Is FirstService’s New Resilience Program Quietly Redefining Its Services Model (TSX:FSV)?

- Earlier this month, FirstService Residential launched Resilience First, a risk management program offering complimentary pre-loss inspections and coordinated support for water, fire and storm-related incidents at community associations and high-rise properties, in collaboration with First Onsite Property Restoration, Roofing Corp. of America and FirstService Insurance Brokers.

- This initiative highlights how FirstService is trying to deepen its role in property risk planning and recovery, potentially strengthening client relationships through integrated restoration, roofing and insurance support.

- We’ll now examine how this coordinated risk management offering could influence FirstService’s broader investment narrative around recurring services and operational efficiency.

Uncover the next big thing with 11 elite penny stocks that balance risk and reward.

FirstService Investment Narrative Recap

To own FirstService, you need to believe in its ability to grow recurring property services while improving efficiency across Residential, Restoration and Brands. The new Resilience First program fits this thesis by tightening links between property management, restoration and insurance, but it does not materially change the near term catalysts or the key risks around macro-sensitive organic growth and weather-driven restoration volatility.

The recent launch of a resident insurance solution with FirstService Insurance Brokers and VIU by HUB is particularly relevant here, because it sits alongside Resilience First as another service that could deepen client engagement and broaden recurring revenue streams tied to insurance readiness and risk support, reinforcing the existing growth drivers in Residential.

Yet, against this backdrop, investors also need to weigh the ongoing volatility tied to weather driven restoration work and how that could...

Read the full narrative on FirstService (it's free!)

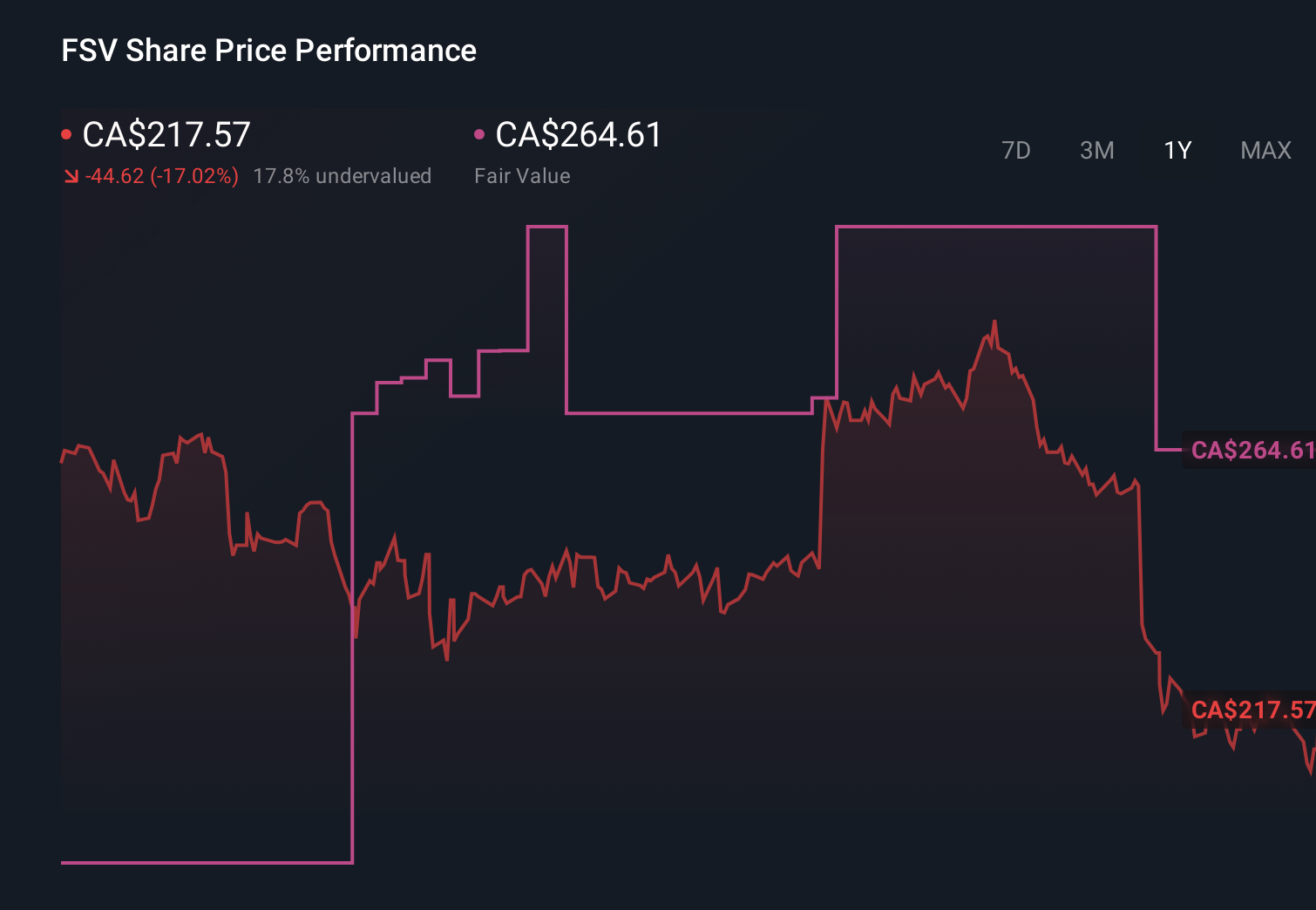

FirstService’s narrative projects $6.6 billion revenue and $256.8 million earnings by 2029. This requires 5.8% yearly revenue growth and about a $94.6 million earnings increase from $162.2 million today.

Uncover how FirstService's forecasts yield a CA$248.69 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Two Simply Wall St Community fair value estimates cluster between CA$214.57 and CA$248.69, underscoring how differently individual investors can size up FirstService. Against that range, the dependence on weather related restoration volumes remains a central issue you may want to test in several contrasting views.

Explore 2 other fair value estimates on FirstService - why the stock might be worth as much as 23% more than the current price!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your FirstService research is our analysis highlighting 3 key rewards and 1 important warning sign that could impact your investment decision.

- Our free FirstService research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate FirstService's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

The market won't wait. These fast-moving stocks are hot now. Grab the list before they run:

- AI is about to change healthcare. These 7 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- Capitalize on the AI infrastructure supercycle with our selection of the 52 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- The latest GPUs need a type of rare earth metal called Terbium and there are only 30 companies in the world exploring or producing it. Find the list for free.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com