Nasdaq

Nasdaq 华尔街日报

华尔街日报Assessing Loblaw Companies (TSX:L) Valuation After Strong Multi Year Shareholder Returns

Loblaw Companies (TSX:L) is drawing attention after recent trading data showed mixed short term performance, with a small gain over the past week and a slight decline over the past month.

See our latest analysis for Loblaw Companies.

Loblaw’s recent 90 day share price return of 14.24% stands out against quieter day to day moves around its CA$62.09 level. Its 1 year total shareholder return of 32.77% and 5 year total shareholder return of 312.08% point to momentum that has been building over a longer horizon as investors react to the company’s mix of food retail and pharmacy earnings, ongoing healthcare service expansion and its financial services arm.

If you are weighing Loblaw’s steady profile against other ideas, this could be a good moment to broaden your watchlist with healthcare stocks.

With Loblaw trading close to analyst price targets after strong multi year returns, the key question now is whether the recent earnings profile still leaves upside on the table or if the market is already pricing in future growth.

Most Popular Narrative: 1% Undervalued

The most followed narrative sees Loblaw’s fair value at CA$62.55, very close to the last close of CA$62.09, and ties that view to specific earnings and margin expectations.

“The analysts have a consensus price target of CA$59.477 for Loblaw Companies based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of CA$66.75, and the most bearish reporting a price target of just CA$39.0.”

Want to see how modest revenue growth, steady margins and a premium future earnings multiple all fit together? The narrative leans on detailed forecasts and a specific discount rate. Curious which assumptions have the biggest impact on that CA$62.55 fair value?

Result: Fair Value of $62.55 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.

However, this hinges on Loblaw holding its ground against rising online grocery competition, as well as any future regulatory scrutiny around pricing that could pressure margins.

Find out about the key risks to this Loblaw Companies narrative.

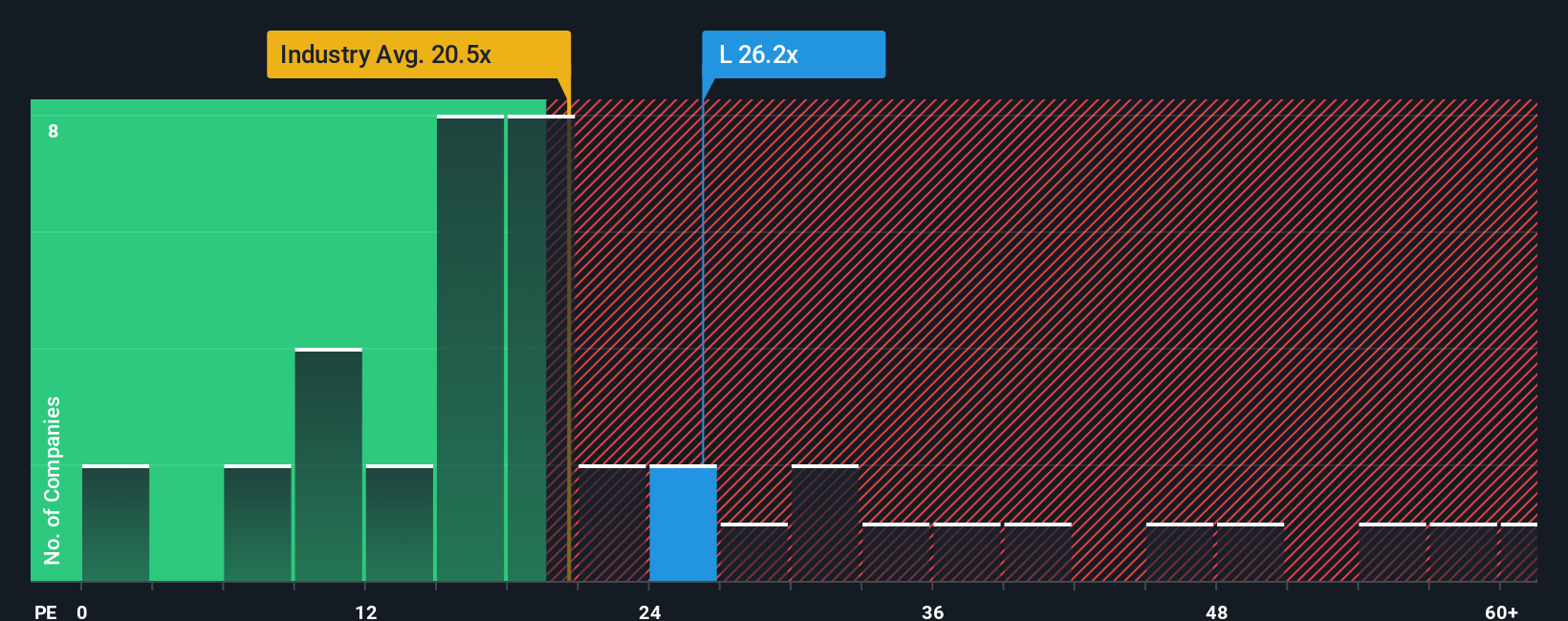

Another Angle: Rich On Earnings Multiples

While the popular narrative pins Loblaw’s fair value close to CA$62.55, the earnings multiple view is less forgiving. At a P/E of 29.5x, the shares sit well above the North American Consumer Retailing average of 22.8x and a fair ratio of 24.7x, which points to an expensive profile rather than a bargain. If sentiment cools or growth expectations ease, that valuation gap could become a source of downside risk.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Loblaw Companies Narrative

If you look at the numbers and reach a different conclusion, or simply prefer to test your own assumptions, you can build a custom view in just a few minutes with Do it your way.

A great starting point for your Loblaw Companies research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

If your thesis on Loblaw is taking shape, do not stop there. Use the same disciplined approach to scan other opportunities before the next move gets away from you.

- Spot potential value opportunities early by checking out these 870 undervalued stocks based on cash flows that may offer stronger cash flow support for their current prices.

- Tap into growth themes in technology and automation by reviewing these 25 AI penny stocks that are tied to long term AI adoption trends.

- Strengthen your income focus by assessing these 14 dividend stocks with yields > 3% that could add more consistent yield to your portfolio.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com