Nasdaq

Nasdaq 华尔街日报

华尔街日报A Look At Toll Brothers (TOL) Valuation As Long Term Returns Contrast With Recent Share Price Softness

Toll Brothers stock performance snapshot

Toll Brothers (TOL) has been on investors’ radar after recent trading left the stock around $134.80, with returns over the past week, month, and past 3 months showing mixed short term moves.

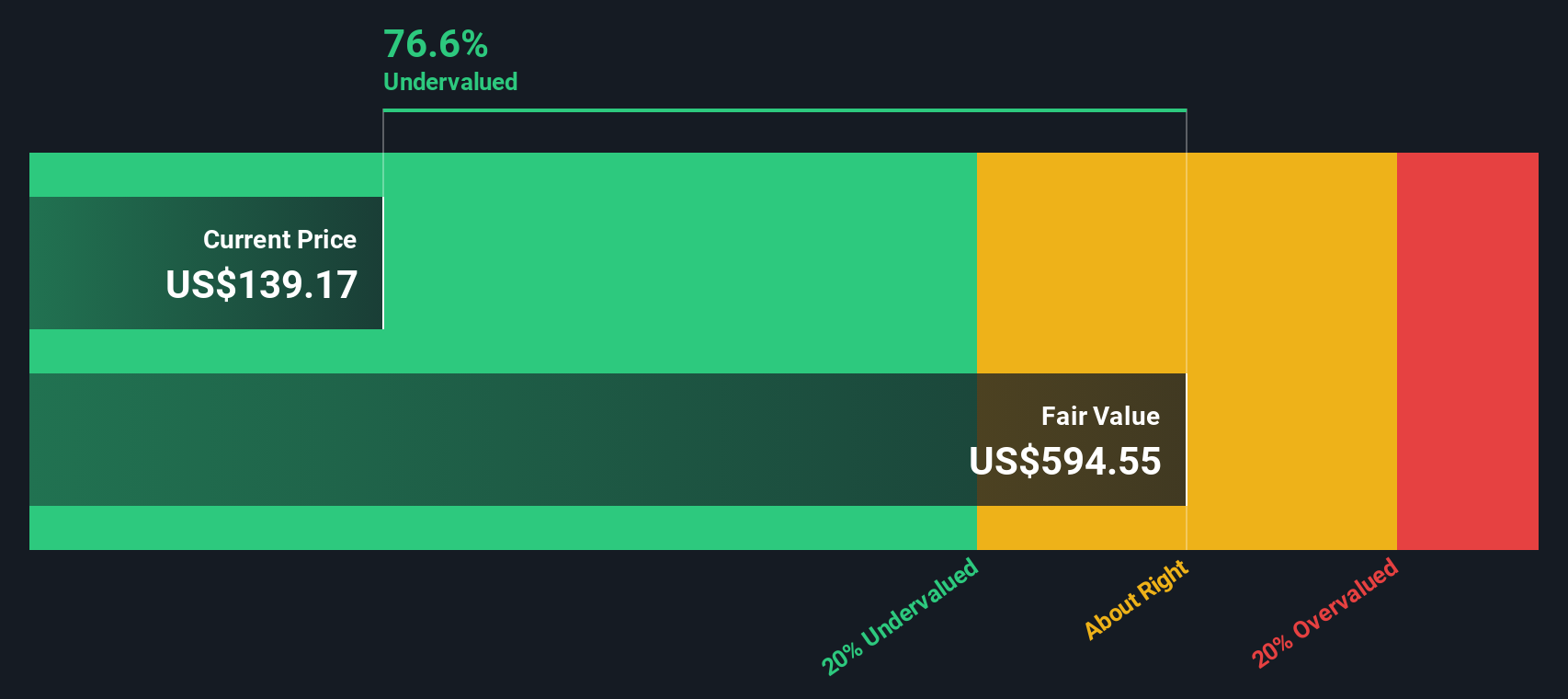

See our latest analysis for Toll Brothers.

At around $134.80, recent share price softness over the past month contrasts with a 90 day share price return of 4.72%, while the 1 year total shareholder return of 7.02% and very large 5 year total shareholder return suggest momentum has been stronger over the longer term as investors reassess growth potential and risks in higher end housing.

If Toll Brothers has you thinking about opportunities in housing and construction, it can be useful to see what else is moving in related areas like auto manufacturers.

With Toll Brothers reporting steady revenue and net income growth and trading around $134.80, the key question is whether the current valuation still leaves upside on the table, or if the market is already pricing in that growth.

Most Popular Narrative Narrative: 11.5% Undervalued

With Toll Brothers last closing at $134.80 against a narrative fair value of $152.40, the gap centers on how durable future earnings and margins might be.

Analysts are assuming Toll Brothers's revenue will grow by 6.3% annually over the next 3 years.

Analysts assume that profit margins will increase from 12.6% today to 12.8% in 3 years time.

Want to see what happens when steady top line growth meets slightly higher margins and a lower future earnings multiple than the industry? The full narrative walks through how those moving pieces stack up to support the fair value and why it still implies a valuation discount even after trimming growth assumptions.

Result: Fair Value of $152.4 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on buyers continuing to absorb a higher mix of spec homes and on luxury demand holding up if rates stay elevated or if economic conditions soften.

Find out about the key risks to this Toll Brothers narrative.

Another View: What Our DCF Model Says

Analysts see Toll Brothers as about 11.5% undervalued using their fair value of $152.40, but our DCF model offers a different view. On that method, the shares at $134.80 sit above an estimate of fair value at $128.07, which points to a mild overvaluation instead.

That gap is not huge in either direction, but it does place more weight on your own assumptions about future cash flows, housing demand, and margins. Do you lean more toward the market aligning with analyst estimates, or the more cautious signal from the SWS DCF model?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Toll Brothers for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 884 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Toll Brothers Narrative

If this view does not quite fit how you see Toll Brothers, or you prefer to work from your own numbers, you can pull the same data, test your assumptions, and build a custom story for the stock in just a few minutes with Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Toll Brothers.

Looking for more investment ideas?

If Toll Brothers is only one piece of your watchlist, now is the time to broaden your research and line up a few more potential opportunities.

- Spot early stage potential by scanning these 3545 penny stocks with strong financials that already show stronger fundamentals than many expect at this price range.

- Position yourself for the next wave of automation and data trends by zeroing in on these 26 AI penny stocks shaping how AI shows up in real businesses.

- Hunt for quality at a price by filtering for these 884 undervalued stocks based on cash flows that might not match their cash flow profiles right now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com