Dollarama Stock And 2 Retail Picks Facing Tariff And Inventory Pressure

Tariff headlines and shifting import rules can feel abstract until they hit store shelves and freight costs. With the Section 122 surcharge set to expire in 2026, tariff refunds in play, and shippers pulling orders forward, retail sector stocks are sitting in the crosshairs of policy and demand. For investors, this mix of legal uncertainty and firm consumer resilience can create both opportunity and risk. This article walks through 3 stocks from our Retail Sector Stocks screener that are directly exposed to these trade and inventory currents, to help you decide which may deserve a closer look or a wider berth.

Dollarama (TSX:DOL)

Overview: Dollarama is a discount retailer that runs a large network of low-price variety stores, selling everyday consumables, general merchandise, and seasonal products across Canada and several international markets, with an online store complementing its physical presence.

Operations: Dollarama generates about CA$7.6b in revenue from its Retail - Variety Stores segment.

Market Cap: CA$50.1b

Investors watching tariff headlines should pay attention to Dollarama because it sits at the intersection of resilient consumer demand and complex import costs. The company is benefiting from steady appetite for value, solid recent earnings and ongoing international expansion into Latin America and Australia, while using buybacks and dividends to return capital. At the same time, high leverage, an elevated P/E multiple versus peers, and exposure to trade rules and counter tariffs on U.S. imports mean results are sensitive to logistics, sourcing and consumer confidence. If you want to understand how this mix of discount demand, international growth and tariff risk could affect Dollarama over the next few years, you are only seeing part of the picture here.

Dollarama’s expanding reach, solid recent earnings and tariff exposure make for an unusual mix of strength and vulnerability, and the full story only really comes into focus in the 2 key rewards and 2 important warning signs

Myer Holdings (ASX:MYR)

Overview: Myer Holdings is a long established Australian department store group that sells a wide range of fashion, beauty, homewares, toys and gifts for women, men and kids through its national store network and online channel.

Operations: Myer Holdings generates about A$2.7b in revenue from its Myer Retail segment, with a further A$771.9m reported as segment adjustments.

Market Cap: A$510.6m

Myer Holdings is closely tied to consumer spending and inventory cycles, so signs of resilient shoppers, early restocking and heavier import flows are especially relevant. The stock trades on a very low P/S ratio versus peers and carries a double digit dividend yield, which some investors may see as appealing. However, that payout is not well covered by current earnings and the company is presently loss making. Forecasts indicate revenue growth and a move back into profit, yet funding is entirely dependent on external borrowing and both the board and management are relatively new. The balance between recovery potential, tariff tailwinds and financial risk is where both the opportunity and the caution lie for Myer.

Myer Holdings appears to be a recovery story hiding inside a low P/S tag and a double digit yield, yet the real tension sits in its funding, payout and tariff exposure. Get the fuller picture in the analysis report for Myer Holdings

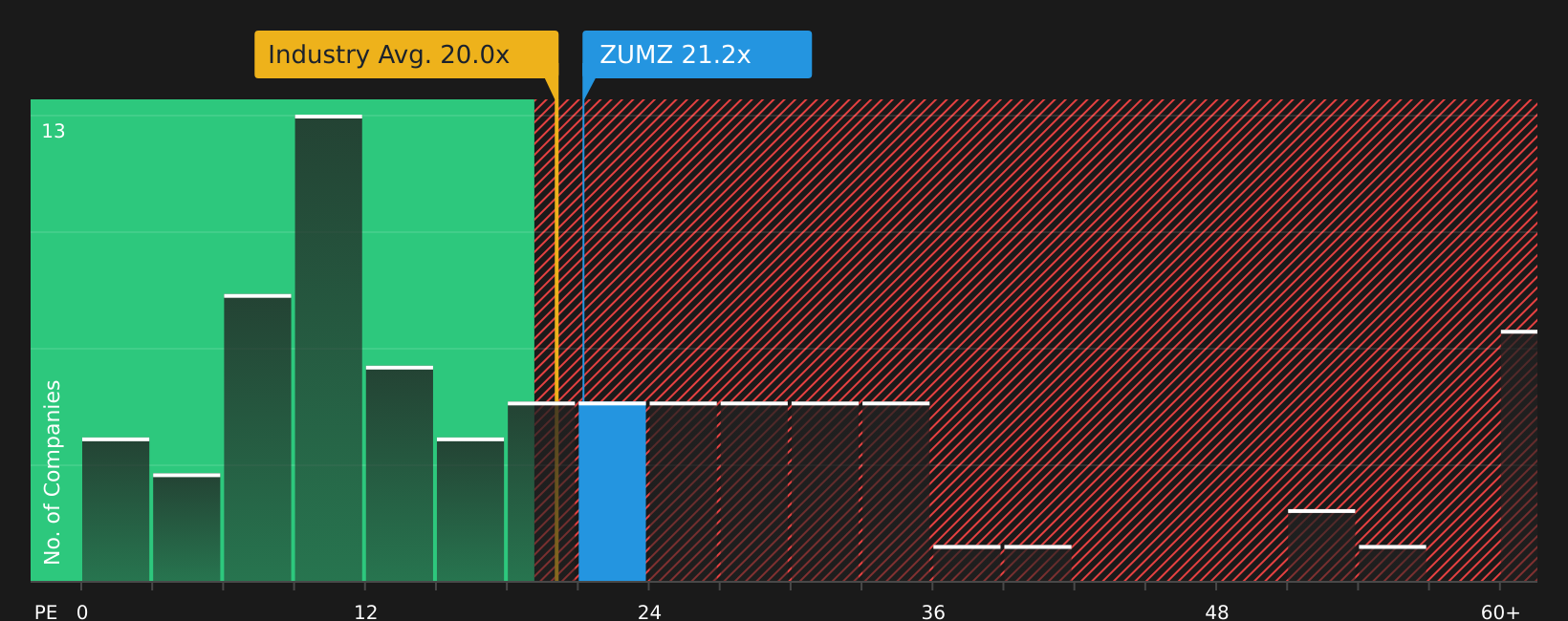

Zumiez (ZUMZ)

Overview: Zumiez is a specialty retailer focused on youth oriented apparel, footwear, accessories and skate and snow hardgoods, selling through its Zumiez, Blue Tomato and Fast Times stores and e commerce sites across the United States, Canada, Europe, Australia and other markets.

Operations: Zumiez generates about US$938.1m in revenue from its Retail - Apparel segment, with roughly US$713.1m from the United States and the rest split across Canada, Europe and Australia.

Market Cap: US$305.6m

Zumiez sits right where tariff headlines, youth fashion trends and inventory decisions meet. This is why tariff related stockpiling and signs of resilient discretionary spending matter so much for this retailer. Management has been pulling some imports forward, working to spread sourcing across more countries and leaning harder into private label, digital engagement and experiential stores. These efforts aim to support margins even as earnings remain volatile and recent quarters included losses. At the same time, a richer P/E, recent insider selling, weak European results and a CFO transition mean the stock is hardly a one way bet. To see how this balance of potential upside from margin improvement and digital growth stacks up against tariff, execution and valuation risks, you will need more than the snapshot here.

Zumiez looks like a stock where tariff risk, youth fashion and digital engagement are colliding, while the real twist sits in how its margins, sourcing shifts and valuation line up in the analysis report for Zumiez

The three retail sector stocks covered here are just a starting point. The full Retail Sector Stocks screener uncovers 37 more companies with equally compelling narratives and different mixes of tariff exposure, balance sheet strength and consumer demand sensitivity in the Retail Sector Stocks screener. Use Simply Wall St to identify and analyze the specific catalysts that matter to you, from import costs and inventory moves to dividends and valuation, so you can focus on the highest conviction opportunities that fit your own view of the retail sector.

Take Control of Your Investment Journey

If Zumiez or any of these companies sound like a great opportunity, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value the ideal entry point. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Beyond Retail?

New stock ideas do not stay under the radar for long. Before the next breakout gathers momentum and prices start flying, scan these fresh sets of opportunities while it matters and consider your options early.

- Target reliable cash flows and balance sheet strength by reviewing a curated list of solid balance sheet and fundamentals (12 results) that may help you avoid weaker stocks before sentiment drops.

- Catch structural trends early by scanning 52 AI infrastructure stocks before these behind the scenes enablers of AI demand get fully caught by the broader market.

- Explore long term metal demand by checking 8 top copper producer stocks while these producers are still largely under the radar, rather than waiting until after prices move significantly.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com