Nasdaq

Nasdaq 华尔街日报

华尔街日报Does VinFast’s Shelf Offering And Record Vietnam EV Deliveries Change The Bull Case For VFS?

- VinFast Auto Ltd. recently closed a shelf registration dated November 12, 2025 for US$470.62 million, offering 133,320,822 ordinary shares, and previously reported record preliminary domestic deliveries of 23,186 electric vehicles in Vietnam in November 2025, led by the Limo Green model.

- The combination of fresh capital access and the company’s highest monthly EV deliveries highlights how VinFast is simultaneously strengthening its balance sheet and scaling its Green lineup in its core market.

- We’ll now examine how VinFast’s record November EV deliveries in Vietnam may reshape its investment narrative and long-term expansion plans.

The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

VinFast Auto Investment Narrative Recap

To own VinFast today, you need to believe the company can turn strong domestic EV delivery momentum into scale, while managing high cash burn and ongoing funding needs. The closed US$470.62 million shelf registration and record November deliveries in Vietnam support near term balance sheet flexibility, but do not remove the key risk around liquidity and potential shareholder dilution.

Among recent developments, VinFast’s disclosure that it had a quarterly cash burn of US$607 million in Q1 2025, with a projected US$2–2.5 billion annual burn, feels especially relevant. The fresh shelf capacity and record domestic volumes sit directly against this backdrop of heavy funding requirements, which remain central to how investors may think about catalysts like further expansion in Vietnam and across Southeast Asia.

However, investors should also be aware that the company’s reliance on external funding and the possibility of future equity issuance could...

Read the full narrative on VinFast Auto (it's free!)

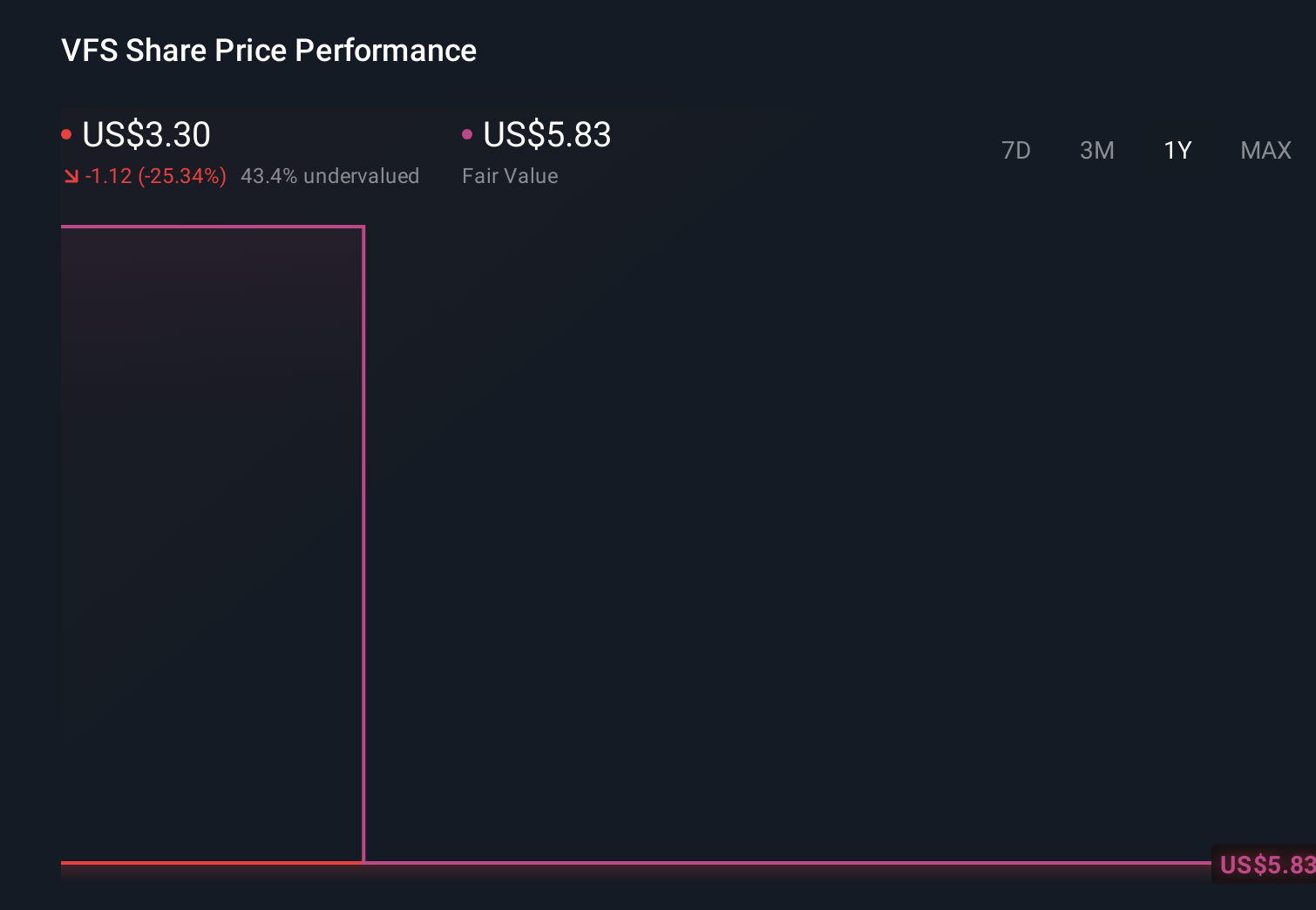

VinFast Auto's narrative projects ₫177527.7 billion revenue and ₫8991.9 billion earnings by 2028.

Uncover how VinFast Auto's forecasts yield a $6.36 fair value, a 84% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community value VinFast between US$4.05 and US$88 per share, showing sharply different expectations. When you set those views against VinFast’s sustained cash burn and liquidity risk, it underlines why you may want to compare several perspectives before forming your own.

Explore 5 other fair value estimates on VinFast Auto - why the stock might be worth just $4.05!

Build Your Own VinFast Auto Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your VinFast Auto research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free VinFast Auto research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate VinFast Auto's overall financial health at a glance.

No Opportunity In VinFast Auto?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- AI is about to change healthcare. These 29 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com