Nasdaq

Nasdaq 华尔街日报

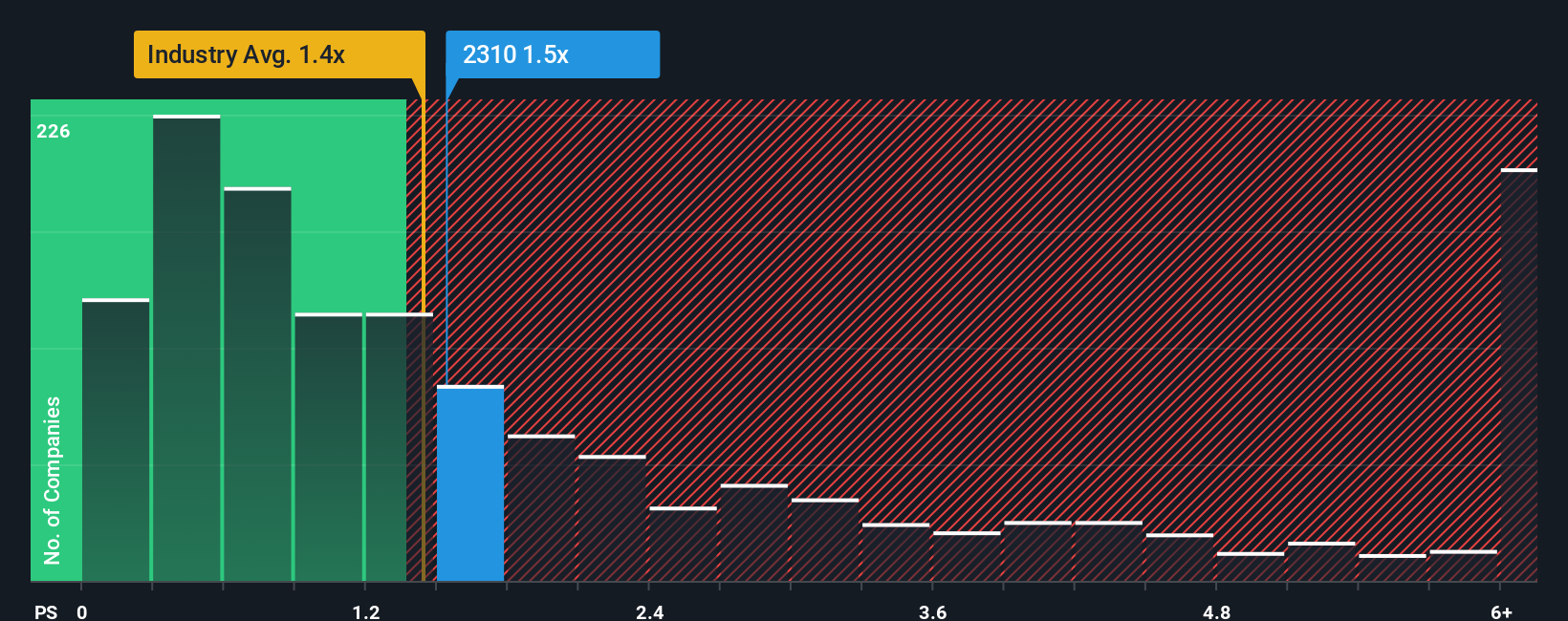

华尔街日报Some Confidence Is Lacking In Sahara International Petrochemical Company's (TADAWUL:2310) P/S

There wouldn't be many who think Sahara International Petrochemical Company's (TADAWUL:2310) price-to-sales (or "P/S") ratio of 1.5x is worth a mention when the median P/S for the Chemicals industry in Saudi Arabia is very similar. Although, it's not wise to simply ignore the P/S without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

View our latest analysis for Sahara International Petrochemical

What Does Sahara International Petrochemical's P/S Mean For Shareholders?

While the industry has experienced revenue growth lately, Sahara International Petrochemical's revenue has gone into reverse gear, which is not great. It might be that many expect the dour revenue performance to strengthen positively, which has kept the P/S from falling. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Sahara International Petrochemical.Is There Some Revenue Growth Forecasted For Sahara International Petrochemical?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Sahara International Petrochemical's to be considered reasonable.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 5.2%. This means it has also seen a slide in revenue over the longer-term as revenue is down 37% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been undesirable for the company.

Looking ahead now, revenue is anticipated to slump, contracting by 0.7% during the coming year according to the six analysts following the company. With the industry predicted to deliver 0.9% growth, that's a disappointing outcome.

With this in consideration, we think it doesn't make sense that Sahara International Petrochemical's P/S is closely matching its industry peers. It seems most investors are hoping for a turnaround in the company's business prospects, but the analyst cohort is not so confident this will happen. There's a good chance these shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with the negative growth outlook.

The Bottom Line On Sahara International Petrochemical's P/S

We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

Our check of Sahara International Petrochemical's analyst forecasts revealed that its outlook for shrinking revenue isn't bringing down its P/S as much as we would have predicted. When we see a gloomy outlook like this, our immediate thoughts are that the share price is at risk of declining, negatively impacting P/S. If the declining revenues were to materialize in the form of a declining share price, shareholders will be feeling the pinch.

Having said that, be aware Sahara International Petrochemical is showing 1 warning sign in our investment analysis, you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.