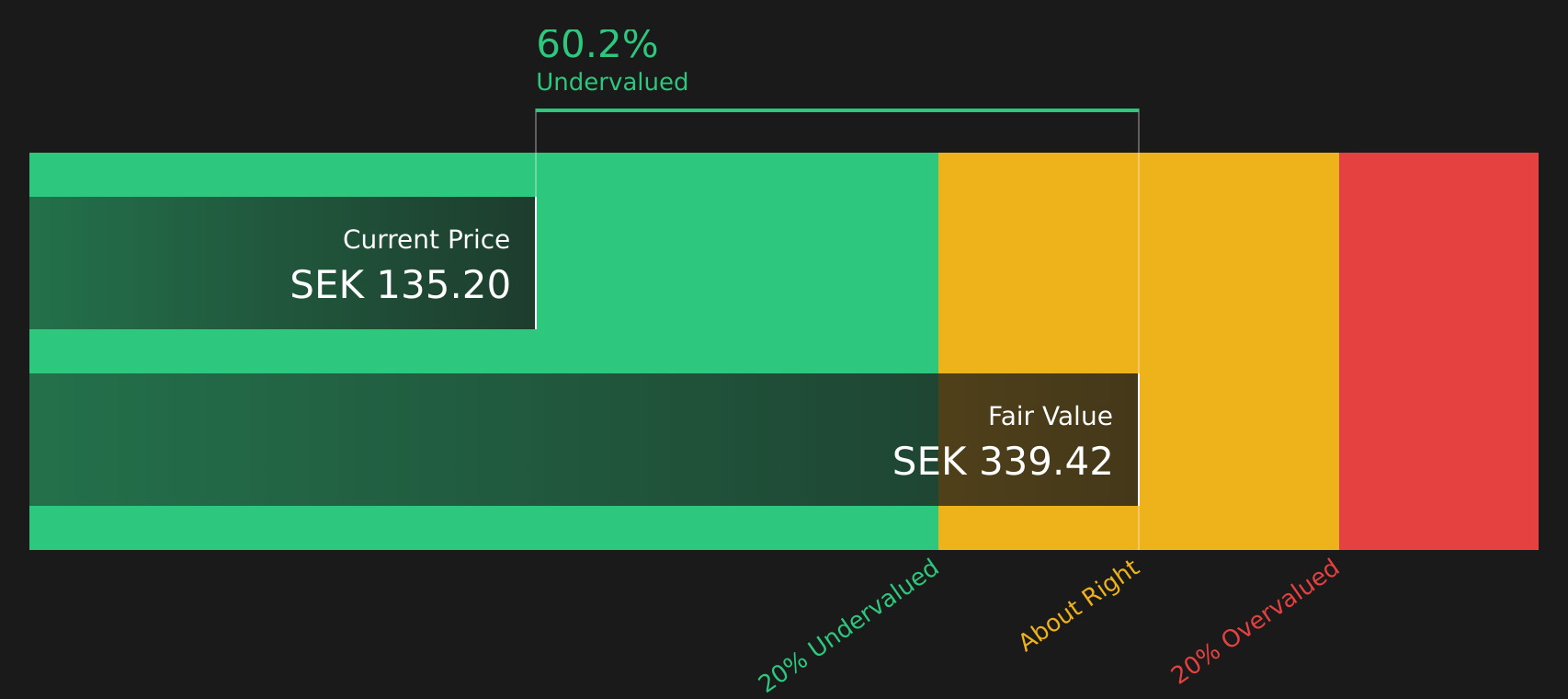

Another View: Bravida Holding Through a Cash Flow Lens

While the analyst narrative frames Bravida Holding as about 1% overvalued against a SEK128.43 fair value, the SWS DCF model comes to a very different conclusion. On that approach, SEK130.40 sits well below an estimated future cash flow value of SEK339.42, which points to a wide gap in what different methods imply.

For investors, the real question is which set of assumptions feels more realistic when you line them up against Bravida Holding’s order trends, margins and long term contract profile.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Bravida Holding for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 215 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this combination of optimism and tension around Bravida Holding has you considering your next steps, take action while the facts are top of mind and review the complete picture yourself with the 4 key rewards.

Looking for more investment ideas beyond Bravida Holding?

Do not stop with Bravida Holding. Broaden your watchlist now with focused stock ideas that could sharpen your next move using the Simply Wall St Screener.

- Target value opportunities by reviewing companies that appear underpriced on quality and fundamentals through the 215 high quality undervalued stocks.

- Prioritise resilience by focusing on companies with stronger balance sheets and financial foundations using the solid balance sheet and fundamentals stocks screener (419 results).

- Hunt for underfollowed opportunities by scanning the screener containing 500 high quality undiscovered gems before others start paying attention.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com