Nasdaq

Nasdaq 华尔街日报

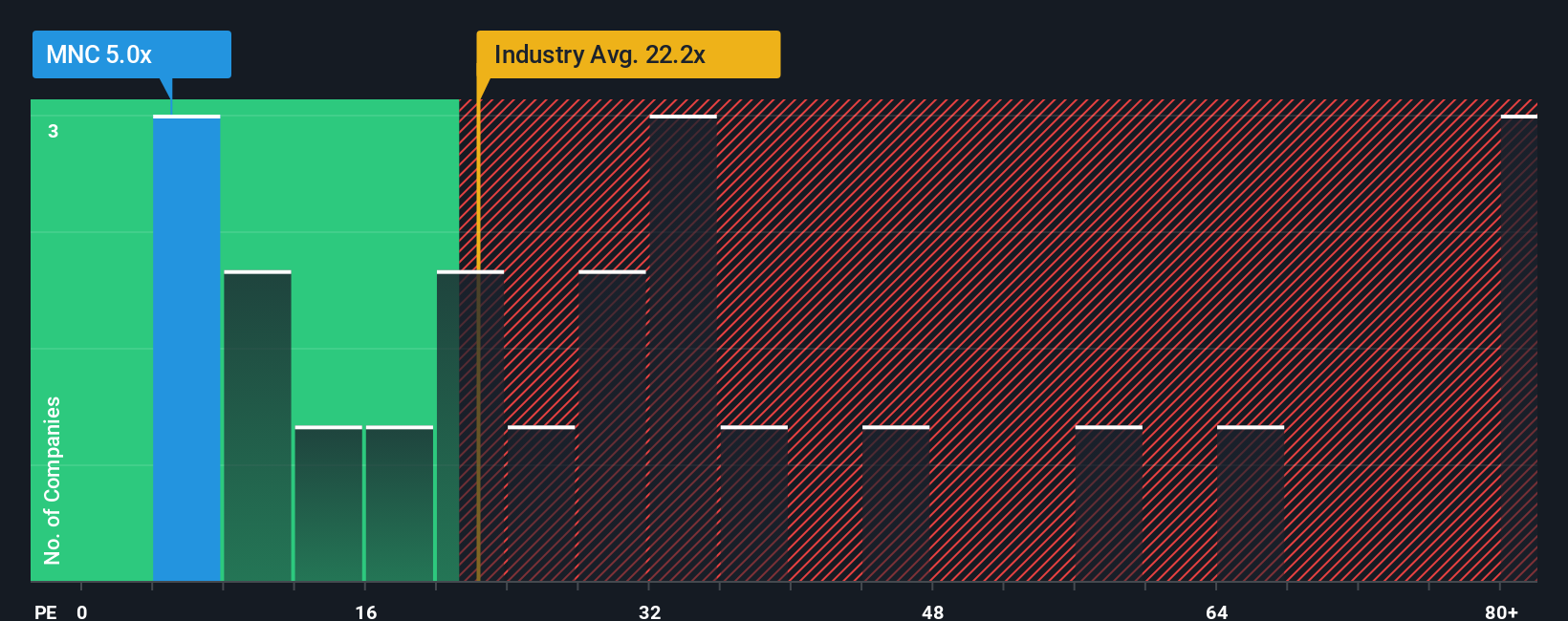

华尔街日报Market Might Still Lack Some Conviction On Mennica Polska S.A. (WSE:MNC) Even After 27% Share Price Boost

Despite an already strong run, Mennica Polska S.A. (WSE:MNC) shares have been powering on, with a gain of 27% in the last thirty days. The last month tops off a massive increase of 139% in the last year.

Even after such a large jump in price, given about half the companies in Poland have price-to-earnings ratios (or "P/E's") above 13x, you may still consider Mennica Polska as a highly attractive investment with its 5x P/E ratio. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/E.

With earnings growth that's exceedingly strong of late, Mennica Polska has been doing very well. One possibility is that the P/E is low because investors think this strong earnings growth might actually underperform the broader market in the near future. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for Mennica Polska

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as depressed as Mennica Polska's is when the company's growth is on track to lag the market decidedly.

Retrospectively, the last year delivered an exceptional 358% gain to the company's bottom line. Pleasingly, EPS has also lifted 1,754% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Weighing that recent medium-term earnings trajectory against the broader market's one-year forecast for expansion of 18% shows it's noticeably more attractive on an annualised basis.

With this information, we find it odd that Mennica Polska is trading at a P/E lower than the market. Apparently some shareholders believe the recent performance has exceeded its limits and have been accepting significantly lower selling prices.

The Key Takeaway

Shares in Mennica Polska are going to need a lot more upward momentum to get the company's P/E out of its slump. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Mennica Polska currently trades on a much lower than expected P/E since its recent three-year growth is higher than the wider market forecast. When we see strong earnings with faster-than-market growth, we assume potential risks are what might be placing significant pressure on the P/E ratio. At least price risks look to be very low if recent medium-term earnings trends continue, but investors seem to think future earnings could see a lot of volatility.

Plus, you should also learn about this 1 warning sign we've spotted with Mennica Polska.

Of course, you might also be able to find a better stock than Mennica Polska. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.