Arista Stock And 2 More Quality Picks Backed By Strong Balance Sheets

With inflation signals mixed, government bond yields adjusting to softer data, and central banks weighing their next moves, many investors are looking for stocks backed by solid fundamentals rather than short term sentiment. That is where a Solid Balance Sheet and Fundamentals approach can help, focusing on companies with high return on equity, a record of past performance and sound balance sheets. This article takes that screener and highlights three stocks identified through it, providing a clear, practical starting point for researching resilient opportunities in a market influenced by rates, growth headlines and energy prices.

Powell Industries (POWL)

Overview: Powell Industries is a Houston based manufacturer of custom engineered electrical equipment that powers and protects large scale infrastructure such as data centers, energy projects, utilities, rail systems, and industrial facilities across the globe. Alongside its switchgear, control gear, and power control rooms, the company also provides inspection, installation, commissioning, and repair services for customers in multiple regions and sectors.

Operations: Powell Industries generates about US$1.13b in revenue from electrical equipment, with the United States contributing US$881.77m and additional sales from Canada, Europe, Asia/Pacific, the Middle East and Africa, and Latin America.

Market Cap: US$8.46b

Investors looking at Powell Industries are getting a company tied directly to long term themes like grid upgrades, data center build outs, and electrification, backed by reported profitability metrics such as a 26.4% ROE and net margins around the mid teens. At the same time, current expectations already reflect revenue and earnings growth, while the P/E is above one estimate of fair value and analyst models note some risk of margin normalization if recent project benefits fade. In addition, rising competition, funding that leans on external borrowing, and recent insider selling present a mix of strong fundamentals and secular demand alongside valuation and execution considerations that may warrant closer due diligence.

Powell Industries looks like a pure play on grid upgrades and data center build outs, but the real story may sit in how current expectations stack up against fundamentals in the DCF valuation analysis for Powell Industries

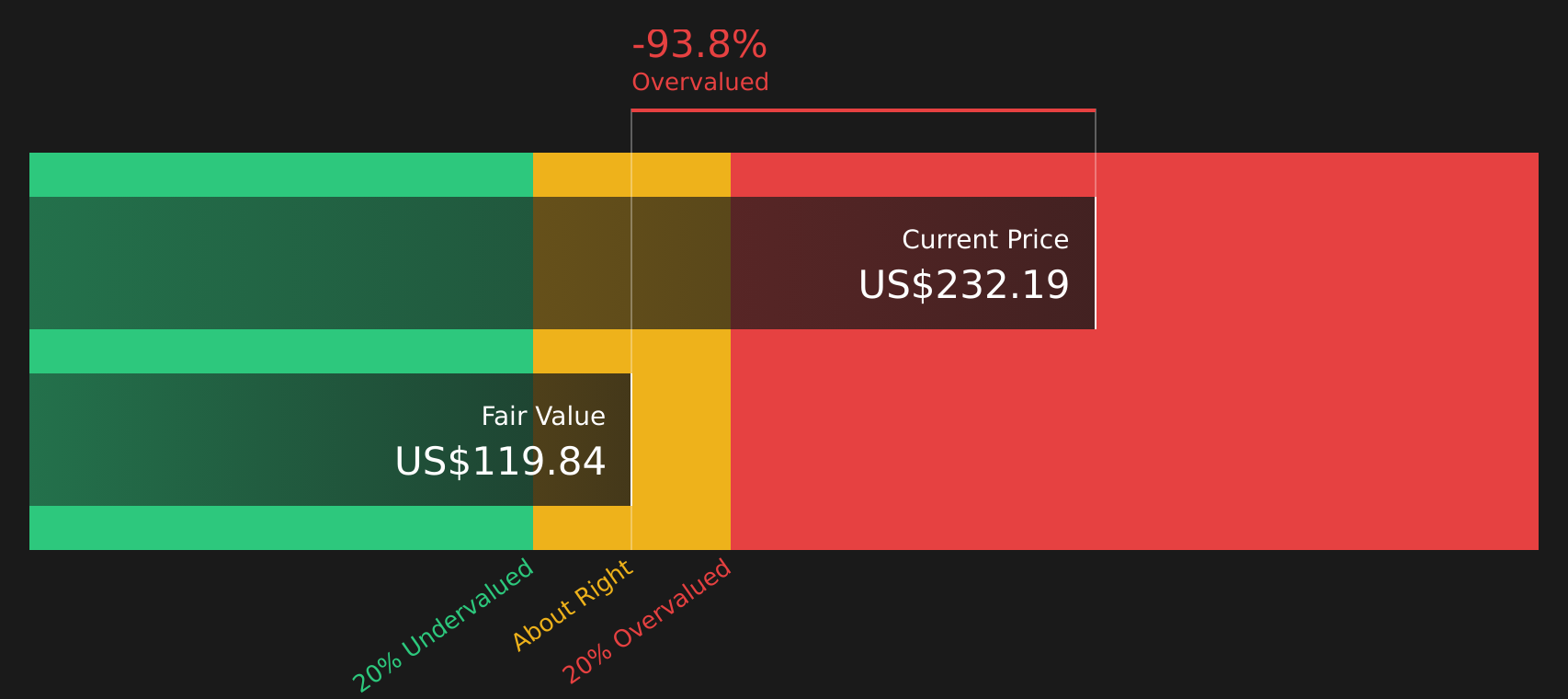

Arista Networks (ANET)

Overview: Arista Networks builds the high speed networking gear and software that link together modern data centers, AI clusters, and large corporate campuses, using its EOS operating system and cloud software to manage traffic efficiently from client devices through to the cloud. Its products and services are used by large internet platforms, financial institutions, governments, and enterprises across sectors that need reliable, scalable connectivity.

Operations: Arista Networks generates US$9.71b in revenue almost entirely from computer networking products and services, with the United States accounting for US$7.75b and additional contributions from Europe, the Middle East and Africa, Asia Pacific, and the rest of the Americas.

Market Cap: US$235.42b

Arista Networks sits at the heart of AI infrastructure build outs, supplying high bandwidth switches and software that underpin GPU clusters and cloud data centers. Recent news shows management lifting revenue guidance and expanding its AI product lineup. High profitability, with a 27.6% ROE and net margins of 38.3%, and expectations for continued high ROE help explain why analysts model solid earnings growth, even as they factor in some margin compression. The flip side is a rich valuation and heavy reliance on a small group of hyperscale customers, plus sizeable backlogs and deferred revenue that could affect how growth shows up in reported numbers. For investors who care about balance sheet strength and fundamentals, the real question is how these strengths and risks line up against the current price.

Arista Networks sits at the crossroads of AI infrastructure and premium valuation, with high margins and concentrated customers raising tough questions. See how the analysis report for Arista Networks weighs the upside against the one factor that could suddenly shift the story.

Costco Wholesale (COST)

Overview: Costco Wholesale operates membership-only warehouse clubs across North America, Europe, and Asia, selling a wide range of discounted groceries, household goods, electronics, apparel, and services, supported by its own Kirkland Signature private label and a growing e-commerce and travel offering.

Operations: Costco Wholesale generates about US$293.59b in revenue primarily from its membership warehouses, with around US$212.16b from the United States, US$39.68b from Canada, and US$41.75b from other international markets.

Market Cap: US$406.34b

Costco Wholesale combines a resilient membership model, with renewal rates above 92% in core markets, and steady earnings growth of around 12% last year, with a sizeable cash pile near US$20b supporting warehouse expansion, dividends, and potential specials. At the same time, a high P/E multiple, reliance on external borrowing for liabilities, tariff risks on key product categories, and rising competition from Sam’s Club mean the stock is not priced like a bargain. For investors focused on solid balance sheets and fundamentals, the real interest is how this mix of quality, growth from digital and international warehouses, and premium pricing compares with the risk of the company being priced for perfection.

Costco’s membership machine, cash reserves near US$20b, and growth from digital and international warehouses could be masking a key valuation twist. See how the analyst forecasts for Costco Wholesale frames the real trade off hiding in plain sight.

The three stocks in this article are only a starting point, with the full Solid Balance Sheet and Fundamentals screener surfacing 44 more companies that share strong return on equity, past performance, and sound balance sheet profiles in the Solid Balance Sheet and Fundamentals screener. Use Simply Wall St to identify and analyze the specific catalysts and narratives that matter most to you so you can focus on the highest conviction opportunities within this group.

Take Control of Your Investment Journey

If Arista Networks or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh ideas move first, and by the time the crowd catches on, the cleanest entry points can be gone. Scan these curated stock groups while it matters and consider acting while the opportunity is still developing.

- Target companies aiming for durable income streams with the 9 dividend fortresses and see which businesses currently pair robust payouts with balance sheets built to handle stress.

- Spot potential early leaders in AI infrastructure by reviewing the 52 AI infrastructure stocks and focus on businesses supplying the picks and shovels behind data center demand.

- Pursue growth stories tied to future power demand with the 89 nuclear energy infrastructure stocks and concentrate on companies supporting long term nuclear energy expansion.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com