AMETEK (AME) Could Be 10% Undervalued Following Its Acquisition Led Growth Narrative

AMETEK (AME) is back on investor radars after recent share moves and fresh performance data highlighted its position in electronic instruments and electromechanical devices, prompting a closer look at the stock’s current profile.

See our latest analysis for AMETEK.

Over the past year, AMETEK has combined relatively steady recent trading, with a 30 day share price return of 5.5% and year to date share price return of 11.88%, alongside stronger longer term momentum reflected in a 1 year total shareholder return of 30.11% and 5 year total shareholder return of 77.43%. This suggests recent moves are being interpreted through the lens of an already solid multi year experience for investors.

If AMETEK’s profile has you thinking about other industrial technology opportunities, this can be a good moment to scan the market for 34 power grid technology and infrastructure stocks

Those recent AMETEK gains can be read two ways: either as the market reaffirming confidence in a growing electronic instruments and electromechanical business, or as sentiment stretching expectations, which puts the valuation in sharper focus next.

Most Popular Narrative: 9.7% Undervalued

With AMETEK’s last close at $233.98 against a narrative fair value of $259.05, the most followed storyline frames the stock as undervalued and closely links that view to acquisition driven growth and execution.

Ongoing successful execution of a disciplined M&A strategy, leveraging a robust acquisition pipeline and significant balance sheet capacity, provides a catalyst for compounding top-line and EPS growth, while integration synergies and operational excellence drive expansion of operating and EBITDA margins.

Want to see what sits behind that confidence in AMETEK’s deal making, margin profile and future earnings power? The full narrative spells out the revenue, profit and valuation assumptions that underpin this fair value call.

Result: Fair Value of $259.05 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, AMETEK’s story can shift quickly if acquisition integration underwhelms or if continued softness in semiconductor and research end markets weighs on organic demand and margins.

Find out about the key risks to this AMETEK narrative.

Another View: AMETEK Through a Cash Flow Lens

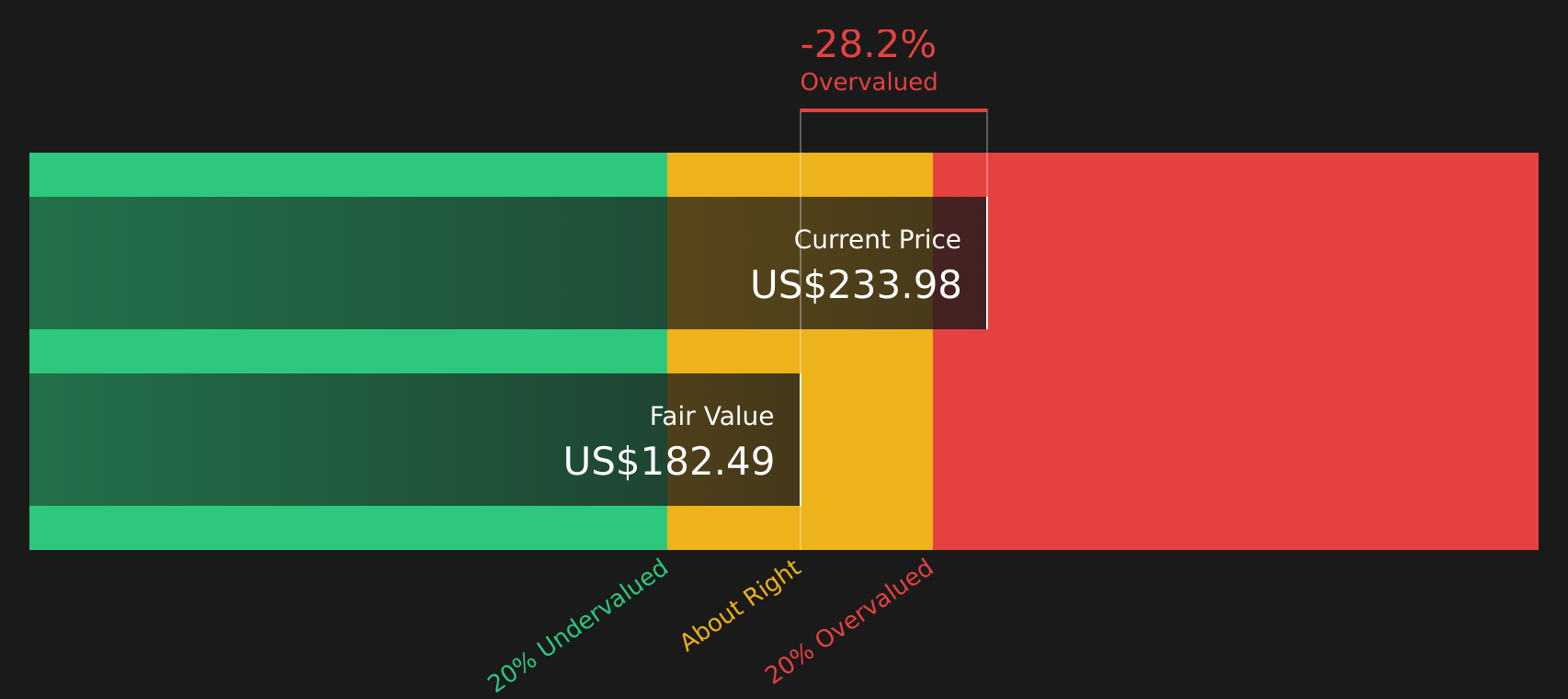

While the analyst narrative points to a fair value of $259.05, Simply Wall St's DCF model presents a different perspective, with an estimate of $181.20 versus AMETEK's recent $233.98 share price. This frames the stock as expensive rather than 9.7% undervalued. Which set of assumptions do you find more realistic for the long term?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out AMETEK for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 44 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

If this mix of optimism and caution around AMETEK has you thinking, use the data while it is fresh and form your own stance by reviewing the 3 key rewards.

Looking for more investment ideas beyond AMETEK?

Before you move on, take a moment to widen your watchlist using fresh stock ideas surfaced by the Simply Wall St Screener so you do not miss opportunities that fit your style.

- Zero in on potential bargains by scanning companies that combine quality fundamentals with attractive prices through the 44 high quality undervalued stocks.

- Strengthen your income focus by reviewing companies offering robust yields and payout profiles via the 9 dividend fortresses.

- Prioritize resilience and capital preservation by filtering for companies with lower risk scores using the 76 resilient stocks with low risk scores.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com