Merck (MRK) Stock Trades At A Discount To Cash Flow But A Premium To Earnings

Merck stock has delivered a strong 94.2% return over the past five years, yet the valuation checks send a mixed message, with the Discounted Cash Flow (DCF) estimate pointing to meaningful upside while the broader scorecard is less enthusiastic.

- Over five years, Merck has returned 94.2%, which puts more weight on whether today’s price still leaves room for attractive long term returns.

- Recent drug approvals and pipeline progress can support expectations for future cash flows, but regulatory, political and research setbacks may still change how much investors are willing to pay for that growth.

- Merck currently passes only 2 of 6 valuation checks, which leans more toward “not obviously cheap” rather than a clear bargain on the usual metrics.

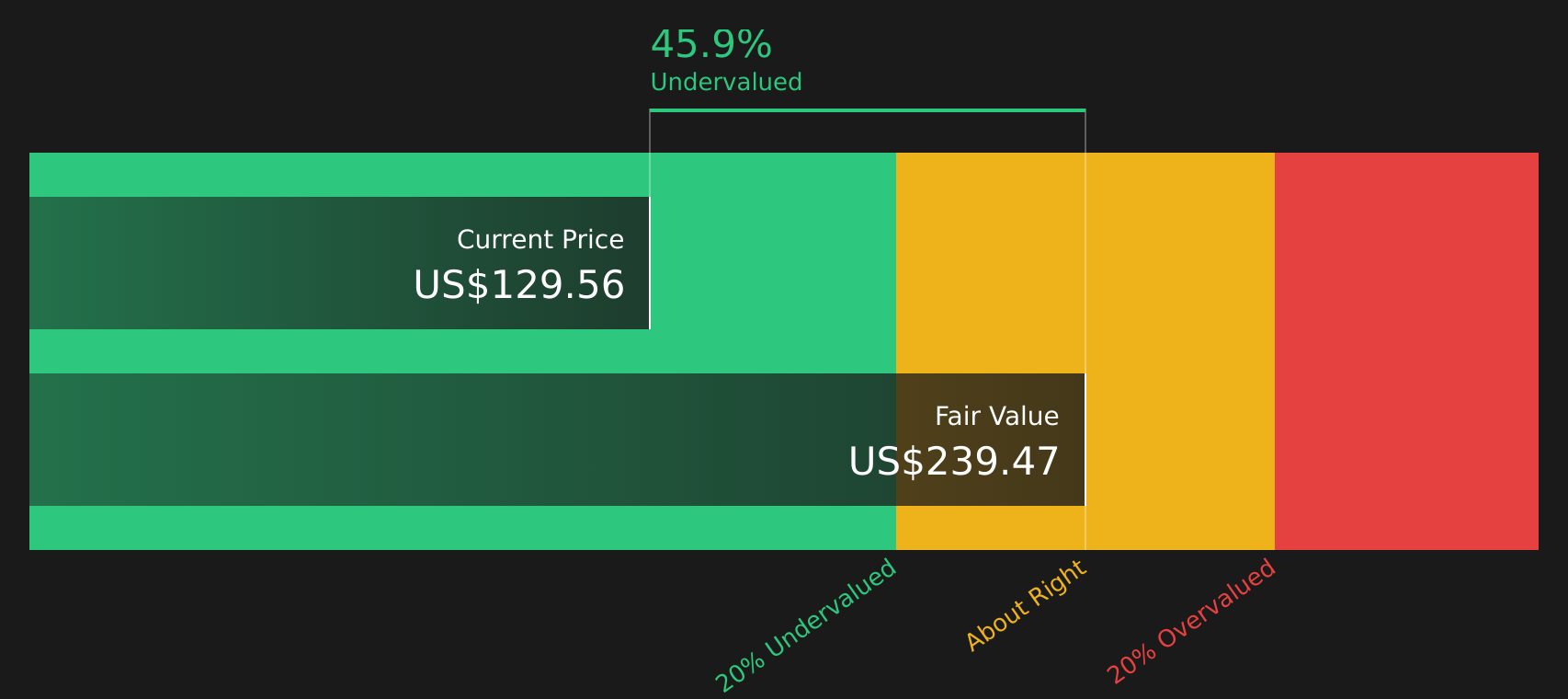

The issue now is whether the DCF based intrinsic value, which points to Merck as undervalued by 45.9%, or the low overall value score is the better guide for where the stock stands today.

Is Merck a Bargain on Cash Flow?

The Discounted Cash Flow (DCF) approach estimates what Merck is worth today based on the cash it could generate for shareholders over time. Merck currently produces about $14.0b in free cash flow over the latest twelve months, and the model assumes these cash flows keep growing rather than shrinking from here. On those inputs, the DCF points to an intrinsic value of about $239 per share.

That sits well above the current share price, implying Merck screens as roughly 45.9% undervalued on this cash flow view. The ongoing focus on expanding beyond KEYTRUDA through new approvals and pipeline assets, plus acquisitions, is consistent with the growth profile embedded in the cash flow projections. Because lawmakers are investigating Merck’s clinical trial work in China, some investors may be applying a risk discount that helps explain why the market price sits well below the model’s intrinsic value today.

On this DCF view, Merck stock currently appears undervalued relative to the cash flows the company is projected to generate.

Our Discounted Cash Flow (DCF) analysis suggests Merck is undervalued by 45.9%. Track this in your watchlist or portfolio, or discover 43 more high quality undervalued stocks.

Does Merck Look Fairly Valued on Earnings?

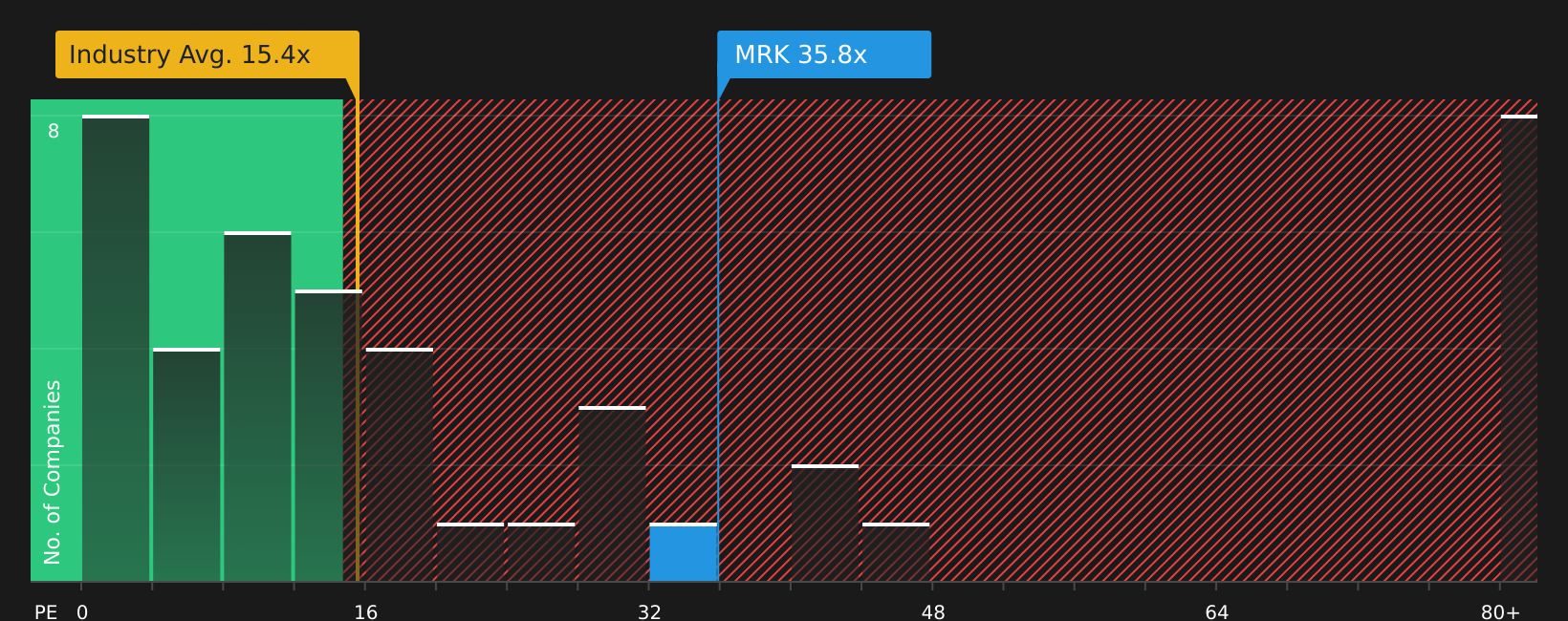

For a mature pharma group like Merck, the P/E ratio is often the cleanest snapshot of how much investors are paying for each dollar of earnings. Merck trades on a P/E of 35.8x, which is higher than the broader pharmaceuticals industry average of 15.4x and also above the peer average of 26.9x.

The fair P/E ratio implied by the model is 34.8x, only slightly below where Merck is currently priced. That small gap suggests the stock is neither clearly cheap nor stretched on earnings, once its scale, margins and risk profile are taken into account. The key question for you is whether Merck’s product mix, patent profile and research pipeline justify paying a premium to the sector while still sitting close to that modelled fair range.

On balance, Merck appears roughly fairly valued on its current P/E multiple.

See what the numbers say about this price — find out in our valuation breakdown.

The Merck Narrative: What Would Justify Today's Price?

Simply Wall St Narratives pick up where the Merck valuation puzzle leaves off by spelling out which assumptions about Merck's future growth, margins and earnings would need to hold for the stock to be worth materially more or less than its current price. Each one treats fair value as a thesis about the business that you can keep tracking over time rather than a static number, all housed on Simply Wall St's Community page.

Community views on Merck sit wide apart, with one camp focused on the enlarged oncology pipeline and another fixated on pricing and patent risks.

Bull case: roughly fairly valued

"With its acquisition and licensing strategy, Merck has nearly tripled its late-phase pipeline since 2021, which is expected to have a potential commercial opportunity of over $50 billion by the mid-2030s…"

Read the full Bull Case to see why Merck could be undervalued

Bear case: 27% overvalued

"Intensifying global pressure on drug pricing from policymakers, insurers, and patients, including the prospect of government-mandated price cuts and the impending impact of the Inflation Reduction Act, threatens to erode future revenue growth and compress net margins across Merck's flagship and pipeline products…"

Read the full Bear Case to see why Merck could be overvalued

Do you think there's more to the story for Merck? Head over to our Community to see what others are saying!

The Bottom Line

For Merck, the Discounted Cash Flow (DCF) estimate points to meaningful intrinsic value upside, while the earnings multiple suggests the stock is priced roughly in line with peers once its profile is factored in. The tension between an undervalued intrinsic value signal and weak broader valuation checks leaves the story finely balanced rather than a clear-cut bargain. What matters most from here is whether Merck can convert its pipeline and acquisitions into durable cash flows that justify the DCF outlook, or whether regulatory and pricing pressures indicate that the current discount is closer to a value trap than an opportunity.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com