Nasdaq

Nasdaq 华尔街日报

华尔街日报BlueScope Steel (ASX:BSL) Valuation Check After Strong Recent Share Price Performance

BlueScope Steel: recent share performance in focus

Recent trading in BlueScope Steel (ASX:BSL) has drawn attention after a strong run over the past 3 months, leaving investors weighing how the current A$29.87 share price lines up with fundamentals.

See our latest analysis for BlueScope Steel.

That recent 24.1% 7 day share price return and 37.97% 90 day share price return sit alongside a 58.6% 1 year total shareholder return. Together, these figures suggest strong momentum and a shift in how investors are pricing BlueScope Steel’s prospects and risks.

If strong recent moves in BlueScope have your attention, it can be useful to widen the lens and check out fast growing stocks with high insider ownership as other potential ideas.

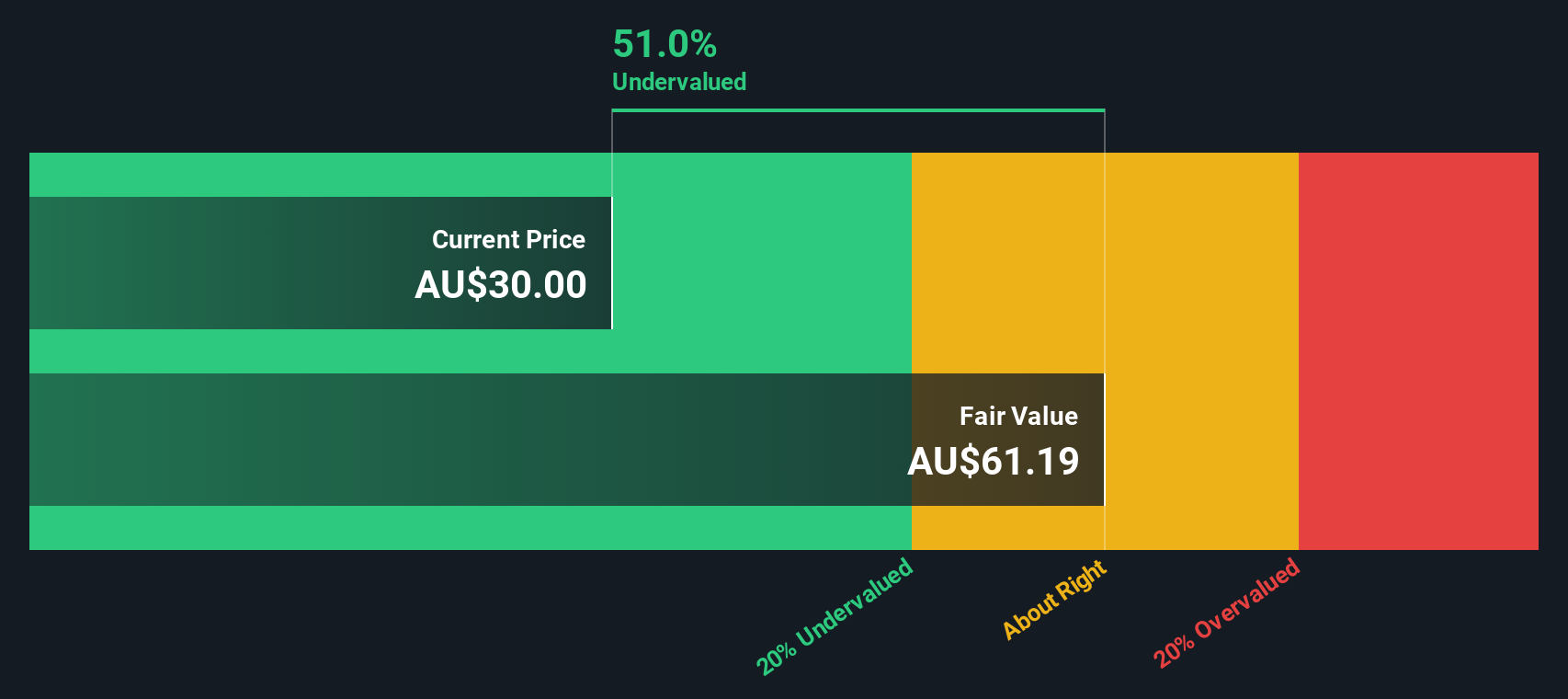

So with BlueScope trading around A$29.87, a 51% gap to one intrinsic value estimate but sitting above the A$27.81 analyst target, you have to ask: is there still a buying opportunity here, or is the market already pricing in future growth?

Most Popular Narrative: 20.3% Overvalued

On the most followed narrative, BlueScope’s fair value sits at A$24.83, below the A$29.87 last close, so the shares screen as expensive on that framework.

In order for you to agree with the analyst's consensus, you'd need to believe that by 2028, revenues will be A$18.1 billion, earnings will come to A$975.1 million, and it would be trading on a PE ratio of 13.7x, assuming you use a discount rate of 7.1%.

Curious what justifies paying up today for a lower future P/E, higher profit margin, and a very different earnings base than now? The full narrative spells it out.

Analysts in this narrative are effectively pricing BlueScope off projected mid single digit revenue growth, a step change in margins and a future earnings multiple below the broader Australian metals and mining peer P/E. Those moving parts, discounted at about 7.1%, are what pull the fair value down below the current share price even though the earnings line they use is significantly higher than today.

Result: Fair Value of A$24.83 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that story can change quickly if higher Australian energy costs or ongoing weakness in the U.S. coated products business continue to squeeze margins instead of improving them.

Find out about the key risks to this BlueScope Steel narrative.

Another View: Market Pricing Versus Cash Flow

That “overvalued” A$24.83 narrative sits uncomfortably next to Simply Wall St’s own DCF work, which points to a fair value of A$60.97. On that SWS DCF model, BlueScope at A$29.87 screens as trading about 51% below fair value, so which set of assumptions do you trust more?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own BlueScope Steel Narrative

If you look at these assumptions and want to stress test them yourself, the tools are there for you to build a custom view in minutes: Do it your way.

A great starting point for your BlueScope Steel research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

If BlueScope has sharpened your focus, do not stop here. Use the Simply Wall St screener to quickly surface fresh ideas you might otherwise miss.

- Spot potential value by hunting through these 877 undervalued stocks based on cash flows where market prices sit below estimated cash flow based worth.

- Ride major tech shifts by scanning these 25 AI penny stocks for companies tied to artificial intelligence trends across sectors.

- Target income-focused opportunities with these 11 dividend stocks with yields > 3% that may suit investors looking for yields above 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com