Should Stronger Smoke-Free Momentum and Higher 2026 EPS Guidance Require Action From Philip Morris (PM) Investors?

- Philip Morris International Inc. reported past first-quarter 2026 results with revenue rising to US$10.15 billion from US$9.30 billion, while net income and diluted EPS from continuing operations eased to US$2.44 billion and US$1.56 respectively, and it updated full-year 2026 EPS guidance to US$7.56–US$7.71.

- Beyond the headline numbers, the quarter underscored how growth in smoke-free products like IQOS and VEEV, supported by pricing power, is reshaping Philip Morris International’s earnings mix even as traditional cigarette volumes soften.

- We’ll now examine how this stronger-than-expected smoke-free performance and updated 2026 EPS guidance may influence Philip Morris International’s investment narrative.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

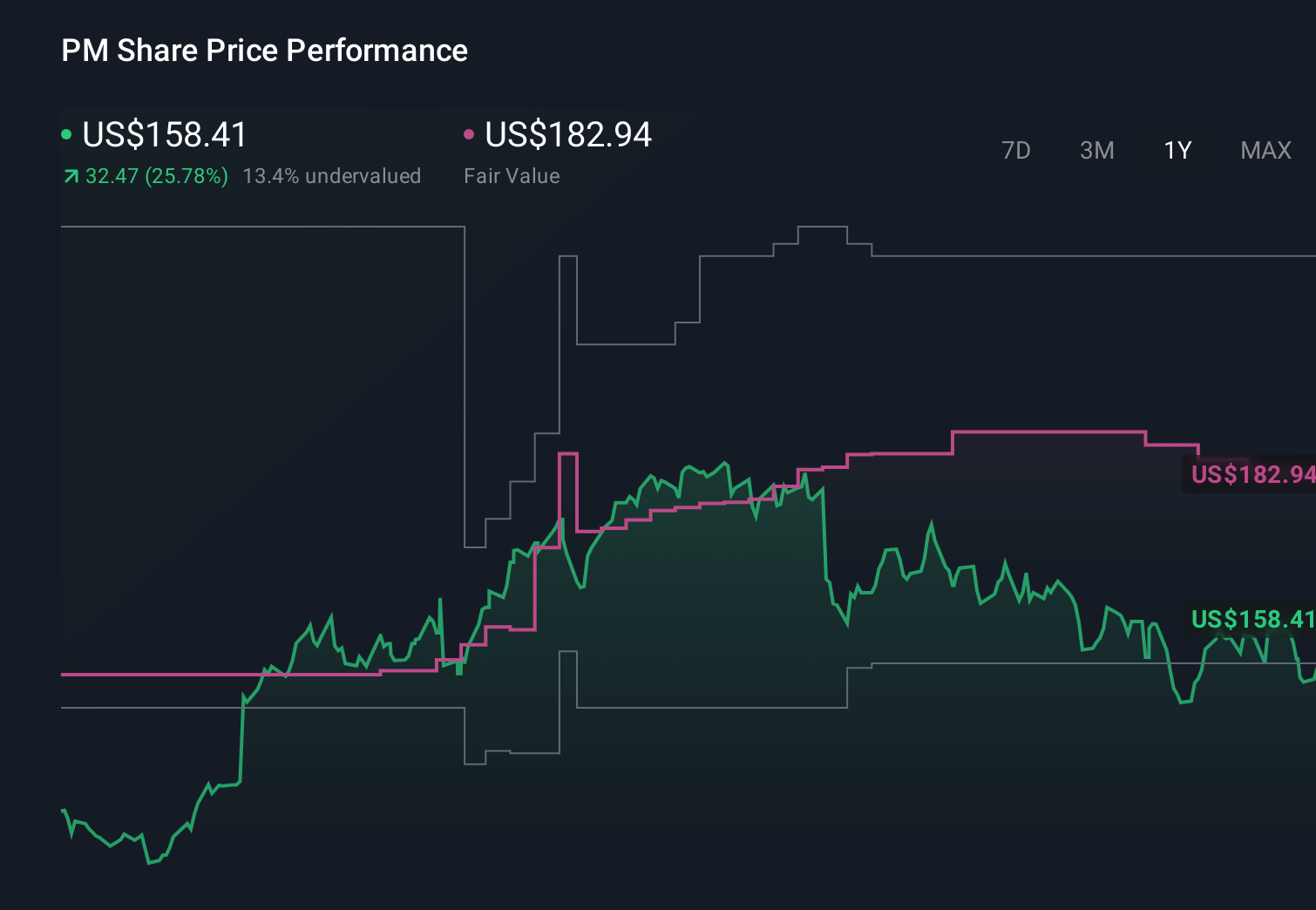

Philip Morris International Investment Narrative Recap

To own Philip Morris International, you need to be comfortable with a tobacco group that is gradually shifting its earnings base toward smoke free products while managing a slow decline in cigarettes. The Q1 2026 beat and updated full year EPS guidance to US$7.56–US$7.71 reinforce the importance of smoke free momentum as the key short term catalyst, while regulatory and growth uncertainty around products like ZYN remains the biggest swing factor.

Among the recent announcements, the FDA’s renewal of modified risk tobacco product orders for IQOS and HEETS stands out as most relevant. It supports PMI’s ability to communicate reduced exposure information to U.S. adult smokers, which ties directly into the smoke free growth narrative underpinning the latest results and guidance, even as broader regulatory and tax risks across regions continue to loom in the background.

Yet behind the strong smoke free story, investors should also be aware of growing regulatory scrutiny and the risk that...

Read the full narrative on Philip Morris International (it's free!)

Philip Morris International’s narrative projects $49.8 billion in revenue and $15.0 billion in earnings by 2029.

Uncover how Philip Morris International's forecasts yield a $195.17 fair value, a 19% upside to its current price.

Exploring Other Perspectives

Some of the most optimistic analysts were assuming revenue could reach about US$52.2 billion and earnings US$15.7 billion by 2029, which is far more bullish than consensus. In light of the latest smoke free outperformance and updated guidance, you can see how views on ZYN and IQOS growth, and on regulatory pushback, could legitimately diverge and may shift again as new data comes through.

Explore 9 other fair value estimates on Philip Morris International - why the stock might be worth just $170.00!

Reach Your Own Conclusion

Don't just follow the ticker - dig into the data and build a conviction that's truly your own.

- A great starting point for your Philip Morris International research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Philip Morris International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Philip Morris International's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

- Capitalize on the AI infrastructure supercycle with our selection of the 38 best 'picks and shovels' of the AI gold rush converting record-breaking demand into massive cash flow.

- Find 56 companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com