Is Now the Ultimate Entry Point for Micron Technology Stock?

Key Points

The memory chip shortage will likely last into 2028.

The market expects huge growth from Micron over the next year.

Micron (NASDAQ: MU) has been an incredible stock to own so far in 2026. It's up around 250% this year, but it's also down around 20% from its all-time highs set just a few weeks ago. That begs the question, is now a sign of a future, bigger drop? Or is it the perfect buying opportunity for those who missed out?

Let's take a look at what Micron's stock has to offer investors after its initial major run-up and see if it's a worthwhile buy.

Missed Nvidia in 2009? This Rare Signal Is Flashing Again. In 2009, a "Double Down" signal flashed for a little-known chipmaker called Nvidia. For the first time in years, that same "Total Conviction" signal is flashing for a company 1/100th the size of Nvidia. Continue »

Image source: Getty Images.

The memory chip market will struggle to maintain balance for a while

Micron fabricates memory chips, which are utilized in nearly every computing device on the market. Micron makes the two primary types of memory chips: NAND (non-volatile memory that's often used for long-term data storage) and DRAM (volatile, high-speed memory that's used in conjunction with computing units).

Both NAND and DRAM memory are utilized in all sectors of a data center. However, the massive demand wave the data center build-out is creating is too large for the memory fabrication supply chain to handle. As a result, prices are skyrocketing to adjust for booming demand and limited supply.

Micron and its peers are scrambling to bring new production capacity online. Still, they're also being cautious not to overbuild because this demand wave is temporary (even if it lasts for a few years beyond 2026). Micron's management team believes it will have increased capacity online in mid-2027, but that market conditions won't improve until 2028 or later.

That means there is still plenty of upside ahead for Micron and its investors, but after a 250% rise, is the stock too expensive?

Absolutely not.

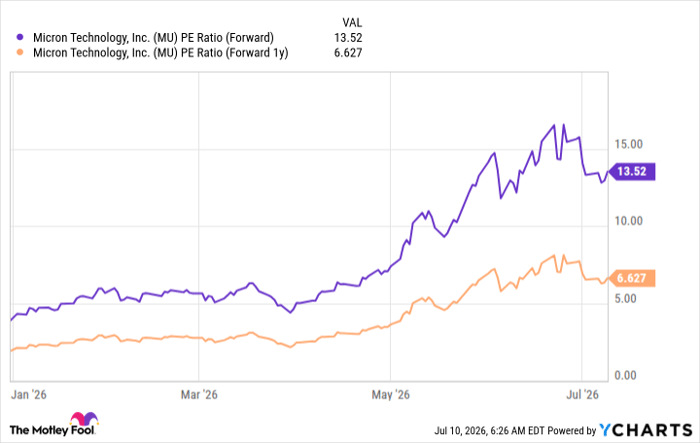

Because Micron operates in the cyclical memory chip business, there will always be some amount of speculation regarding the length of the demand wave. So, investors are slowly pricing in growth. Right now, the stock trades for just 13.5 times forward earnings, but also at just 6.6 times next year's earnings.

MU PE Ratio (Forward) data by YCharts

So, if the 13.5 times forward earnings is the maximum price tag that the market is willing to pay for Micron's business, and Wall Street's earnings projections for next year pan out, it's likely that the stock could double from now until this time next year. While the actual movement of the stock won't be that cut and dried, that's the reality investors are looking at.

With the memory chip market likely to experience tightness for a while and Micron expected to grow massively over that same time frame, I think investors can confidently buy the stock on the dip and achieve incredible returns.

Keithen Drury has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Micron Technology. The Motley Fool has a disclosure policy.