Nasdaq

Nasdaq 华尔街日报

华尔街日报Some Shareholders Feeling Restless Over Rani Zim Shopping Centers Ltd's (TLV:RANI) P/E Ratio

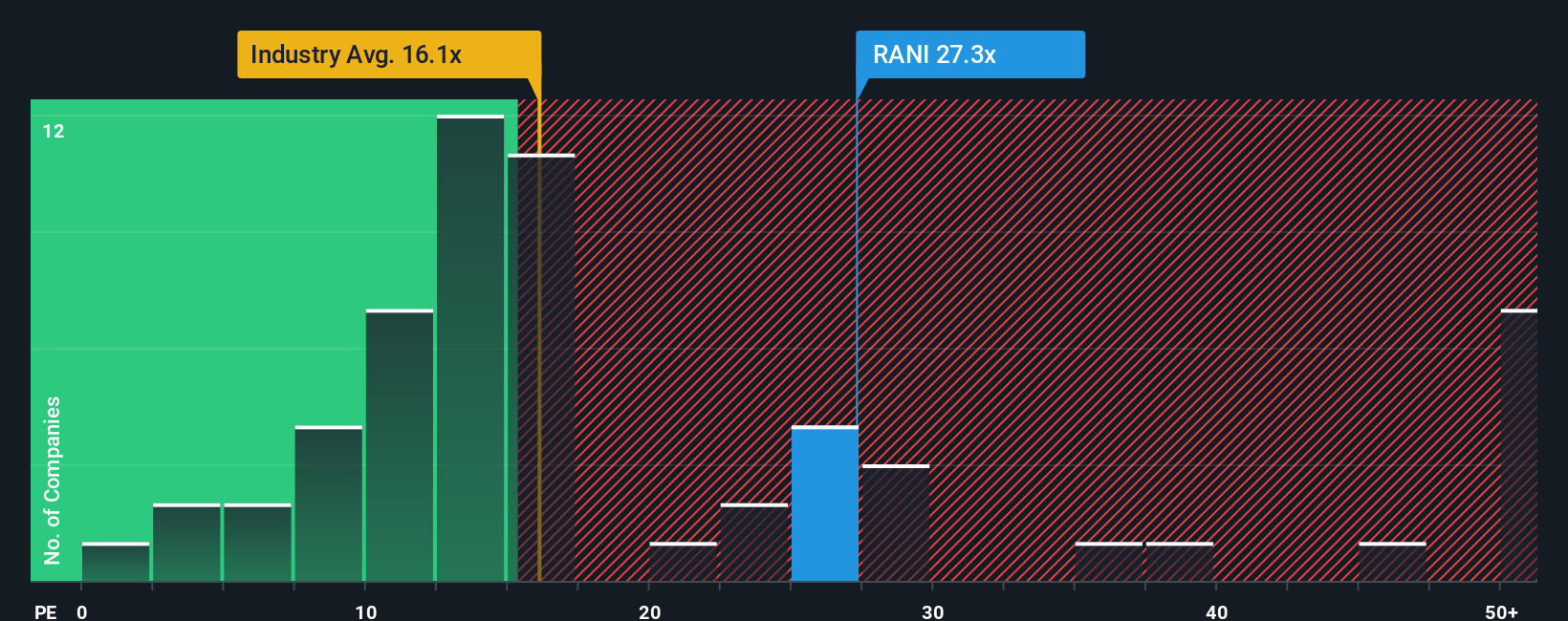

Rani Zim Shopping Centers Ltd's (TLV:RANI) price-to-earnings (or "P/E") ratio of 27.3x might make it look like a strong sell right now compared to the market in Israel, where around half of the companies have P/E ratios below 16x and even P/E's below 11x are quite common. However, the P/E might be quite high for a reason and it requires further investigation to determine if it's justified.

For example, consider that Rani Zim Shopping Centers' financial performance has been poor lately as its earnings have been in decline. It might be that many expect the company to still outplay most other companies over the coming period, which has kept the P/E from collapsing. If not, then existing shareholders may be quite nervous about the viability of the share price.

Check out our latest analysis for Rani Zim Shopping Centers

Does Growth Match The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Rani Zim Shopping Centers' to be considered reasonable.

Retrospectively, the last year delivered a frustrating 72% decrease to the company's bottom line. The last three years don't look nice either as the company has shrunk EPS by 71% in aggregate. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Weighing that medium-term earnings trajectory against the broader market's one-year forecast for expansion of 23% shows it's an unpleasant look.

With this information, we find it concerning that Rani Zim Shopping Centers is trading at a P/E higher than the market. Apparently many investors in the company are way more bullish than recent times would indicate and aren't willing to let go of their stock at any price. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh heavily on the share price eventually.

The Key Takeaway

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that Rani Zim Shopping Centers currently trades on a much higher than expected P/E since its recent earnings have been in decline over the medium-term. When we see earnings heading backwards and underperforming the market forecasts, we suspect the share price is at risk of declining, sending the high P/E lower. If recent medium-term earnings trends continue, it will place shareholders' investments at significant risk and potential investors in danger of paying an excessive premium.

You should always think about risks. Case in point, we've spotted 5 warning signs for Rani Zim Shopping Centers you should be aware of, and 1 of them is significant.

If you're unsure about the strength of Rani Zim Shopping Centers' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.