Can Merck (MRK) Be A Bargain If Earnings Look Fair?

Merck stock has delivered an 85.1% total return over the past five years, yet the current checks send a mixed message, with a Discounted Cash Flow (DCF) intrinsic value estimate pointing to meaningful upside while the broader valuation score is less conclusive.

- Over five years, Merck is up 85.1%, which puts recent valuation questions into the context of a strong long term run.

- Regulatory approvals and late stage pipeline progress can support expectations for future cash flows, while setbacks in areas like Alzheimer’s research and regulatory or political scrutiny may limit how much investors are willing to pay for that growth.

- Merck scores 3 out of 6 on the value checks, which points to a mixed picture rather than a clear bargain or clear overvaluation.

The issue now is whether Merck’s recent share price leaves enough upside relative to the DCF based intrinsic value estimate to justify the risk in the current setup.

Is Merck a Bargain on Cash Flow?

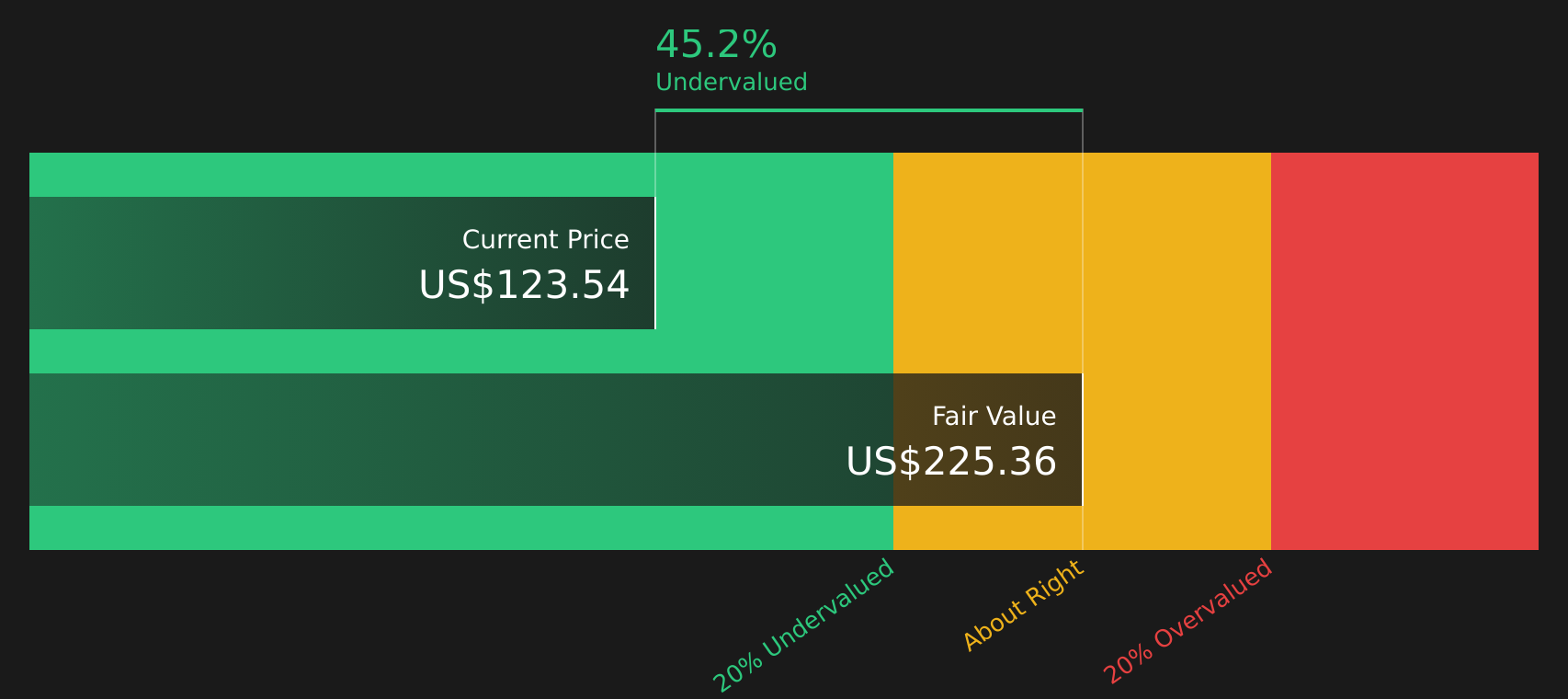

The Discounted Cash Flow (DCF) model estimates what Merck’s future cash generation could be worth in today’s dollars. Merck produced about $14.0b in free cash flow over the latest twelve months, and the model assumes that cash flows continue growing from this base rather than needing a turnaround. On that foundation, the 2 Stage Free Cash Flow to Equity approach points to an intrinsic value of about $225 per share.

Against a recent share price around $129, that implies the stock screens roughly 45.2% undervalued on this DCF view. The series of recent approvals and positive trial updates around KEYTRUDA and other pipeline assets helps explain why the cash flow outlook embedded in the model is relatively supportive. Because of that, Merck’s current price still sits well below what this cash flow based valuation suggests.

Overall, the Discounted Cash Flow model indicates Merck stock looks undervalued relative to its projected cash generation.

Our Discounted Cash Flow (DCF) analysis suggests Merck is undervalued by 45.2%. Track this in your watchlist or portfolio, or discover 44 more high quality undervalued stocks.

Where Does Merck Sit on Earnings?

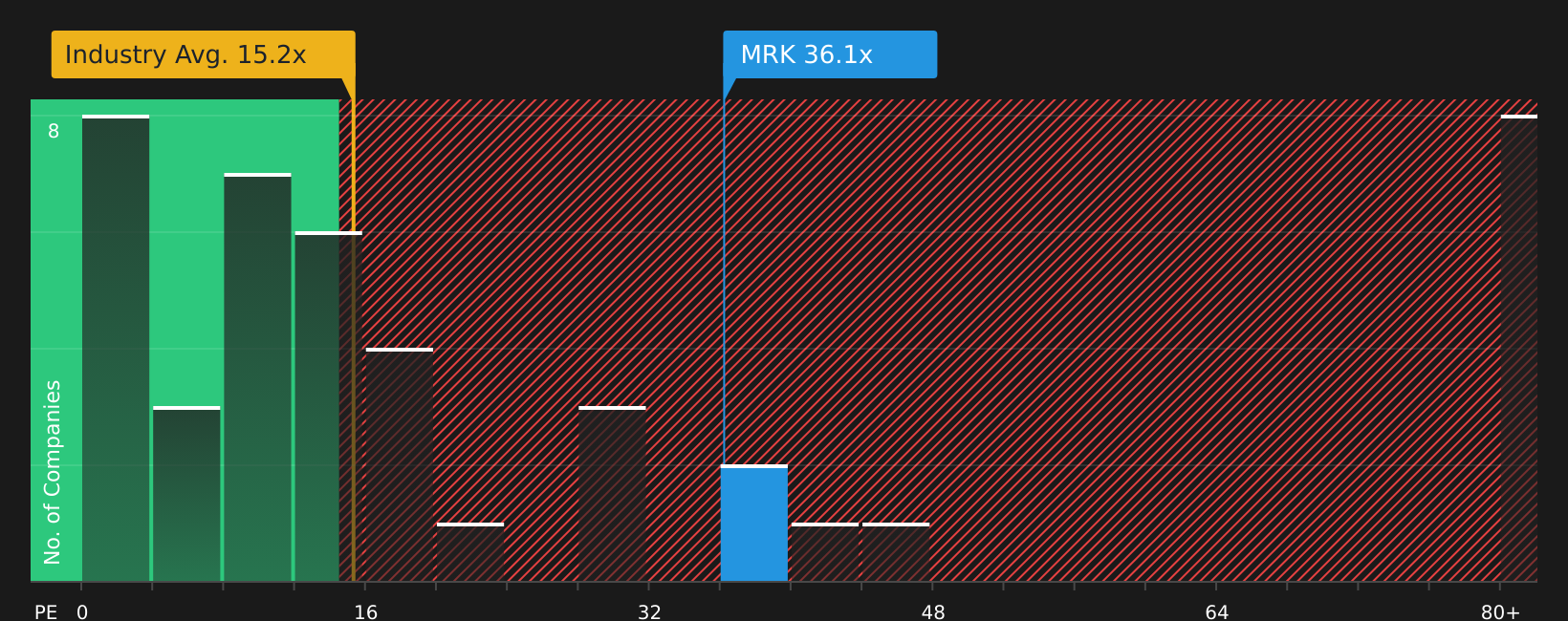

P/E is usually the cleanest quick check for a mature, profitable pharma group like Merck. The stock currently trades on a P/E of about 34.1x, compared with a Pharmaceuticals industry average near 14.9x and a peer group average around 26.5x, so investors are clearly paying a premium for Merck relative to many sector peers.

The tailored fair P/E ratio for Merck, which adjusts for its growth profile, margins, size and risk, sits at roughly 35.8x. That is only slightly above the current 34.1x. This suggests that while the stock is not cheap on headline numbers, the earnings multiple lines up reasonably well with what this framework implies for a company with Merck’s characteristics.

On the P/E test, Merck looks priced roughly in line with what this model suggests is a fair earnings multiple.

See what the numbers say about this price — find out in our valuation breakdown.

The Merck Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where this Merck valuation puzzle leaves off by spelling out which assumptions about Merck's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than today's price. They sit on Simply Wall St's Community page so you can see how that thinking evolves. Each narrative ties a fair value to a particular mix of potential catalysts and risks, giving you a clear story to track against what actually happens over time.

The community is split on Merck, with one camp focusing on the oncology pipeline and deals, and the other zeroing in on Keytruda dependence and pricing pressure.

Bull case: roughly fairly valued

"With its acquisition and licensing strategy, Merck has nearly tripled its late-phase pipeline since 2021, which is expected to have a potential commercial opportunity of over $50 billion by the mid-2030s, driving earnings growth…"

Read the full Bull Case to see why Merck could be undervalued

Bear case: 21% overvalued

"Merck remains heavily reliant on Keytruda, which is projected to face loss of exclusivity in late 2028 or early 2029, and the inability to fully offset this revenue cliff with new launches or pipeline progress could result in a sharp and sustained decline in top-line growth and long-term earnings, despite management's expectations that this will be a hill not a cliff…"

Read the full Bear Case to see why Merck could be overvalued

Do you think there's more to the story for Merck? Head over to our Community to see what others are saying!

The Bottom Line

For Merck, the Discounted Cash Flow (DCF) view points to meaningful upside, while the market-multiple view suggests the current P/E is roughly in line with what its profile might justify. That gap reflects how differently cash flow models and earnings multiples treat timing of cash generation, funding needs and investor sentiment. With the broader valuation checks sitting in mixed territory, the key question is whether Merck’s pipeline and post-Keytruda earnings path ultimately support the cash flow path implied by the intrinsic value estimate, or whether current enthusiasm already captures most of that potential.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com