3 Asian Growth Companies With High Insider Ownership Growing Revenues Up To 50%

Amidst the backdrop of geopolitical tensions and energy market volatility affecting global markets, Asian equities have shown resilience, with technology sectors in particular benefiting from regional initiatives toward self-sufficiency. As investors navigate these uncertain times, growth companies with high insider ownership can present compelling opportunities due to their potential alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Asia

| Name | Insider Ownership | Earnings Growth |

| Suzhou Dongshan Precision Manufacturing (SZSE:002384) | 33.5% | 73.1% |

| Meiko Electronics (TSE:6787) | 19.2% | 27.6% |

| L&C BIOLTD (KOSDAQ:A290650) | 24% | 148.5% |

| Jiangxi Fushine Pharmaceutical (SZSE:300497) | 21.1% | 55.9% |

| HUMAN MADE (TSE:456A) | 23.9% | 23.4% |

| Guangzhou Tinci Materials Technology (SZSE:002709) | 38.4% | 28.9% |

| Great Microwave Technology (SHSE:688270) | 29.5% | 85.5% |

| Gold Circuit Electronics (TWSE:2368) | 30.1% | 38.2% |

| Fulin Precision (SZSE:300432) | 10.4% | 60.7% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 14.1% | 40.4% |

We'll examine a selection from our screener results.

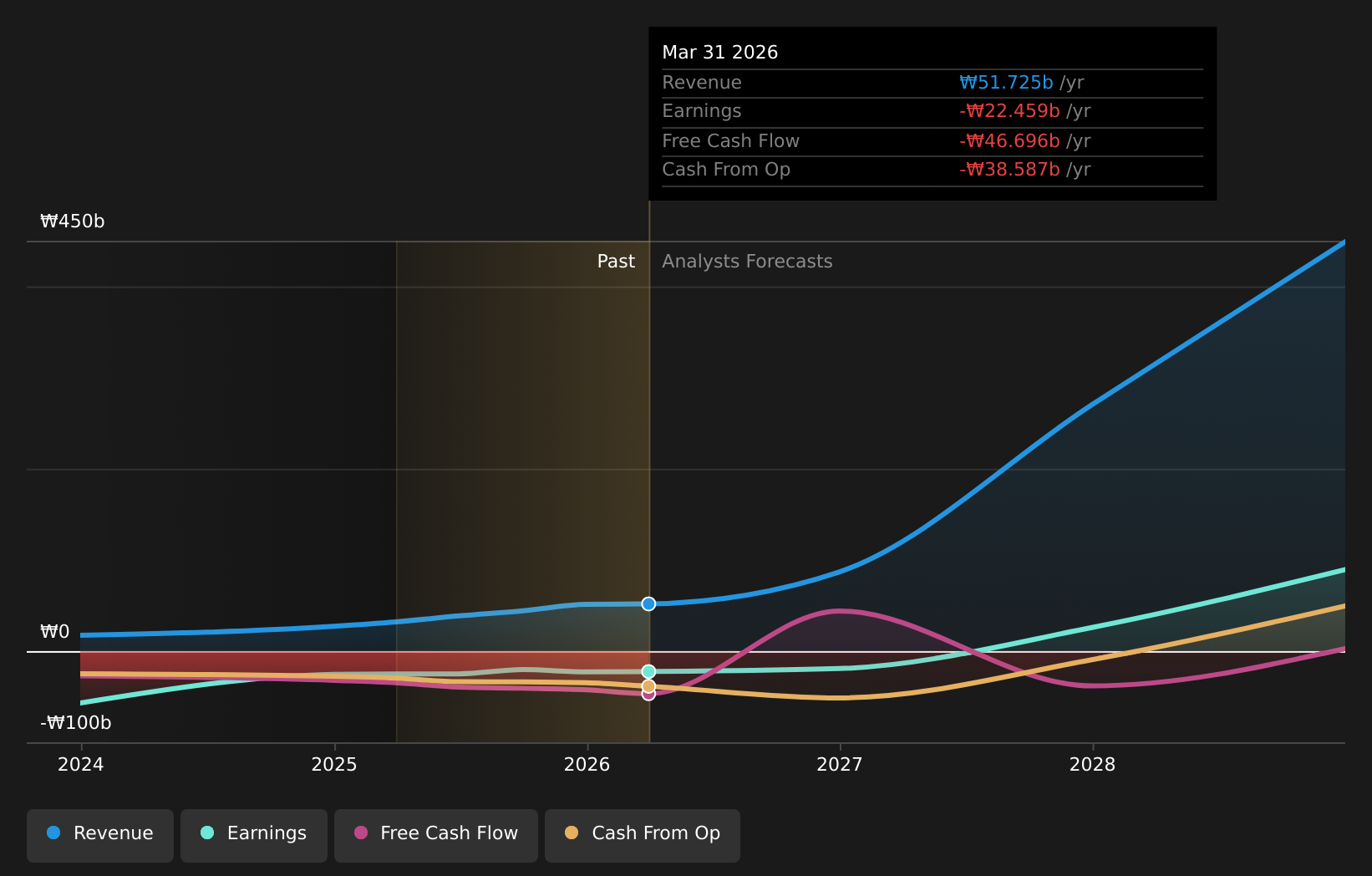

Livsmed (KOSDAQ:A491000)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Livsmed Inc. operates in South Korea, focusing on the research, development, manufacture, export, and import of electro-diagnostic and electro-therapeutic medical devices with a market cap of ₩1.06 trillion.

Operations: The company's revenue primarily comes from its medical device import/export and research and development segment, generating ₩51.72 billion.

Insider Ownership: 39%

Revenue Growth Forecast: 50.9% p.a.

Livsmed, recently added to the S&P Global BMI Index, exhibits significant growth potential with a forecasted revenue increase of 50.9% per year, surpassing the KR market's average. Despite its highly volatile share price, Livsmed's earnings are projected to grow at 74.71% annually and it is expected to become profitable within three years—outpacing average market growth. However, its Return on Equity is anticipated to remain modest at 16.2%.

- Click here and access our complete growth analysis report to understand the dynamics of Livsmed.

- Our expertly prepared valuation report Livsmed implies its share price may be too high.

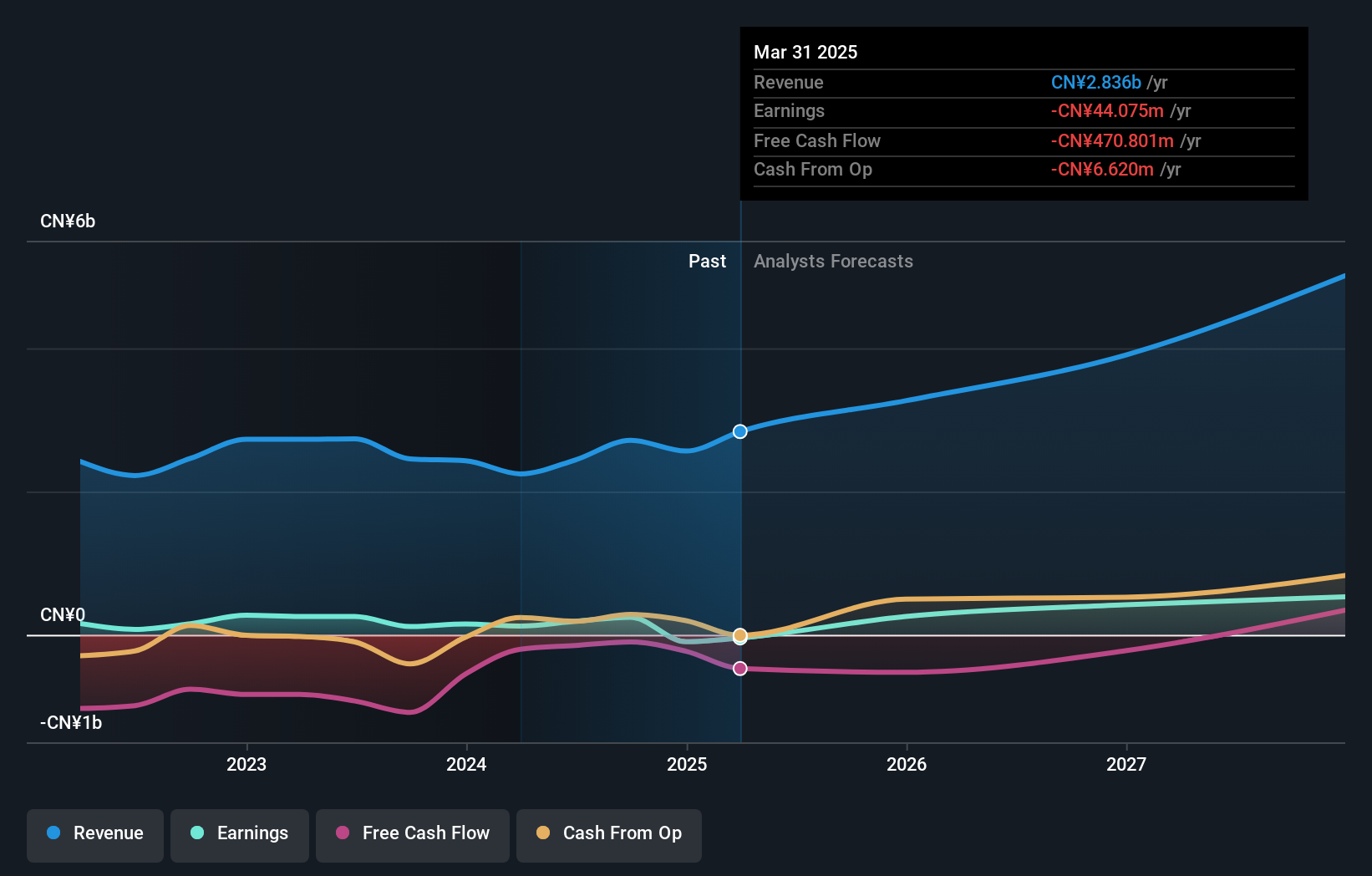

Intsig Information (SHSE:688615)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Intsig Information Co., Ltd. focuses on researching and developing text recognition and commercial big data core technologies in China, with a market cap of CN¥22.47 billion.

Operations: Intsig Information Co., Ltd. generates revenue through its development of text recognition and commercial big data technologies in China.

Insider Ownership: 11.4%

Revenue Growth Forecast: 23.1% p.a.

Intsig Information shows strong growth potential with forecasted revenue growth of 23.1% annually, outpacing the CN market average. While its earnings are expected to grow significantly at 21.9% per year, they trail behind the broader market's anticipated growth rate. The company trades at a favorable value with a price-to-earnings ratio of 45.6x compared to the industry average of 90.2x. Recent quarterly results highlight robust performance, with net income rising to CNY 155.25 million from CNY 116.14 million year-on-year.

- Dive into the specifics of Intsig Information here with our thorough growth forecast report.

- Our valuation report here indicates Intsig Information may be undervalued.

Wuhan Jingce Electronics Group (SZSE:300567)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Wuhan Jingce Electronics Group Co., Ltd. operates in the research, development, production, and sale of semiconductor, display, and new energy testing equipment across China and internationally, with a market capitalization of approximately CN¥83.11 billion.

Operations: The company's revenue primarily comes from its Electron Product segment, which generated approximately CN¥3.40 billion.

Insider Ownership: 32.3%

Revenue Growth Forecast: 23% p.a.

Wuhan Jingce Electronics Group demonstrates strong growth potential with forecasted revenue and earnings growth significantly outpacing the market at 23% and 60.3% annually, respectively. Despite recent volatility in its share price, the company reported improved quarterly results with net income rising to CNY 42.71 million from CNY 37.6 million year-on-year. Recent M&A activity saw a 5.02% stake acquisition by Wuhan Wenfa Yisheng Private Fund Management for approximately CNY 850 million, reflecting strategic insider movements within the firm.

- Navigate through the intricacies of Wuhan Jingce Electronics Group with our comprehensive analyst estimates report here.

- The analysis detailed in our Wuhan Jingce Electronics Group valuation report hints at an inflated share price compared to its estimated value.

Summing It All Up

- Gain an insight into the universe of 472 Fast Growing Asian Companies With High Insider Ownership by clicking here.

- Curious About Other Options? AI is about to change healthcare. These 130 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com