Nasdaq

Nasdaq 华尔街日报

华尔街日报Aura Minerals (NasdaqGS:AUGO) Valuation Check As Era Dorada Gold Project Secures Construction License

Aura Minerals (AUGO) has secured the construction license for its Era Dorada gold project in Guatemala and started early site works, a key step in turning this acquired asset into an operating mine.

See our latest analysis for Aura Minerals.

The Era Dorada progress comes after a sharp run in Aura Minerals’ shares, with a 30-day share price return of 26.89% and a 90-day share price return of 39.20%, while the 1-year total shareholder return is roughly 4.7x. This suggests momentum has been building around the story.

If this kind of project news has your attention, it could be a good moment to look beyond a single name and see fast growing stocks with high insider ownership as well.

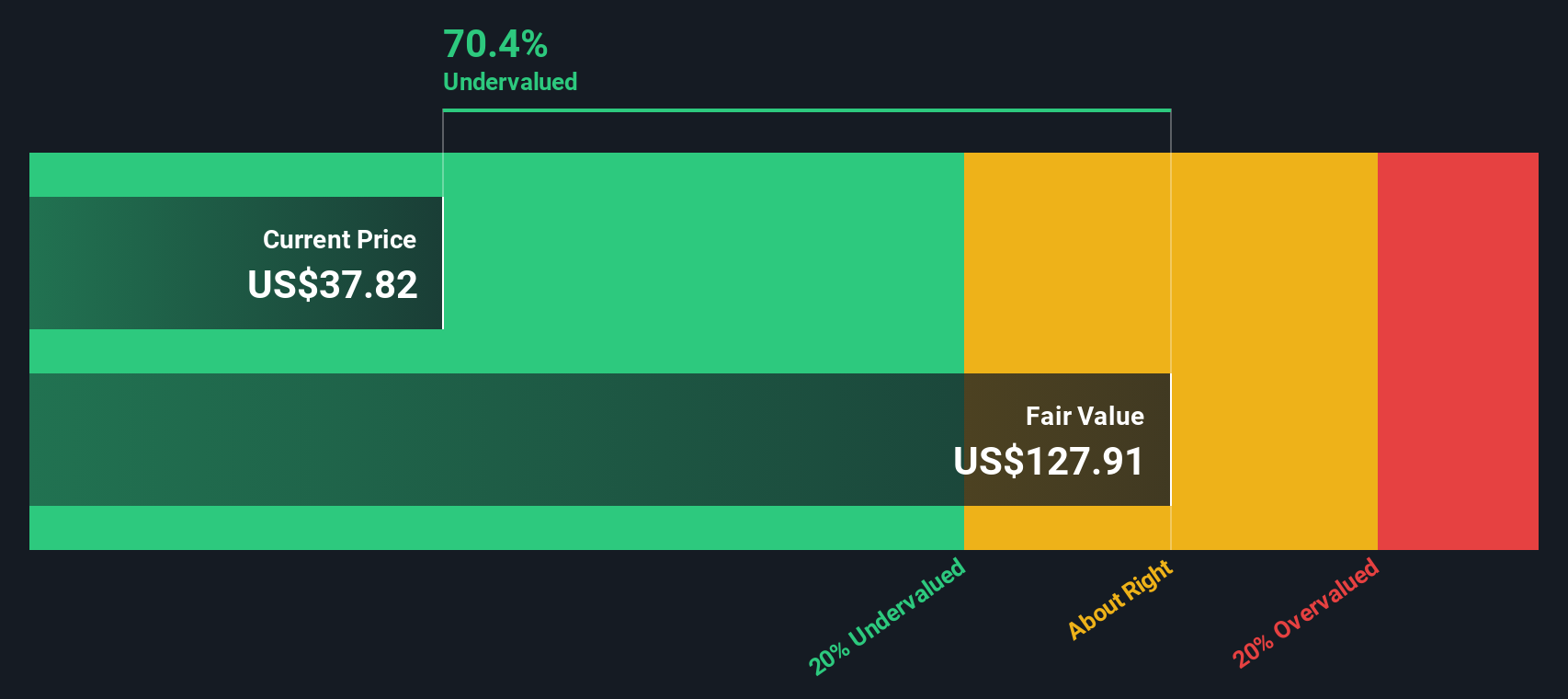

With Aura trading close to its US$54.52 analyst price target and showing very large 1 year returns, plus an indicated 65% intrinsic discount, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Price-to-Sales of 5.5x: Is It Justified?

Aura Minerals last closed at US$51.24, and on a P/S of 5.5x it screens as expensive versus both its own fair ratio and the wider US metals and mining industry.

The P/S multiple compares the company’s market value to its revenue, which is often useful for miners and other businesses that are not currently profitable. For Aura, this means investors are paying 5.5 times its US$771.589m of revenue, a higher mark up than the 2.5x industry average even though the company is reporting a net loss of US$42.832m.

According to the SWS fair ratio work, a P/S of 4.9x would be more in line with what the fundamentals currently support. Today’s 5.5x therefore suggests the market is applying a premium. That premium sits on top of an industry context where peers, on average, trade at a much lower 2.5x. This makes Aura’s valuation stand out clearly on the richer side of the spectrum.

Explore the SWS fair ratio for Aura Minerals

Result: Price-to-Sales of 5.5x (OVERVALUED)

However, there are clear pressure points too, including the current net loss of US$42.832m and the risk that sentiment cools if project execution or commodity prices disappoint.

Find out about the key risks to this Aura Minerals narrative.

Another View: DCF Points to a Very Different Price

While the 5.5x P/S suggests Aura might be priced richly on sales, our DCF model tells a very different story. On that framework, the estimated fair value sits at US$148.27 per share versus the current US$51.24, implying Aura trades at a very large discount. Which signal do you trust more: a rich sales multiple or a big DCF gap?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aura Minerals for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 884 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Aura Minerals Narrative

If parts of this view do not sit right with you, or you prefer to weigh the numbers yourself, you can build a fresh narrative in just a few minutes by starting with Do it your way.

A great starting point for your Aura Minerals research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If Aura has sharpened your thinking, do not stop here. The right watchlist can put you one step ahead when the next opportunity appears.

- Spot potential bargains early by checking out these 884 undervalued stocks based on cash flows that the market may be pricing cautiously relative to their cash flows.

- Tap into powerful trends by scanning these 26 AI penny stocks that sit at the intersection of data, automation and long term demand shifts.

- Strengthen your income stream by reviewing these 12 dividend stocks with yields > 3% that offer yields above 3% while you assess quality and payout reliability.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com