How Index Inclusion And Mixed Earnings Signals At Conagra Brands (CAG) Has Changed Its Investment Story

- Conagra Brands, Inc. was recently added to the Russell Small Cap Comp Value Index and is expected to report quarterly earnings of US$0.46 per share on revenues of US$2.88 billion, compared with the same quarter last year.

- This combination of index inclusion and analyst expectations for lower earnings per share but higher sales puts a spotlight on how Conagra is balancing profitability with revenue growth.

- Next, we’ll explore how Conagra’s addition to the Russell Small Cap Comp Value Index may influence its existing investment narrative and outlook.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Conagra Brands Investment Narrative Recap

To own Conagra Brands, you need to believe in the resilience of its packaged food portfolio and its ability to turn sales into sustainable earnings. The index additions spotlight the stock but do not materially change the key near term story, which still hinges on stabilizing margins amid cost pressures, while the biggest risk remains inflation, tariffs, and regulation squeezing an already thin profitability base.

Among recent announcements, the ongoing US$0.35 per share quarterly dividend stands out alongside index changes. Together, they frame Conagra as a company trying to balance shareholder returns with operational rebuilding at a time when analysts expect quarterly earnings of US$0.46 per share on US$2.88 billion of revenue, putting additional attention on how well cash flows can support both investment needs and payouts.

Yet beneath the index headlines, investors should be aware of how persistent input cost inflation could still...

Read the full narrative on Conagra Brands (it's free!)

Conagra Brands' narrative projects $11.3 billion revenue and $834.3 million earnings by 2029. This assumes fairly flat yearly revenue growth and an earnings increase of about $877.6 million from -$43.3 million today.

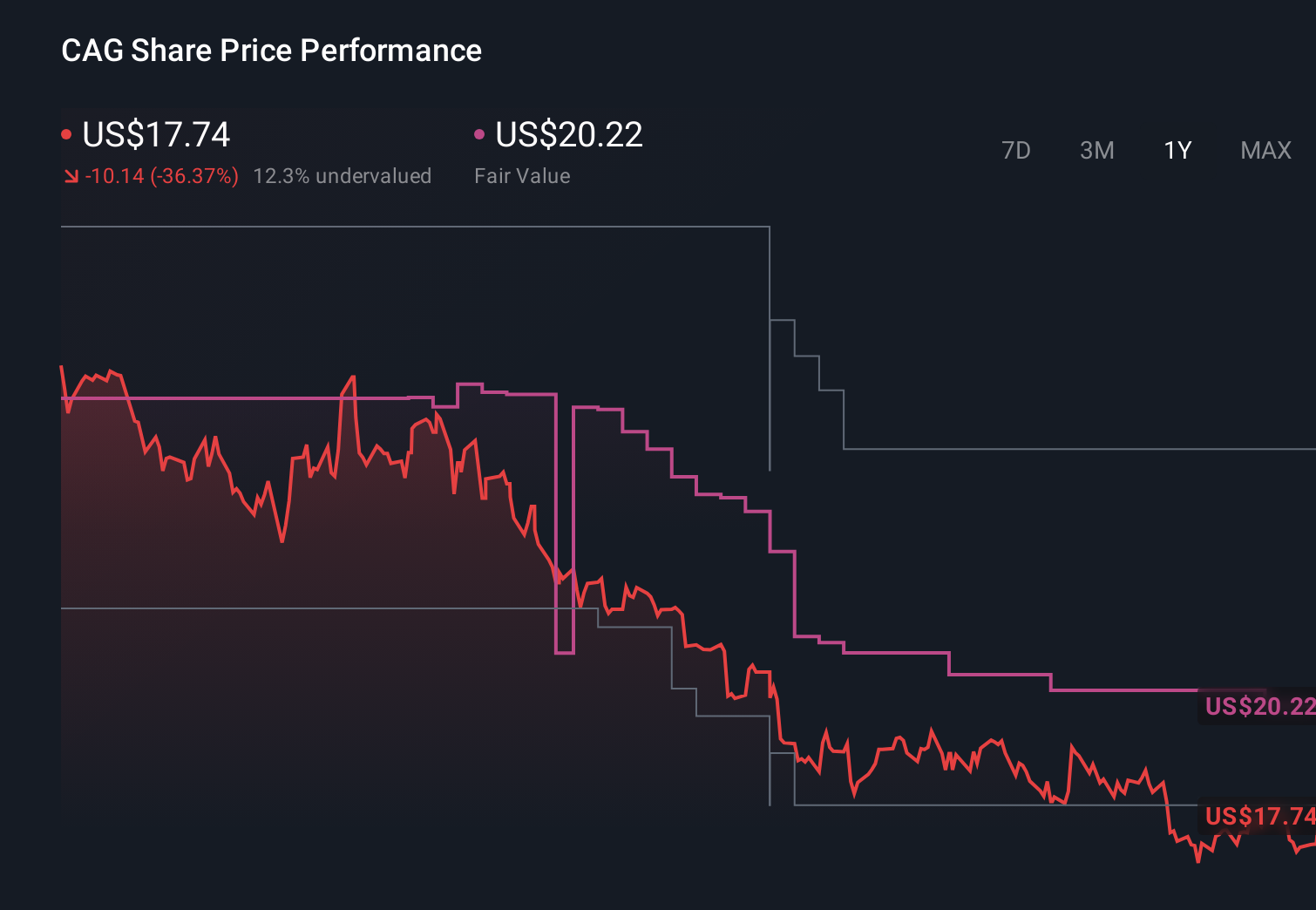

Uncover how Conagra Brands' forecasts yield a $14.59 fair value, a 6% upside to its current price.

Exploring Other Perspectives

Compared with the baseline view, the most optimistic analysts sounded far more upbeat, expecting about US$11.5 billion of revenue and nearly US$980 million of earnings by 2029, while downplaying how Conagra’s heavy focus on processed foods could clash with shifting consumer preferences.

Explore 10 other fair value estimates on Conagra Brands - why the stock might be worth just $14.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Conagra Brands research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Conagra Brands research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Conagra Brands' overall financial health at a glance.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

- We've uncovered the 9 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 16 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com