QBE Stock And 2 Australian Dividend Shares For Passive Income

Dividend Powerhouses, often grouped with Dividend Aristocrats, can be especially appealing when inflation trends, bond yields and growth expectations are all pulling investors in different directions. With central banks weighing their next moves and energy prices influencing both inflation and income assets, a screen that focuses on dividend yields above 5% that are well covered, growing and stable offers a clear, rules based way to seek income from equities. This article highlights three stocks from the Dividend Powerhouses screener that stand out on those measures and provides concrete ideas for further research.

CSL (ASX:CSL)

Overview: CSL is a Melbourne based biopharmaceutical company that develops and manufactures plasma derived medicines, vaccines and treatments for conditions such as immune disorders, bleeding disorders, iron deficiency and kidney disease, serving patients and health systems across major global markets.

Operations: CSL generates most of its revenue from CSL Behring at about $10.9b, with additional contributions from CSL Vifor at about $2.4b and CSL Seqirus at about $2.2b. The United States, at about $7.3b, is its single largest geographic market within a broadly diversified global footprint.

Market Cap: A$60.1b

For income focused investors, CSL combines a 3.36% dividend yield with a large, globally scaled plasma and vaccines business, but it also comes with meaningful questions that cannot be ignored. Profit margins have compressed to 9.1%, the dividend is not well covered by earnings, and a large one off loss of $2.1b plus high debt and funding risk complicate the picture. At the same time, analysts see strong earnings growth potential, and Simply Wall St estimates suggest the stock trades well below fair value, implying upside if execution on restructuring, Vifor integration and governance changes is effective. The key question is whether CSL’s core plasma moat and future cash flows justify looking past the recent setbacks.

CSL’s compressed margins, uncovered dividend and one off A$2.1b loss sit next to a global plasma franchise that many investors may be underestimating, so it is worth reviewing the 2 key rewards and 4 important warning signs

QBE Insurance Group (ASX:QBE)

Overview: QBE Insurance Group is a global insurer headquartered in Sydney that underwrites general insurance and reinsurance across commercial and household property, motor, agriculture, liability, workers’ compensation, accident and health, marine, energy and aviation, as well as managing Lloyd’s syndicates and investment portfolios.

Operations: QBE generates most of its revenue from International at about $11.2b, followed by North America at about $8.2b, Australia Pacific at about $5.7b and Corporate & Other at about $77m.

Market Cap: A$38.2b

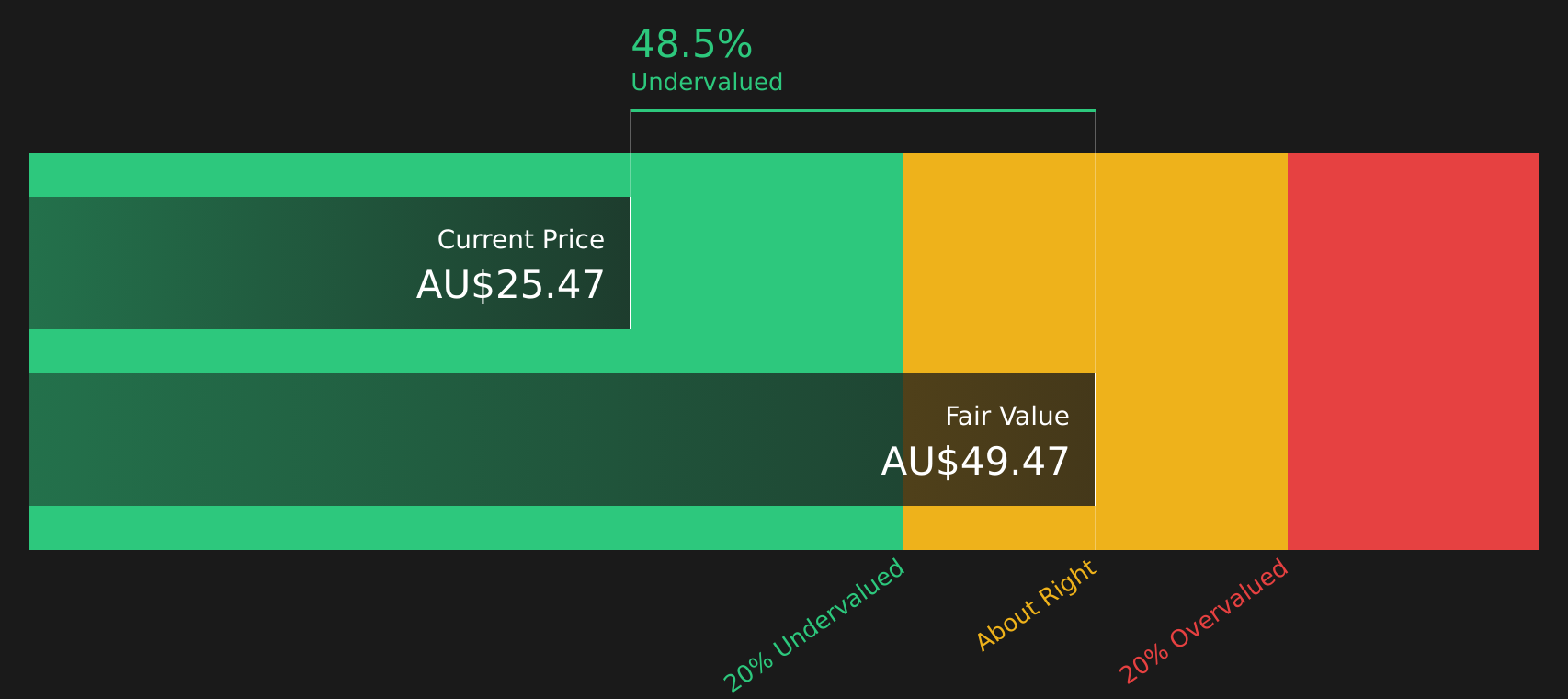

QBE Insurance Group appears in a dividend focused screen because it combines a global commercial insurance footprint, an 11.4% net margin and 18.5% Return on Equity with a share price that is described as trading well below estimated fair value. Earnings have grown 23.3% over the past year and 53.1% per year over five years. However, forecast growth is described as more muted, and the dividend record is described as unstable, which may be relevant for income-focused investors. In addition, QBE is described as pushing into faster growing markets like India and refining its capital structure, while still facing margin pressure from softer premium rates, catastrophe losses and higher funding risk. The relationship between the reported valuation gap, these quality metrics and the identified risks is presented as a key consideration for investors.

QBE Insurance Group’s mix of an 11.4% net margin, 18.5% Return on Equity and a share price described as well below estimated fair value hints at something the market may be missing; go through the 2 key rewards and 1 important warning sign

Evolution Mining (ASX:EVN)

Overview: Evolution Mining is an Australian based gold producer that explores, develops and operates gold and gold copper mines in Australia and Canada, selling gold and gold copper concentrates and also targeting copper and silver deposits.

Operations: Evolution Mining generates most of its revenue from Cowal at about A$1.7b and Ernest Henry at about A$1.1b, with additional contributions from Mungari at about A$780m, Red Lake at about A$670m, Northparkes at about A$580m, Mt Rawdon at about A$150m and Corporate at about A$160m.

Market Cap: A$22.9b

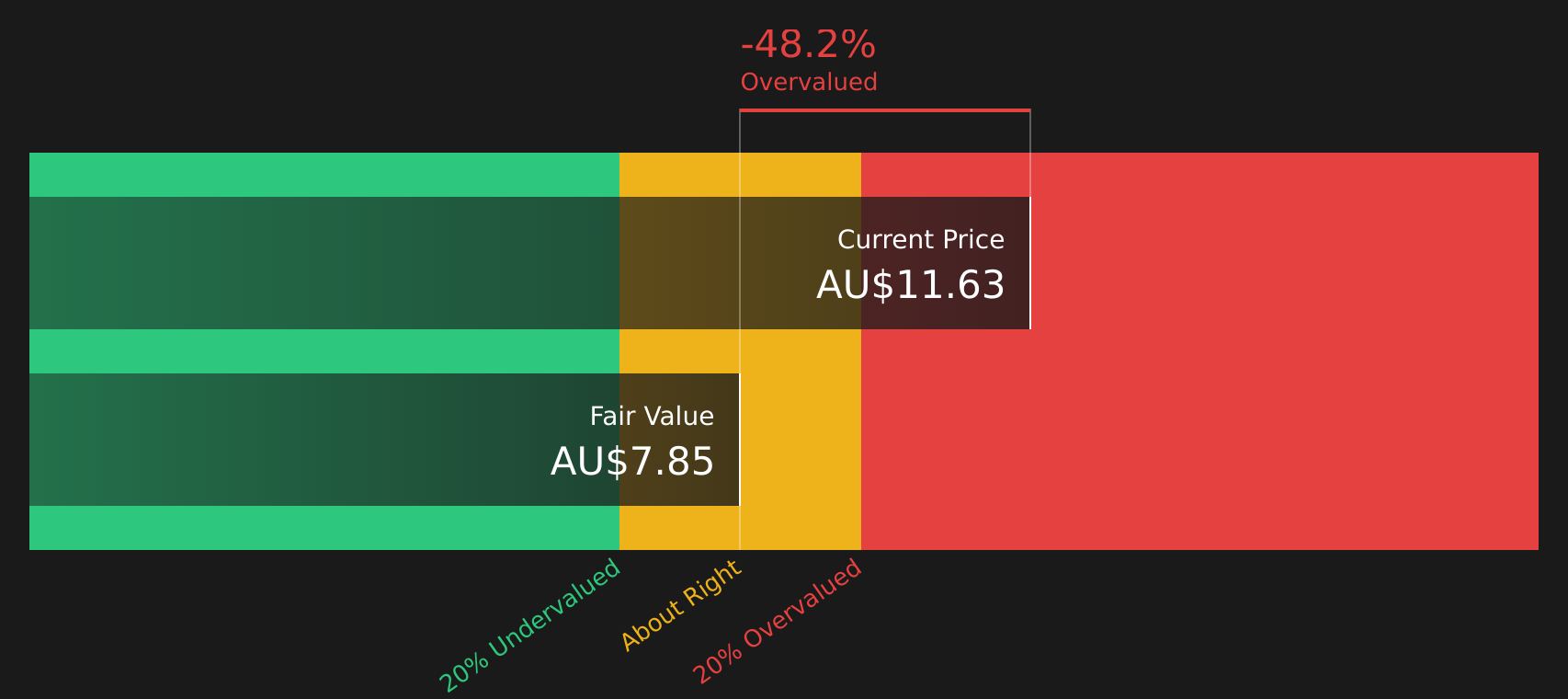

Income focused investors may find Evolution Mining interesting because it combines high quality earnings and strong profitability, with a 26% net margin and Return on Equity above 20%, together with leverage to both gold and fast developing battery metals through its lithium joint venture at Nevada North. At the same time, forecast earnings and revenue growth are slower than the broader Australian market, the dividend record is described as unstable and the balance sheet is fully funded by higher risk external borrowing. As a result, the current P/E premium over estimated fair value leaves less room for error. The key question is whether resilient margins, long mine lives and the lithium option justify accepting those funding and valuation risks in a dividend focused portfolio.

Evolution Mining’s resilient margins and lithium exposure may be masking a very different risk reward profile than a typical gold producer, so it is worth reading the analysis report for Evolution Mining

The three stocks covered here are only the starting point, as the full Dividend Powerhouses screen surfaced 27 more companies with 3%+ yields and equally compelling income narratives, each with its own mix of strengths and trade offs to weigh. To identify the highest conviction ideas for your watchlist, use Simply Wall St to analyze and filter the catalysts, dividend coverage metrics and risk factors discussed here across the full Dividend Powerhouses (3%+ Yield) screener.

Take Control of Your Investment Journey

If QBE Insurance Group or any of these companies have caught your attention, register for FREE with Simply Wall St and add your companies to a Watchlist to monitor the share price against the fair value and track any new developments as they happen. Once you've made your move, manage your holdings with our Portfolio Command Center that filters out the noise to deliver only the most critical, actionable updates. Throughout your journey, our Community allows you to filter the best ideas from thousands of investor perspectives. By uncovering hidden catalysts and risks early, you'll accelerate your decision-making and stay one step ahead of the market.

Seeking Fresh Alternatives Before They Fly?

Fresh opportunities can move from quiet accumulation to full breakout before most investors even notice. Use these curated stock lists while it matters, before momentum gets fully caught, and consider taking action promptly.

- Spot companies building real AI momentum and use the 63 profitable AI stocks that aren't just burning cash to focus on businesses already turning that excitement into actual profits instead of just burning cash.

- Track the power grid upgrade story as it unfolds by scanning the 34 power grid technology and infrastructure stocks that zeroes in on enablers of transmission, reliability and electrification demand.

- Position ahead of the robotics adoption curve with the 31 robotics and automation stocks that highlights companies automating factories, logistics and workflows while the theme still flies under the radar for now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com