Australian Dividend Stocks With Strong Yields and Staying Power

With inflation trends mixed across regions and central banks weighing their next moves, many investors are looking for income streams that feel steadier than headline news. The Dividend Powerhouses (3%+ Yield) screener focuses on companies offering dividend yields above 5% that are described as well covered, growing and stable. That combination can appeal if you want your portfolio to lean on cash returns while bond markets and policy expectations keep shifting. In this article, you will see 3 stocks from the screener that stand out for further research as potential anchors in a dividend-focused strategy.

CSL (ASX:CSL)

Overview: CSL is a global biopharmaceutical company that turns human plasma, vaccines and specialty therapies into treatments for serious conditions such as immune deficiencies, bleeding disorders, iron deficiency and kidney disease, while also supplying influenza vaccines to governments worldwide.

Operations: CSL generates about US$10.9b from CSL Behring, US$2.4b from CSL Vifor and US$2.2b from CSL Seqirus, with revenue spread primarily across the United States (US$7.3b) and a broad Rest of World base (US$4.6b).

Market Cap: A$58.9b

CSL attracts attention in an income screen because it combines a 3.42% dividend yield with a large, diversified healthcare business built around an extensive plasma collection network, flu vaccines and therapies for kidney and iron disorders. Recent restructuring, weaker margins and a one off US$2.1b loss have weighed on sentiment, while debt levels and reliance on external funding add financial risk. At the same time, analysts currently forecast earnings growth, the plasma and gene therapy franchises remain central in rare disease treatment, and some investors see a gap between the current share price and their estimates of long term cash flow value. For dividend focused investors, the question is whether temporary pressure is masking a stronger core business story.

CSL’s pressure on margins and sentiment may be masking a stronger income engine. Before you decide the dividend story is fully priced in, review the 2 key rewards and 4 important warning signs

QBE Insurance Group (ASX:QBE)

Overview: QBE Insurance Group is a global insurer that underwrites general insurance and reinsurance across commercial, personal, and specialty lines, covering everything from property, motor and agriculture to marine, energy, aviation and professional indemnity, while also managing Lloyd’s syndicates and providing investment management services.

Operations: QBE generates around US$11.2b from its International division, US$8.2b from North America, US$5.7b from Australia Pacific and US$77m from Corporate and Other activities.

Market Cap: A$38.0b

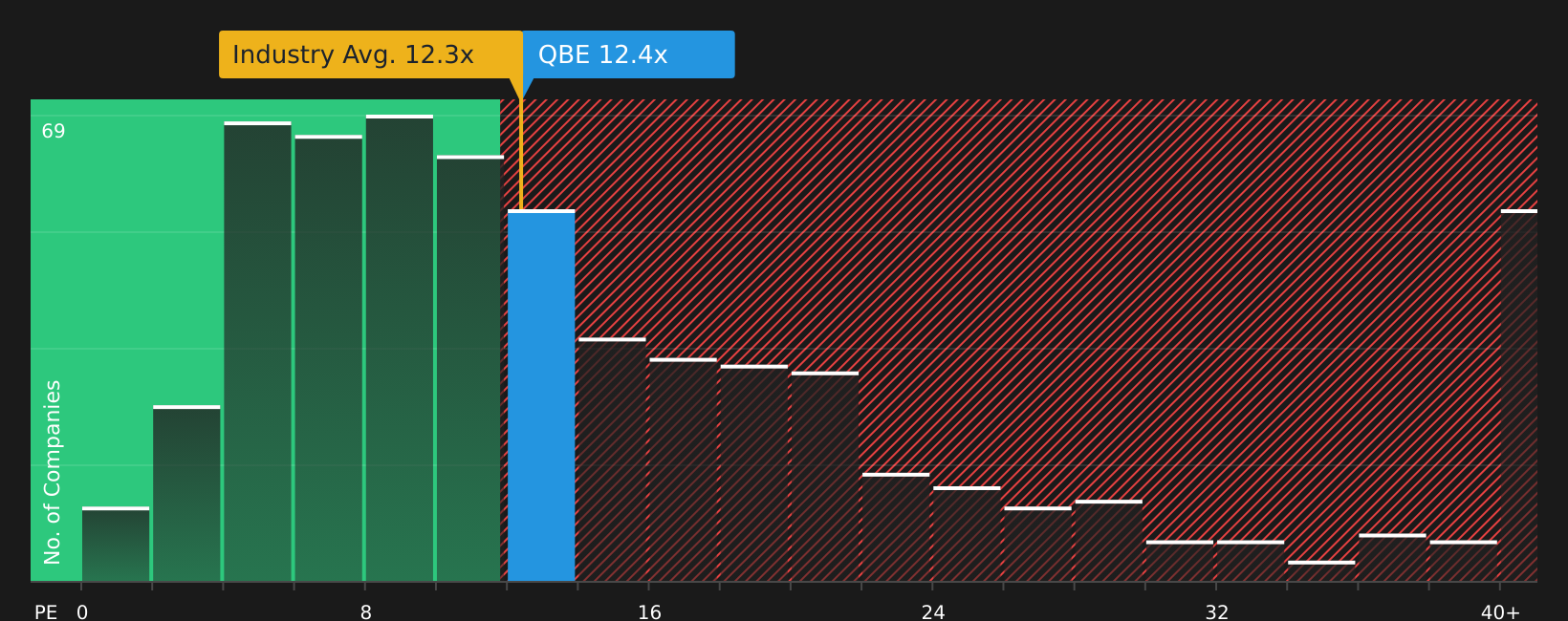

QBE Insurance Group appears in an income screen because it combines a global spread of premiums with an 18.5% Return on Equity, an 11.4% net margin and earnings growth of 23.3% over the past year, while trading on a P/E of 12.4x that is below the local insurance peer average. At the same time, softening premium rate increases, underwriting volatility from large losses and an unstable dividend history keep risk firmly on the table, especially with 100% of liabilities tied to external funding rather than customer deposits. For dividend focused investors, the question is whether QBE’s diversification, digital investments and recent expansion in markets such as India offset those pressure points and support a more dependable income profile over time.

QBE Insurance Group’s 18.5% Return on Equity and global spread of premiums suggest a stronger earnings engine than the P/E of 12.4x implies, but the real story sits inside the 2 key rewards and 1 important warning sign

Evolution Mining (ASX:EVN)

Overview: Evolution Mining is a gold producer that explores for, develops and operates gold and gold copper mines in Australia and Canada, also producing copper and silver concentrates that are sold into global markets.

Operations: Evolution Mining generates A$1.7b from Cowal, A$1.1b from Ernest Henry, A$780m from Mungari, A$674m from Red Lake, A$581m from Northparkes, A$153m from Mt Rawdon and A$156m from corporate and other activities.

Market Cap: A$23.6b

Evolution Mining is attracting attention in a dividend focused screen because it couples high quality gold assets and copper exposure with strong recent fundamentals, including 92.3% earnings growth over the past year, a 23.6% Return on Equity and margins that widened from 17.7% to 26%. The Nevada North Lithium joint venture adds a different commodity angle. However, it also introduces execution and project risk, alongside rising regulatory, labor and ESG compliance costs that could pressure future margins, especially as ore grades at key assets mature. For income and quality focused investors, the key consideration is whether this mix of high margin gold production, copper and lithium growth options, premium pricing and an unstable dividend track record aligns with their expectations for more resilient long term cash generation.

Evolution Mining’s mix of high margin gold, copper and lithium options suggests an earnings story many investors may be underestimating. It is worth checking the analyst forecasts for Evolution Mining before one key piece of the risk reward puzzle shifts.

The three stocks covered here are just a starting point, and the full Dividend Powerhouses (3%+ Yield) screen has surfaced 27 more companies with equally compelling income stories buried inside the Dividend Powerhouses (3%+ Yield) screener. Use Simply Wall St to identify, filter and analyze the specific catalysts and dividend narratives that matter to you so you can focus on your highest conviction ideas.

Take Control of Your Investment Journey

If Evolution Mining or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Curious About What You Might Be Missing?

Fresh stock ideas can move from under the radar to full breakout fast, and the best entry points rarely wait around before the crowd catches on, so consider acting early.

- Spot overlooked strength by scanning a curated list of solid balance sheet and fundamentals (20 results) that can help you focus on companies built to handle tougher conditions without constant surprises.

- Explore potential momentum in metals by checking a hand picked 33 elite gold producer stocks that highlights producers tied to one of the market’s most watched commodities.

- Review a focused 34 power grid technology and infrastructure stocks that zeroes in on businesses positioned around critical energy upgrades.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com