Charles River Laboratories International (CRL) Expands AI Pathology Platform, Is The Valuation Upside Already Priced In?

AI Pathology Expansion and Fresh Highs Focus Attention on Charles River Laboratories International

Charles River Laboratories International (CRL) recently expanded its AI-enabled digital pathology platform. This initiative coincided with the stock reaching a 52-week high at US$236.67 and attracting increased investor attention.

See our latest analysis for Charles River Laboratories International.

Alongside the AI pathology expansion, Charles River Laboratories International has seen strong momentum, with a 30-day share price return of 24.48% and a 1-year total shareholder return of 46.43%, even though the 5-year total shareholder return is down 39.29%.

If this kind of AI driven story has your attention, it could be worth scanning a wider set of healthcare technology opportunities through our curated list of 41 healthcare AI stocks

Charles River Laboratories International now combines an AI-focused story with a fresh 52-week high, which raises a different issue for you as an investor: is this strong platform business already priced for that promise or not?

Most Popular Narrative: 25.6% Undervalued

According to the most followed narrative on Charles River Laboratories International, the fair value of $313.61 sits well above the recent $233.41 close, which frames the current AI story against a much higher long term valuation anchor.

The Hidden Bottleneck in Drug Development: Why Charles River Acquired a Cambodian Primate Supplier

On January 12, 2026, Charles River Laboratories announced that it had signed an agreement to acquire the assets of K.F. (Cambodia) Ltd., a major non-human primate (NHP) breeding and supply company. [$510M] At first glance, this transaction might appear to be a routine supply chain acquisition in the contract research organization (CRO) industry. However, the deeper implication is far more significant.

Want to see what underpins that higher fair value for Charles River Laboratories International? The narrative leans on confident assumptions about future margins, profit growth and the earnings multiple applied to those profits. The full story connects these moving parts into one cohesive pricing view.

Result: Fair Value of $313.61 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that Charles River Laboratories International narrative could be challenged if the primate acquisition faces regulatory pushback, or if AI pathology adoption falls short of expectations.

Find out about the key risks to this Charles River Laboratories International narrative.

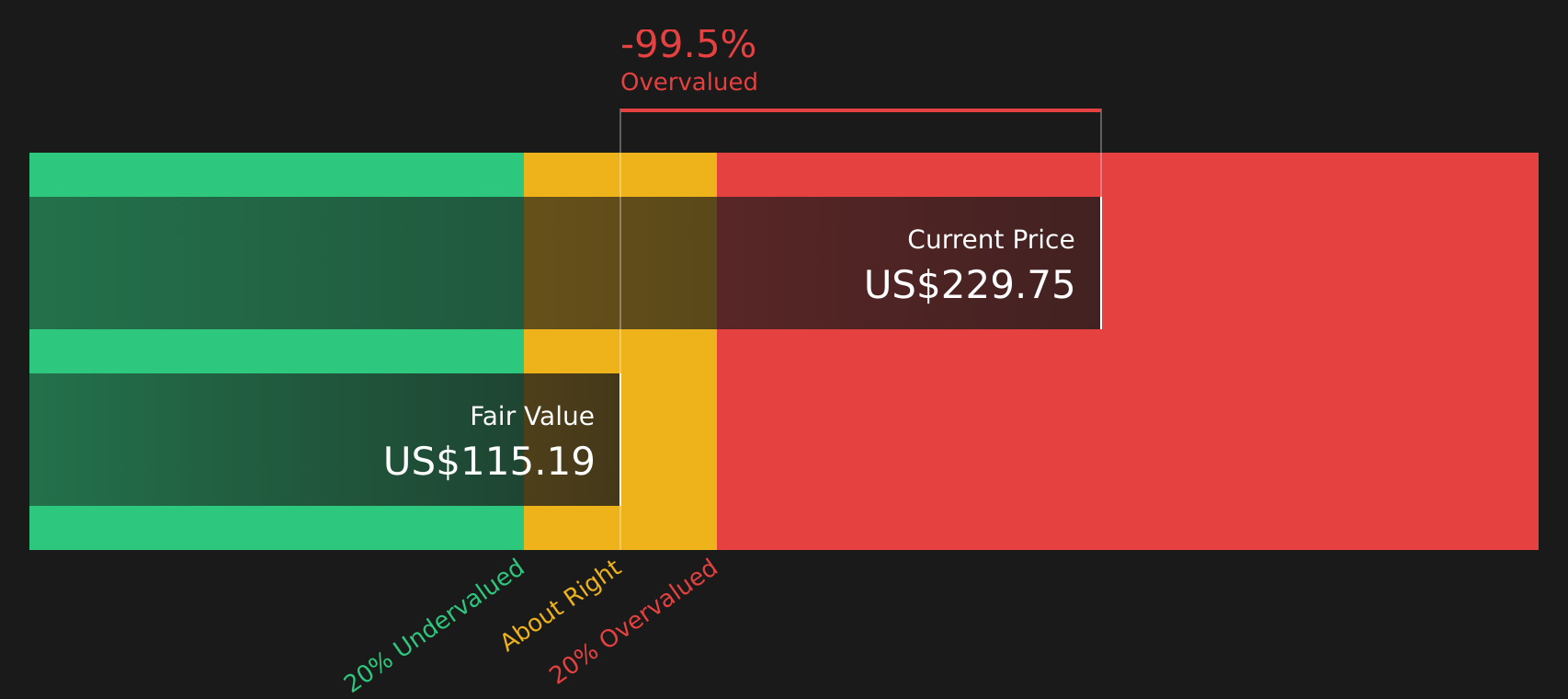

Another View: Our DCF Model Sees Charles River Laboratories International As Overvalued

The user narrative frames Charles River Laboratories International as 25.6% undervalued, with a fair value of $313.61 against the recent $233.41 share price. Our DCF model tells a very different story, with an estimate of future cash flow value of $115.19, which would imply the stock is overvalued instead.

This gap between a narrative driven fair value and the SWS DCF model raises a practical question for you as an investor: which set of assumptions about future cash generation feels more realistic when you look at Charles River Laboratories International's actual track record and current fundamentals?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Charles River Laboratories International for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 45 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly split on Charles River Laboratories International, it makes sense to move quickly, review the full picture, and weigh both sides for yourself using the 2 key rewards and 2 important warning signs

Looking for more investment ideas beyond Charles River Laboratories International?

If you are weighing what to do after the Charles River Laboratories International news, do not stop here. Fresh ideas elsewhere could be just as important for your portfolio.

- Target potential mispricings by scanning 45 high quality undervalued stocks that combine strong fundamentals with room for the market to reassess their prospects.

- Strengthen your income stream by reviewing 9 dividend fortresses built around higher yielding companies with the potential to support regular payouts.

- Dial down volatility risk by focusing on 78 resilient stocks with low risk scores that aim for more resilient balance sheets and steadier business profiles.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com