Nasdaq

Nasdaq 华尔街日报

华尔街日报Tecnisa S.A.'s (BVMF:TCSA3) Share Price Not Quite Adding Up

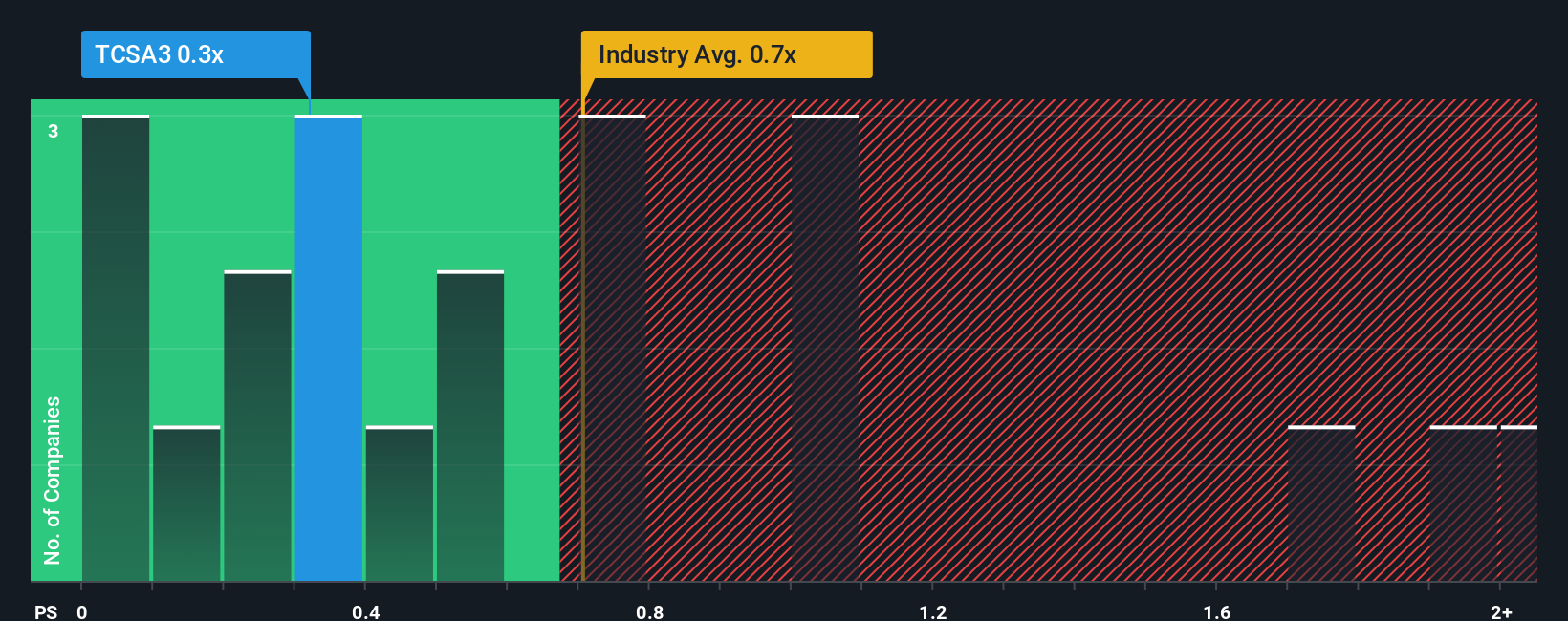

There wouldn't be many who think Tecnisa S.A.'s (BVMF:TCSA3) price-to-sales (or "P/S") ratio of 0.3x is worth a mention when the median P/S for the Consumer Durables industry in Brazil is similar at about 0.8x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Tecnisa

What Does Tecnisa's P/S Mean For Shareholders?

Tecnisa hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. One possibility is that the P/S ratio is moderate because investors think this poor revenue performance will turn around. If not, then existing shareholders may be a little nervous about the viability of the share price.

Want the full picture on analyst estimates for the company? Then our free report on Tecnisa will help you uncover what's on the horizon.Is There Some Revenue Growth Forecasted For Tecnisa?

Tecnisa's P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 38%. However, a few very strong years before that means that it was still able to grow revenue by an impressive 61% in total over the last three years. Accordingly, while they would have preferred to keep the run going, shareholders would definitely welcome the medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to slump, contracting by 8.7% during the coming year according to the sole analyst following the company. Meanwhile, the broader industry is forecast to expand by 20%, which paints a poor picture.

In light of this, it's somewhat alarming that Tecnisa's P/S sits in line with the majority of other companies. Apparently many investors in the company reject the analyst cohort's pessimism and aren't willing to let go of their stock right now. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

What We Can Learn From Tecnisa's P/S?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Our check of Tecnisa's analyst forecasts revealed that its outlook for shrinking revenue isn't bringing down its P/S as much as we would have predicted. With this in mind, we don't feel the current P/S is justified as declining revenues are unlikely to support a more positive sentiment for long. If we consider the revenue outlook, the P/S seems to indicate that potential investors may be paying a premium for the stock.

There are also other vital risk factors to consider before investing and we've discovered 1 warning sign for Tecnisa that you should be aware of.

If you're unsure about the strength of Tecnisa's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.