Undiscovered Gems in Asia to Explore This July 2026

As global markets navigate mixed economic signals, with the U.S. labor market showing signs of cooling and China's manufacturing activity demonstrating resilience, investors are increasingly turning their attention to Asia's small-cap landscape for potential opportunities. In this environment, identifying promising stocks often involves seeking companies with robust fundamentals and growth potential that can withstand broader market fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| CNMC Goldmine Holdings | 0.84% | 32.52% | 78.36% | ★★★★★★ |

| Transcend Information | NA | 4.45% | 25.56% | ★★★★★★ |

| DeHua TB New Decoration MaterialLtd | 0.63% | 1.50% | 2.14% | ★★★★★★ |

| Nippon Carbide Industries | 16.74% | 1.99% | -4.81% | ★★★★★★ |

| Hyundai Home Shopping Network | 6.43% | 16.06% | -2.84% | ★★★★★★ |

| Zhejiang Jolly PharmaceuticalLTD | 21.31% | 17.83% | 29.70% | ★★★★★☆ |

| Magnate Technology | 77.36% | 10.92% | 35.95% | ★★★★★☆ |

| Sing Investments & Finance | 0.15% | 7.06% | 8.65% | ★★★★☆☆ |

| Shengda ResourcesLtd | 54.08% | 7.99% | 3.75% | ★★★☆☆☆ |

| Regina Miracle International (Holdings) | 132.81% | 0.48% | -15.87% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

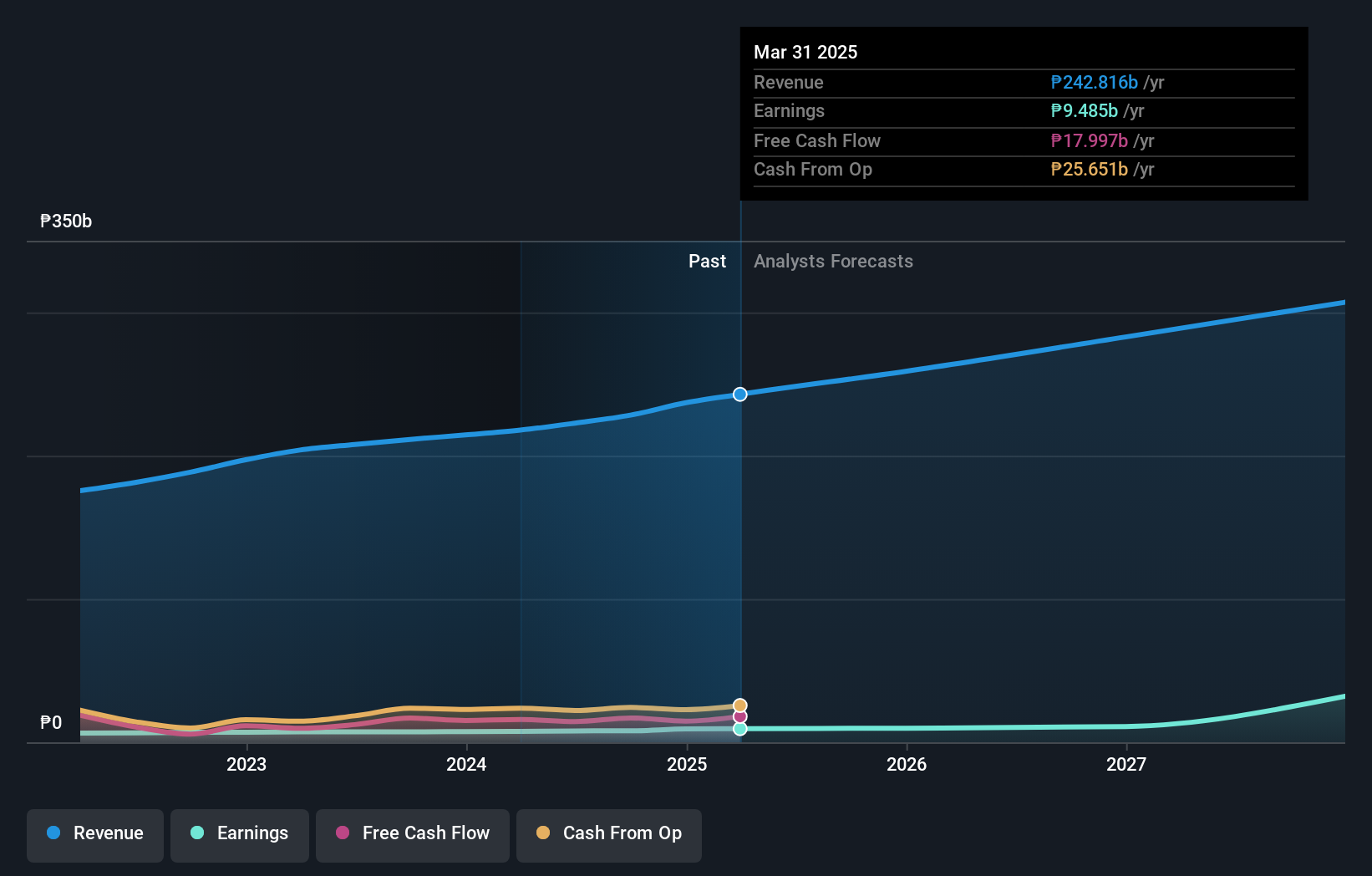

Cosco Capital (PSE:COSCO)

Simply Wall St Value Rating: ★★★★★★

Overview: Cosco Capital, Inc. operates in the Philippines across various sectors including retail, real estate, liquor distribution, and oil and mineral exploration with a market capitalization of approximately ₱58.20 billion.

Operations: The company generates significant revenue primarily from grocery retail at ₱248.82 billion, followed by liquor distribution contributing ₱20.44 billion. Specialty retail and real estate add smaller portions of ₱2.14 billion and ₱2.24 billion, respectively, while energy, oil, and mining contribute a modest ₱476 million to the overall revenue stream.

Cosco Capital, a notable player in the consumer retailing sector, has demonstrated robust financial health with its debt-to-equity ratio dropping from 14.8% to 7.1% over five years. Its earnings grew by 3.5% last year, outpacing the industry average of 2.4%. Trading at a substantial discount of 85% below its estimated fair value suggests potential undervaluation. Recent quarterly results showed sales reaching PHP 63 billion and net income rising to PHP 4.47 billion from PHP 3.68 billion year-on-year, indicating strong operational performance despite market challenges and recent board changes enhancing corporate governance dynamics.

- Unlock comprehensive insights into our analysis of Cosco Capital stock in this health report.

Examine Cosco Capital's past performance report to understand how it has performed in the past.

Luye Pharma Group (SEHK:2186)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Luye Pharma Group Ltd. is engaged in the development, production, marketing, and sale of pharmaceutical products across China, the United States, Europe, and other international markets with a market capitalization of approximately HK$7.63 billion.

Operations: Luye Pharma generates revenue primarily from oncology drugs (CN¥2.30 billion), central nervous system drugs (CN¥2.03 billion), and cardio-vascular system drugs (CN¥1.15 billion).

Luye Pharma Group, a nimble player in the pharmaceutical sector, is making waves with its innovative drug LY03015. This groundbreaking treatment for tardive dyskinesia (TD) has completed a successful phase 2 clinical trial in China, showing a response rate of up to 76.5%. The company's net debt to equity ratio stands at 15%, reflecting prudent financial management over five years as it reduced from 122.9% to 55.8%. Despite interest payments being covered only 2.3 times by EBIT, earnings grew by an impressive 31.1% last year, outpacing industry growth and highlighting Luye's potential for future expansion in CNS therapeutics.

- Click to explore a detailed breakdown of our findings in Luye Pharma Group's health report.

Evaluate Luye Pharma Group's historical performance by accessing our past performance report.

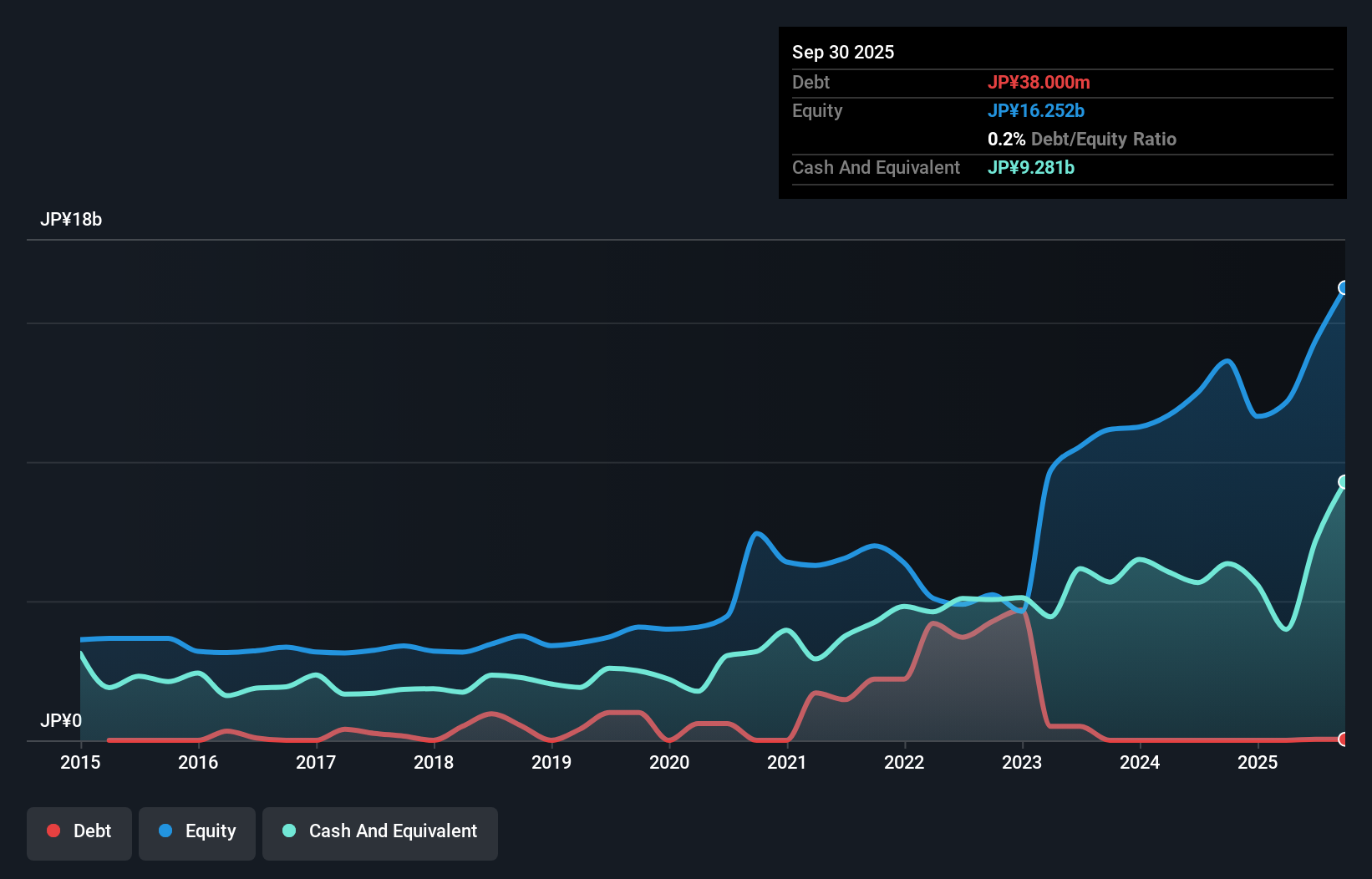

Cybozu (TSE:4776)

Simply Wall St Value Rating: ★★★★★★

Overview: Cybozu, Inc. is a Japanese company focused on the development, sale, and operation of groupware solutions with a market capitalization of approximately ¥121.30 billion.

Operations: The primary revenue stream for Cybozu comes from software development and sales, generating ¥38.92 billion. The company's financial performance is highlighted by a net profit margin that reflects its profitability within the groupware sector.

Cybozu has been making waves with its impressive financial performance and strategic initiatives. The company reported a notable earnings growth of 72% over the past year, significantly outpacing the software industry's 16%. Its debt-to-equity ratio has impressively shrunk from 27.1 to just 0.2 over five years, reflecting prudent financial management. Trading at nearly 44% below estimated fair value, Cybozu presents an attractive proposition in terms of valuation compared to peers. Recent share repurchases totaling ¥2,237 million for about 933,900 shares underscore a commitment to optimizing capital structure amidst its ongoing growth trajectory.

- Take a closer look at Cybozu's potential here in our health report.

Explore historical data to track Cybozu's performance over time in our Past section.

Next Steps

- Click here to access our complete index of 110 Asian Undiscovered Gems With Strong Fundamentals.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com