VinFast’s Asset-Light Pivot and Internal Restructuring Might Change The Case For Investing In VinFast Auto (VFS)

- In recent days, VinFast Auto completed the transfer of its equity interest in VinFast Trading and Production JSC and terminated a multi‑billion-share exchange agreement with Vingroup, advancing a shift to an asset-light structure focused on global R&D, technology, brand building, and sales.

- This restructuring marks a significant operational pivot that could reshape VinFast’s risk profile by separating capital-heavy manufacturing from its core corporate platform and changing internal ownership linkages.

- We’ll now examine how VinFast’s move toward an asset-light, globally focused model could influence the company’s existing investment narrative.

AI is about to change healthcare. These 40 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

VinFast Auto Investment Narrative Recap

To own VinFast today, you need to believe it can turn fast growing EV and two wheeler volumes into a financially sustainable, globally relevant brand. The shift to an asset light structure and the unwinding of the Vingroup share exchange speak directly to the key near term catalyst of improving capital efficiency, while also touching the biggest current risk around liquidity and dilution. Whether this restructuring meaningfully reduces cash burn or simply reshuffles exposure is still an open question.

Among recent announcements, the collaboration with NVIDIA and Autobrains on a Level 4 autonomous driving program is particularly relevant. As VinFast refocuses on R&D, technology and brand rather than heavy manufacturing, this kind of partnership shows where management wants investors to look for future differentiation, even as near term catalysts still hinge more on unit economics, cash runway and proving that the new structure can support international expansion at lower risk.

Yet behind this pivot, one issue investors should be aware of is the liquidity risk created by high cash burn and a limited cash runway...

Read the full narrative on VinFast Auto (it's free!)

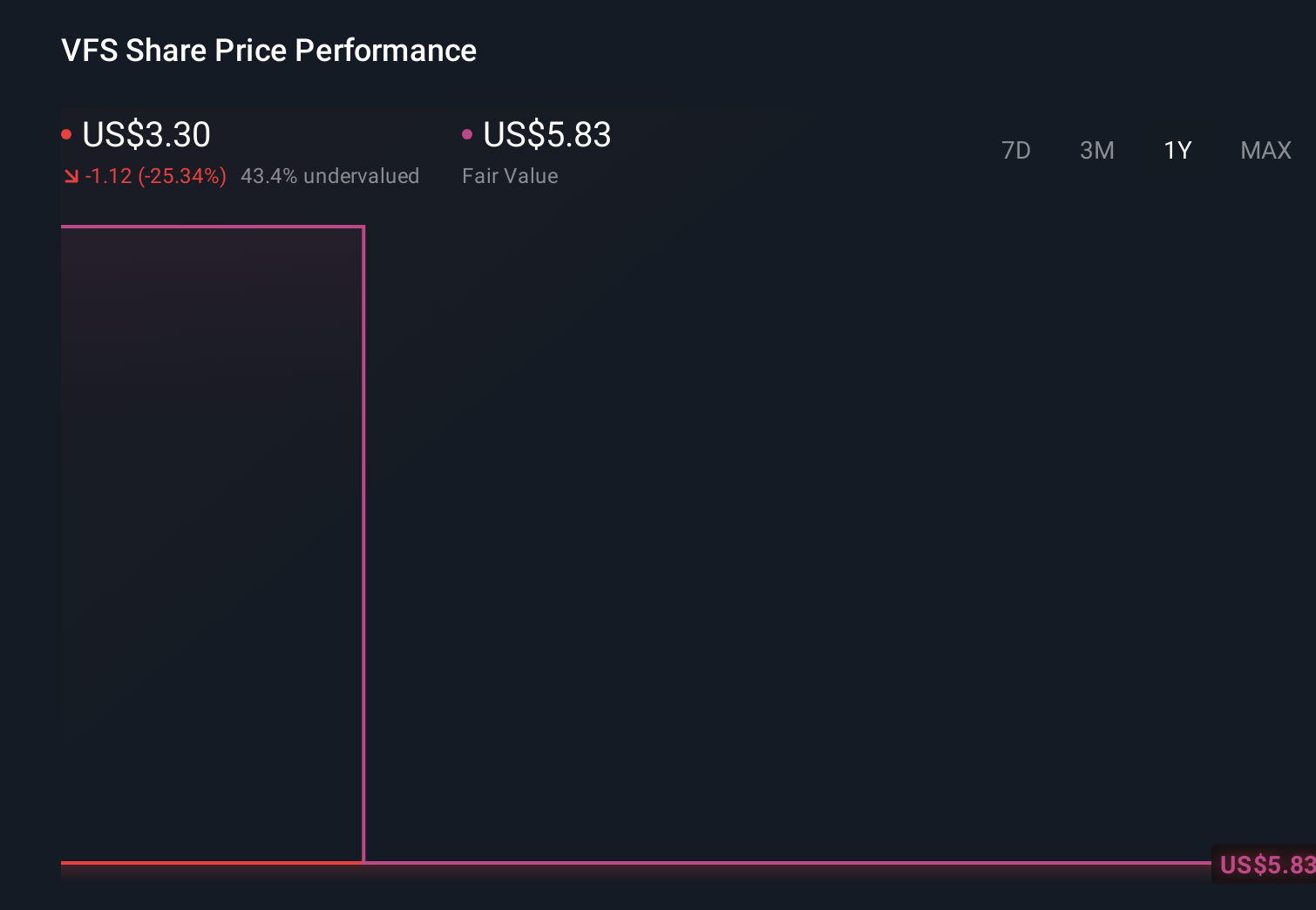

VinFast Auto's narrative projects ₫239006.9 billion revenue and ₫6230.1 billion earnings by 2029. This requires 38.4% yearly revenue growth and an earnings increase of about ₫105614.8 billion from -₫99384.7 billion today.

Uncover how VinFast Auto's forecasts yield a $6.30 fair value, a 105% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about ₫246,543.0 billion and earnings turn positive by 2029, which is far more upbeat than consensus. Set against the asset light pivot and ongoing heavy losses, this highlights how differently you and other shareholders might weigh the risk that high cash burn and funding needs could still limit how much of that growth story actually shows up in your returns.

Explore 4 other fair value estimates on VinFast Auto - why the stock might be worth less than half the current price!

Decide For Yourself

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your VinFast Auto research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

Want Some Alternatives?

These stocks are moving-our analysis flagged them today. Act fast before the price catches up:

- The future of work is here. Discover the 30 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

- Uncover the next big thing with 20 elite penny stocks that balance risk and reward.

- Invest in the nuclear renaissance through our list of 89 elite nuclear energy infrastructure plays powering the global AI revolution.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com