Does Ciena (CIEN) Winning Vodafone Idea Deal Quietly Redefine Its AI-Optical Edge?

- Vodafone Idea Limited recently announced it has modernized its transport network using Ciena’s WaveLogic 6 Extreme coherent optical technology on the 6500 platform, enabling 1.6 Tb/s on its meshed Data Center Interconnect network in India and providing a foundation to efficiently support up to 800G services.

- The deployment underscores how Ciena’s WaveLogic 6 Extreme, described as the industry’s first 1.6 Tb/s coherent optical solution, can expand service providers’ addressable markets by boosting fiber capacity while lowering cost per bit and power consumption for high-bandwidth use cases.

- Next, we’ll examine how Ciena’s WaveLogic 6 Extreme win at Vodafone Idea could influence the company’s AI-focused optical investment narrative.

The future of work is here. Discover the 33 top robotics and automation stocks leading the charge in AI-driven automation and industrial transformation.

Ciena Investment Narrative Recap

To own Ciena, you have to believe AI and cloud buildouts keep requiring denser, more power efficient optical networks where WaveLogic 6 can matter. The Vodafone Idea deployment reinforces that story but does not fundamentally change the key near term swing factor: converting strong optical demand into timely deliveries at acceptable margins. The biggest risk remains Ciena’s exposure to a concentrated group of large cloud and telecom buyers whose spending plans can shift quickly.

Among recent developments, Ciena’s March quarter results and FY2026 revenue guidance increase to US$5.9 billion to US$6.3 billion tie directly into the Vodafone Idea news. Together they frame WaveLogic 6 Extreme not just as a flagship product win, but as part of a broader push into AI centric optical upgrades with hyperscalers, neoscalers, and large carriers, which many investors see as the core catalyst for the stock over the next few years.

Yet beneath the AI optics enthusiasm, investors should be aware of how concentrated customer spending could...

Read the full narrative on Ciena (it's free!)

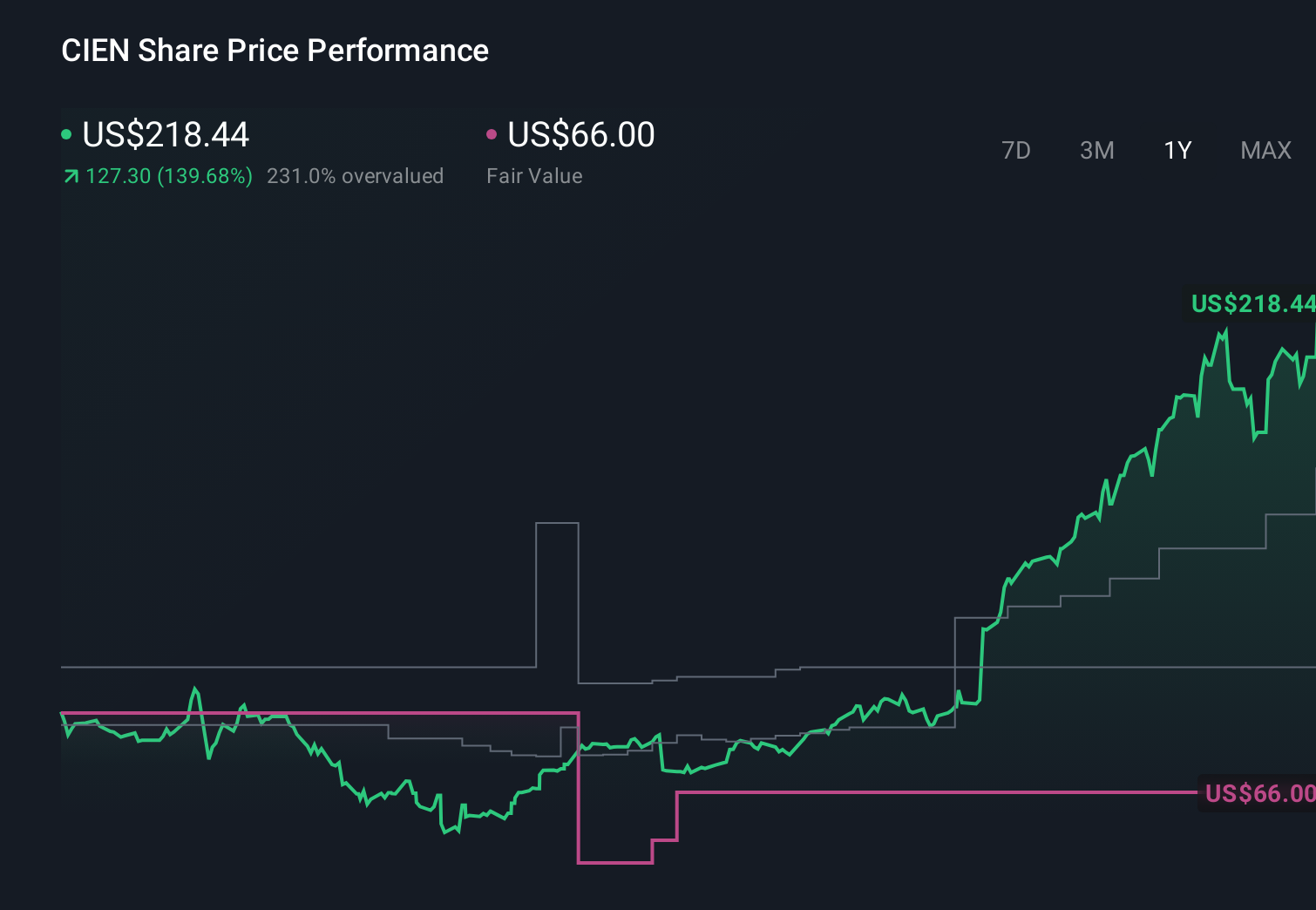

Ciena's narrative projects $6.5 billion revenue and $590.5 million earnings by 2028. This requires 12.5% yearly revenue growth and an earnings increase of about $449.6 million from $140.9 million today.

Uncover how Ciena's forecasts yield a $237.12 fair value, a 47% downside to its current price.

Exploring Other Perspectives

Some analysts are far more cautious, assuming revenue of about US$6.6 billion and earnings near US$589 million by 2028, highlighting how views on AI driven demand and customer concentration can differ widely and may shift again after wins like Vodafone Idea.

Explore 9 other fair value estimates on Ciena - why the stock might be worth less than half the current price!

Reach Your Own Conclusion

Disagree with existing narratives? Extraordinary investment returns rarely come from following the herd, so go with your instincts.

- A great starting point for your Ciena research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Ciena research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Ciena's overall financial health at a glance.

Want Some Alternatives?

Our top stock finds are flying under the radar-for now. Get in early:

- This technology could replace computers: discover 24 stocks that are working to make quantum computing a reality.

- Find 59 companies with promising cash flow potential yet trading below their fair value.

- We've uncovered the 13 dividend fortresses yielding 5%+ that don't just survive market storms, but thrive in them.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com