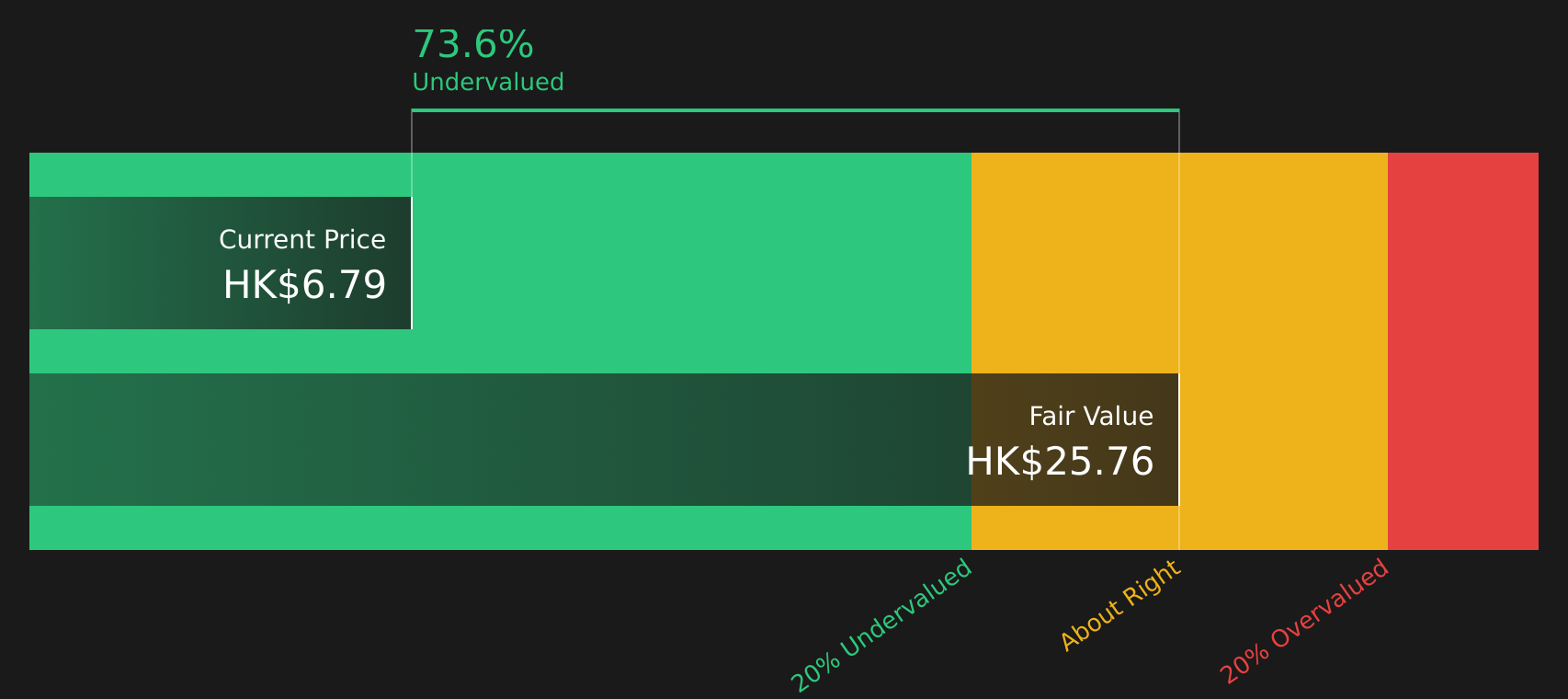

Greentown China Holdings (SEHK:3900) Could Be 74% Below Fair Value On Fresh Sales Update

Greentown China Holdings (SEHK:3900) has released unaudited sales figures for June and the first half of 2026, giving investors fresh detail on contracted volumes, pricing and project management activity.

See our latest analysis for Greentown China Holdings.

Following these June sales figures, Greentown China Holdings’ share price has softened, with a 30 day share price return of 18.68% and a 1 year total shareholder return decline of 33.04%, suggesting recent momentum has been weak despite ongoing project activity.

If these sales updates have you rethinking where growth could come from next, it may be worth scanning other opportunities through the 107 top founder-led companies

Greentown China Holdings’ share price has retreated while analyst targets and some intrinsic value estimates sit materially higher. This leaves a wide gap between trading levels and implied fair value. How does that spread look when broken down by the numbers?

Preferred Price-to-Sales of 0.1x: Is it justified?

On simple sales-based metrics, Greentown China Holdings screens as inexpensive, with a current Price-to-Sales (P/S) ratio of 0.1x while also trading at a wide discount to several fair value estimates.

The P/S ratio compares the company’s market value with its revenue, giving you a sense of how much investors are paying for each unit of sales. For a business like Greentown China Holdings that is heavily focused on property development in the People’s Republic of China, revenue tends to be influenced by project delivery cycles, contracted sales, and timing of revenue recognition, so a low P/S may reflect both cyclical headwinds and investor caution.

Relative to peers, the 0.1x P/S ratio stands well below the Hong Kong Real Estate industry average of 0.6x and also below an estimated fair P/S ratio of 0.5x. That gap suggests the market is pricing Greentown China Holdings at a steep discount to both comparable stocks and a level the P/S multiple could potentially gravitate toward if sentiment or fundamentals shift.

Explore the SWS fair ratio for Greentown China Holdings

Result: Price-to-Sales of 0.1x (UNDERVALUED)

However, this gap could persist if Greentown China Holdings’ revenue continues to decline or if weak recent share price returns further weigh on sentiment.

Find out about the key risks to this Greentown China Holdings narrative.

Another View: What The SWS DCF Model Says About Greentown China Holdings

While the low 0.1x P/S ratio makes Greentown China Holdings look inexpensive, the SWS DCF model points in the same direction, with an estimated future cash flow value of HK$25.74 per share versus the current HK$6.79 price, suggesting the stock screens as undervalued on cash flows too. If both sales and cash flow signals agree, the question becomes what risk the market is still pricing in.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Greentown China Holdings for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 211 high quality undervalued stocks. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Next Steps

With sentiment clearly mixed around Greentown China Holdings, now is the time to look through the data yourself, weigh the trade offs, and decide how the balance of risks and rewards sits for your portfolio via the 3 key rewards and 3 important warning signs

Looking for more investment ideas beyond Greentown China Holdings?

If Greentown China Holdings has sharpened your focus on value, now is a good time to broaden your watchlist with other stocks that fit clear, disciplined criteria.

- Target potential upside by scanning companies that combine quality fundamentals with attractive valuations through the 211 high quality undervalued stocks.

- Strengthen your income stream by reviewing companies with higher yields and more resilient payouts via the 471 dividend fortresses.

- Prioritise stability by focusing on companies with healthier finances and dependable metrics using the solid balance sheet and fundamentals stocks screener (419 results).

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com