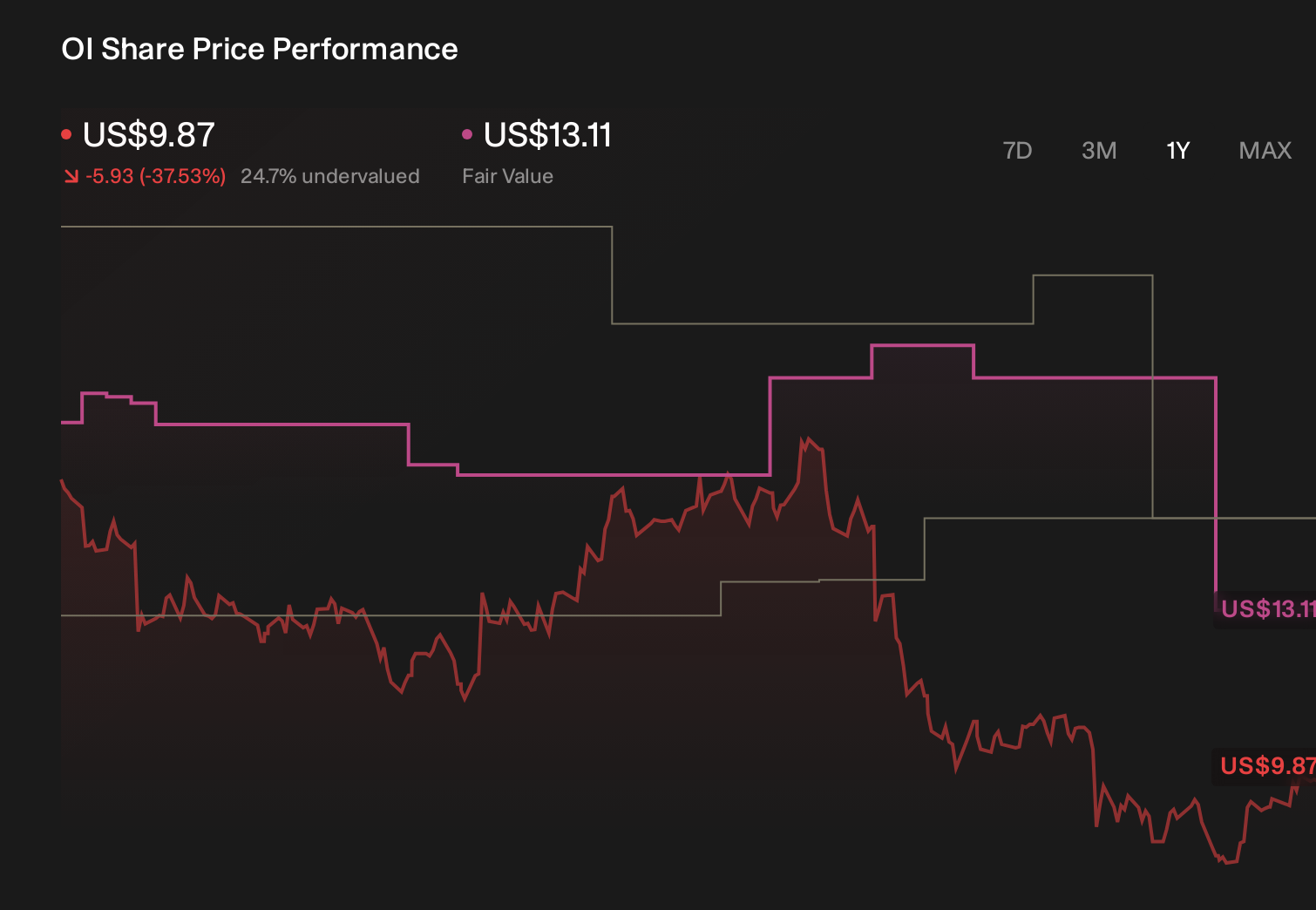

O-I Glass (OI) Is Down 11.3% After Cutting 2026 EPS Guidance on European Headwinds and Costs

- O-I Glass, Inc. reported first-quarter 2026 results with sales of US$1,540 million versus US$1,567 million a year earlier, and a net loss of US$73 million, widening from US$16 million, with basic and diluted loss per share from continuing operations at US$0.48 versus US$0.10.

- Alongside these weaker results, management cut full-year adjusted EPS guidance to US$1.00–US$1.50, citing energy cost inflation and ongoing competitive pressures in Europe despite ongoing Fit to Win cost savings progress.

- We’ll now examine how the lowered full-year earnings guidance and European market headwinds reshape O-I Glass’s existing investment narrative.

Find 51 companies with promising cash flow potential yet trading below their fair value.

O-I Glass Investment Narrative Recap

To own O-I Glass today, you need to believe that glass packaging can still earn acceptable returns despite structural pressure from alternative materials and rising production costs. The latest results and lower 2026 EPS guidance bring the key near term catalyst, Fit to Win driven cost savings, into sharper focus, while also underlining the biggest current risk: persistent European weakness and energy inflation that could keep the business in loss making territory.

The most relevant recent announcement here is the Q4 2025 and full year 2025 result, which already showed a full year net loss of US$129 million on US$6,426 million of sales. That backdrop makes the larger Q1 2026 loss and reduced EPS guidance feel less like a one off and more like a continuation of existing pressures, raising the bar for Fit to Win savings and network optimization to offset headwinds in Europe and higher energy costs.

Yet beneath the cost cutting story, investors should be aware of how sustained energy inflation could interact with O-I Glass's already high...

Read the full narrative on O-I Glass (it's free!)

O-I Glass' narrative projects $6.6 billion revenue and $380.4 million earnings by 2029. This implies fairly flat yearly revenue growth and a $509.4 million earnings increase from -$129.0 million today.

Uncover how O-I Glass' forecasts yield a $17.89 fair value, a 89% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts were already cautious, assuming roughly flat revenues around US$6.6 billion and earnings of about US$407 million by 2028, and Q1’s weaker results plus European energy pressures may push that more pessimistic view even further, so it is worth comparing their concerns about rising energy and modernization costs with more optimistic Fit to Win expectations before you decide where you stand.

Explore 3 other fair value estimates on O-I Glass - why the stock might be worth just $17.89!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your O-I Glass research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free O-I Glass research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate O-I Glass' overall financial health at a glance.

Ready For A Different Approach?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with 23 elite penny stocks that balance risk and reward.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com