Will Dow’s (DOW) New CEO Shift Its Strategic Priorities or Reinforce the Existing Playbook?

- Dow Inc. recently announced that long-time Chair and CEO Jim Fitterling will shift to Executive Chair and Chief Operating Officer Karen S. Carter will become Chief Executive Officer, joining the Board, effective July 1, 2026, while Richard Davis continues as Independent Lead Director.

- Carter’s elevation from COO to CEO brings her extensive operational experience across Dow’s largest businesses directly into the top role, with Fitterling’s continued Board leadership helping maintain leadership continuity and focus on long-term strategy and governance.

- We’ll now examine how Karen S. Carter’s promotion from COO to CEO may influence Dow’s existing investment narrative and future priorities.

AI is about to change healthcare. These 35 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Dow Investment Narrative Recap

To own Dow, you need to believe it can convert a challenged, capital intensive chemicals portfolio into durable cash generation, despite margin pressure, delayed growth projects and weak macro demand. The CEO transition to Karen S. Carter looks more like planned succession than a change to near term drivers, so it does not materially alter the key catalyst of cash preservation and asset rationalization, or the central risk that elevated energy and feedstock costs keep profitability under strain.

The most relevant recent announcement alongside the CEO news is Dow’s reaffirmed quarterly dividend of US$0.35 per share, even as the company remains unprofitable and delays projects like Path2Zero. This reinforces that capital allocation and balance sheet flexibility remain front and center for investors tracking near term catalysts such as cost cuts, European asset reviews and expected cash inflows from asset sales and litigation.

But against this backdrop, investors should also be aware that prolonged margin pressure could still force tougher choices on dividends and deferred projects...

Read the full narrative on Dow (it's free!)

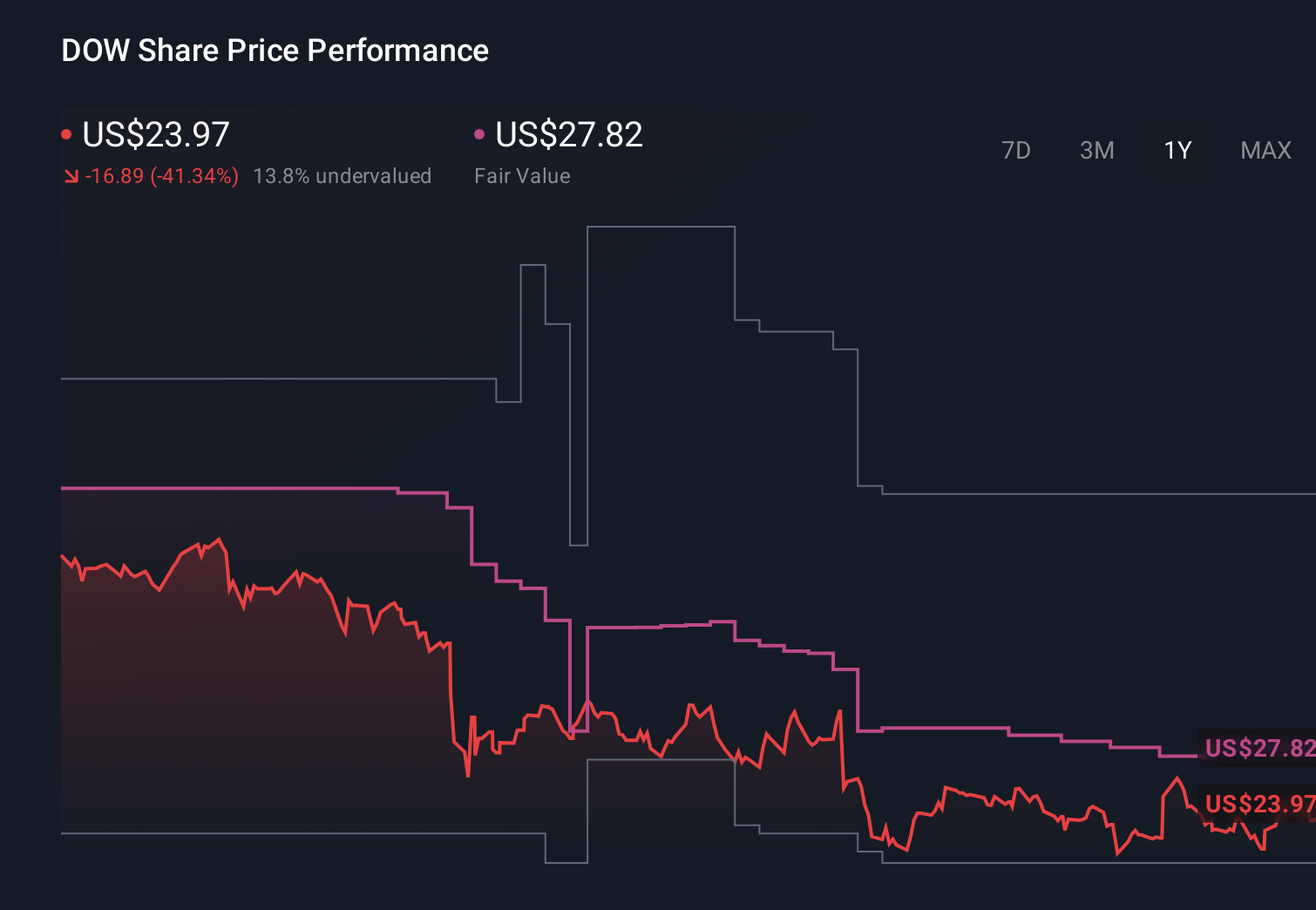

Dow's narrative projects $43.6 billion revenue and $1.5 billion earnings by 2028. This requires 1.4% yearly revenue growth and an earnings increase of about $2.5 billion from -$994.0 million today.

Uncover how Dow's forecasts yield a $29.94 fair value, a 16% downside to its current price.

Exploring Other Perspectives

Some of the lowest estimate analysts paint a much tougher picture, expecting flat revenue near US$39.7 billion and only about US$650 million in earnings by 2029, so compared with the more constructive cost savings and asset optimization story, you can see how opinions can differ sharply and why this leadership change could reshape both narratives over time.

Explore 6 other fair value estimates on Dow - why the stock might be worth 24% less than the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Dow research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Dow research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Dow's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 31 best rare earth metal stocks of the very few that mine this essential strategic resource.

- Invest in the nuclear renaissance through our list of 93 elite nuclear energy infrastructure plays powering the global AI revolution.

- Uncover the next big thing with 25 elite penny stocks that balance risk and reward.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com