National Australia Bank (ASX:NAB) Puts Capital And Dividends In Focus On An Undervalued View

National Australia Bank (ASX:NAB) has caught investor attention after reinforcing its capital position through an additional ordinary share issue and paying a fully franked interim dividend of A$0.850 per share, with a 4.32% annual yield.

See our latest analysis for National Australia Bank.

At a share price of A$39.61, National Australia Bank has seen firm short term momentum, with a 1 month share price return of 11.01%, while the 3 month share price return is down 12.68% and the 1 year total shareholder return is 4.22%. This is alongside a 3 year total shareholder return of 69.31% and a 5 year total shareholder return of 94.43%.

If you are weighing bank stocks against other income and growth ideas, it can help to compare them with sectors benefiting from structural trends and resilient cash flows.

To widen your watchlist beyond the big banks, take a look at our screener of 5 top founder-led companies

After that sharp 1 month move and the latest dividend, the question for National Australia Bank is whether the current A$39.61 level already prices in the good news, or if it still stacks up on valuation grounds.

Most Popular Narrative: 4.6% Undervalued

Against the last close at A$39.61, the most followed narrative for National Australia Bank points to a fair value of A$41.53 using a 7.78% discount rate and detailed earnings assumptions.

Ongoing digital transformation, focus on cost management, and productivity initiatives (including Citi integration, streamlined processes, and leveraging AI tools) are expected to structurally reduce the cost-to-income ratio over time, potentially boosting net margins and profitability.

Want to see what sits behind that margin story? The narrative leans heavily on measured revenue growth, steady earnings expansion and a richer future earnings multiple. The exact mix of those ingredients is what really drives the A$41.53 fair value call.

Result: Fair Value of A$41.53 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the National Australia Bank narrative could be tested if fintech competition eats into revenue streams or if higher compliance and technology costs continue to put pressure on margins.

Find out about the key risks to this National Australia Bank narrative.

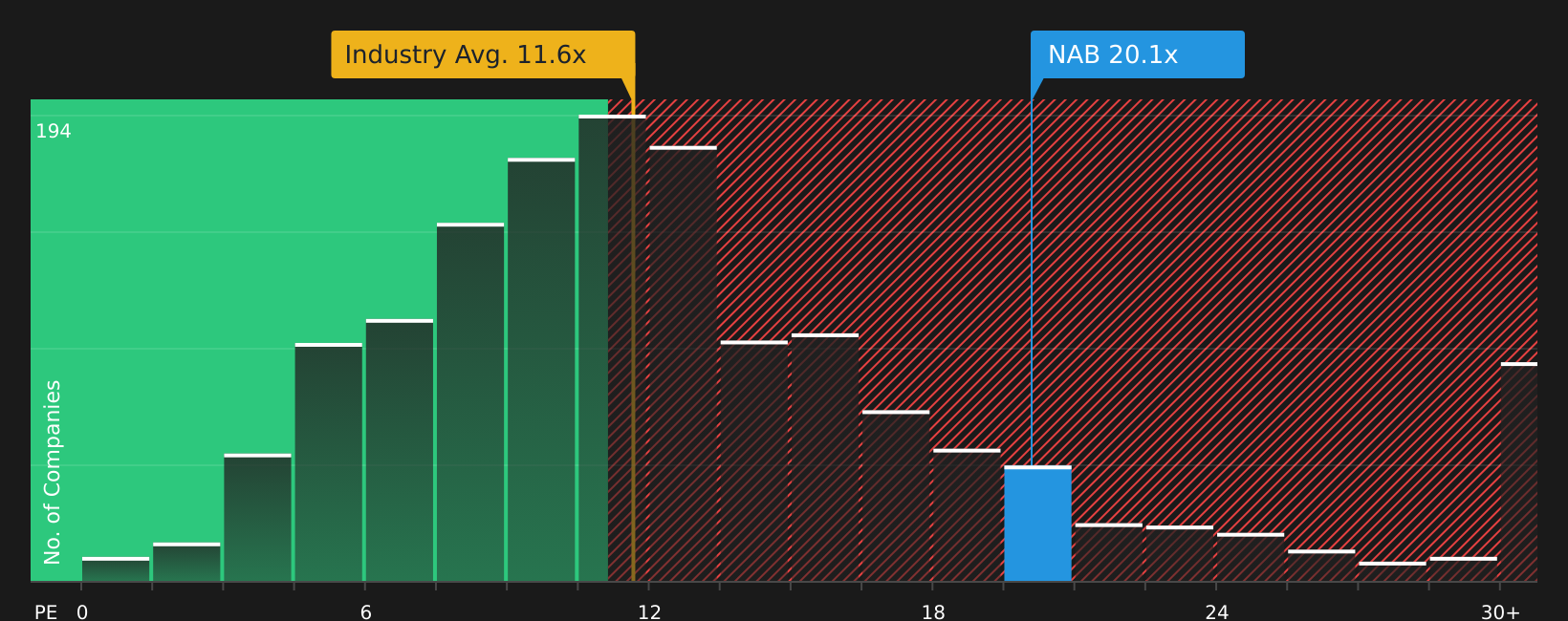

Another View: National Australia Bank Through The P/E Lens

Set against that A$41.53 fair value narrative, National Australia Bank trades on a P/E of 19.8x compared with 18.3x for peers and 11.6x for the wider global banks group, slightly above even its own 19.7x fair ratio. This points to limited margin for error if sentiment cools.

For a closer look at how this P/E gap could close over time and what that might mean for valuation risk, See what the numbers say about this price — find out in our valuation breakdown.

Next Steps

Given the mix of optimism and questions around National Australia Bank, it makes sense to move quickly, review the data yourself and weigh up the 1 key reward and 2 important warning signs highlighted in the 1 key reward and 2 important warning signs

Looking for more investment ideas beyond National Australia Bank?

If National Australia Bank is already on your radar, now could be a time to broaden your watchlist and explore other potential opportunities.

- Consider dependable income streams by reviewing companies in the 6 dividend fortresses that may align with your yield and stability preferences.

- Explore potential value opportunities by scanning the screener containing 12 high quality undiscovered gems before they attract wider market attention.

- Emphasise resilience and capital preservation by focusing on companies highlighted in the 8 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com