Is WisdomTree's New Space ETF WSPC a Sign WT Is Doubling Down on Thematics?

- Earlier this week, WisdomTree, Inc. launched the WisdomTree Space Economy Fund (WSPC) on Nasdaq with a 0.75% expense ratio, offering actively managed exposure to global companies tied to launch services, satellite infrastructure, defense space systems, and emerging orbital technologies.

- This ETF adds another specialist theme to WisdomTree’s expanding lineup of differentiated products, underscoring its push into higher-conviction areas such as the space economy alongside existing quantum, AI, and robotics strategies.

- Against this backdrop, we’ll explore how the new space economy ETF fits into WisdomTree’s broader growth story in thematic and alternative products.

We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

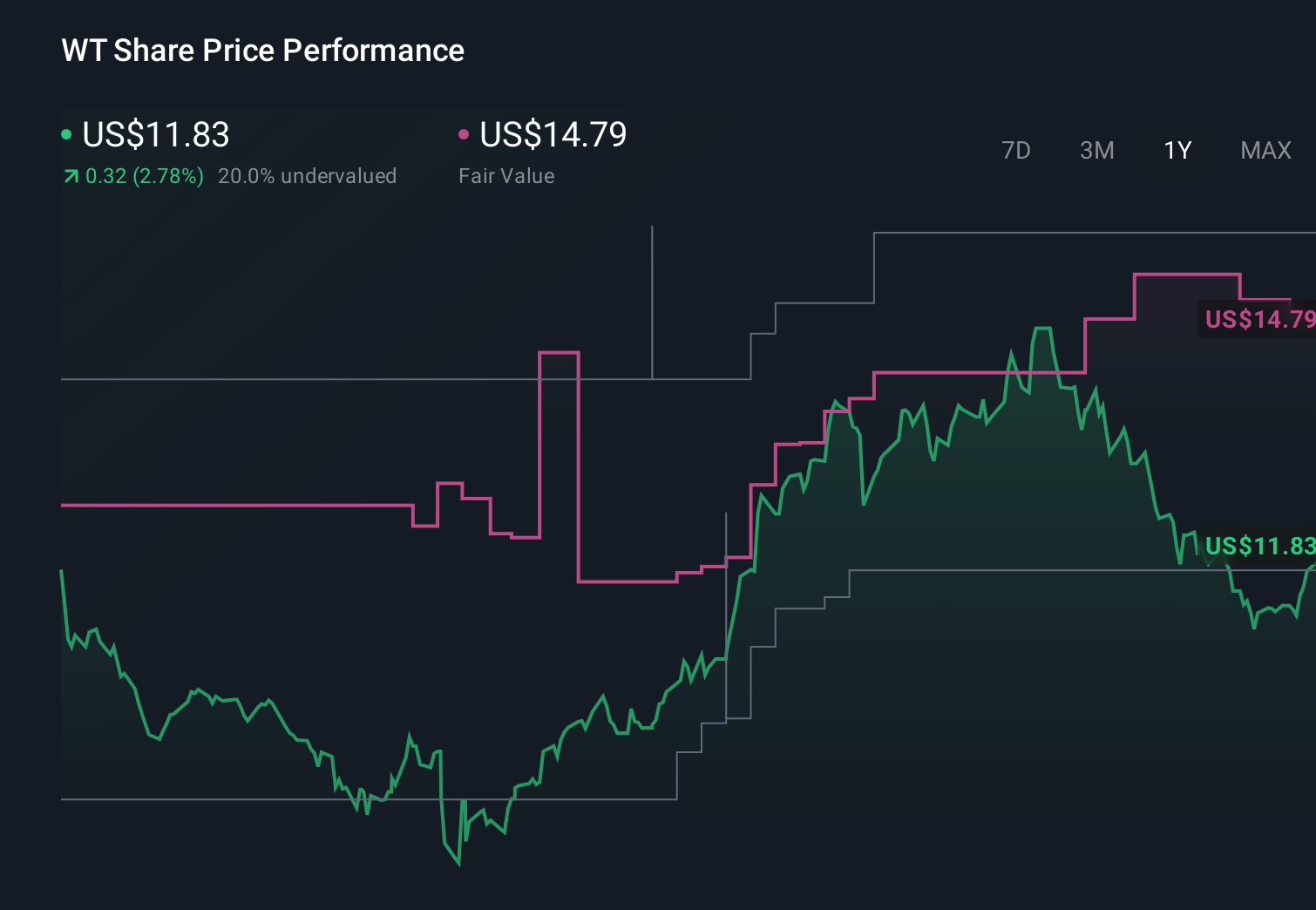

WisdomTree Investment Narrative Recap

To own WisdomTree, you need to believe it can keep growing fee revenues by standing out in crowded ETFs, thematics, and digital assets, while managing industry fee pressure and product complexity. The WSPC launch is consistent with that product expansion story but does not materially change the near term focus on sustaining organic inflows and managing earnings volatility after the recent quarterly net loss.

The most relevant backdrop to WSPC is WisdomTree’s recent update showing about US$9 billion of net inflows year to date and a roughly 13 percent annualized organic growth rate, with strong demand for quantum, AI, robotics, and alternatives. WSPC extends that same high conviction thematic playbook into space, adding another differentiated sleeve that could matter more over time if those inflow trends continue.

Yet beneath the headline growth, one risk investors should be aware of is how fee compression and higher cost, complex themes like space ETFs could...

Read the full narrative on WisdomTree (it's free!)

WisdomTree's narrative projects $905.2 million revenue and $303.1 million earnings by 2029. This requires 18.4% yearly revenue growth and an earnings increase of about $242.5 million from $60.6 million today.

Uncover how WisdomTree's forecasts yield a $19.97 fair value, a 4% upside to its current price.

Exploring Other Perspectives

More cautious analysts were already projecting revenue of about US$880.7 million and earnings of roughly US$269.6 million by 2029, so if you see WSPC as reinforcing WisdomTree’s product innovation catalyst, it is worth asking whether those lower end assumptions still feel too pessimistic or perhaps not cautious enough.

Explore 3 other fair value estimates on WisdomTree - why the stock might be worth as much as $19.97!

The Verdict Is Yours

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your WisdomTree research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

- Our free WisdomTree research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate WisdomTree's overall financial health at a glance.

Ready For A Different Approach?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- This technology could replace computers: discover 26 stocks that are working to make quantum computing a reality.

- The future of work is here. Discover the 31 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com